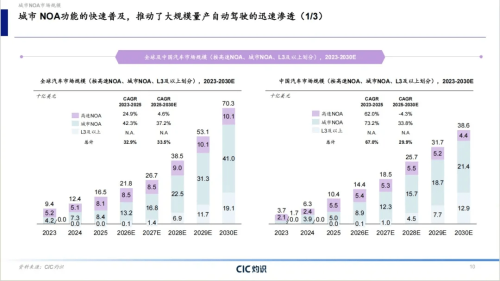

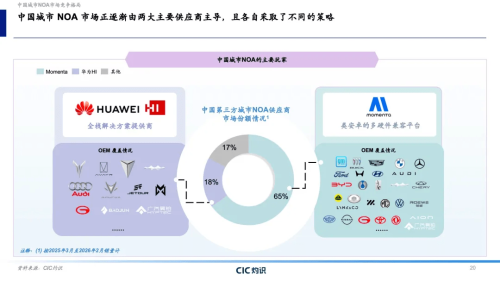

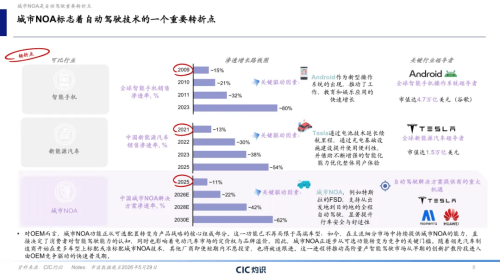

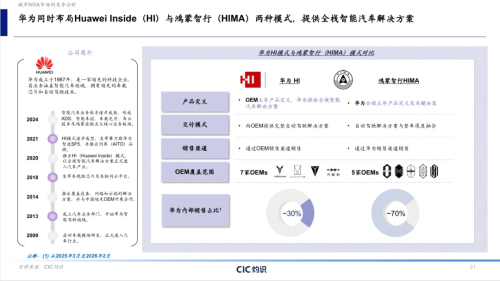

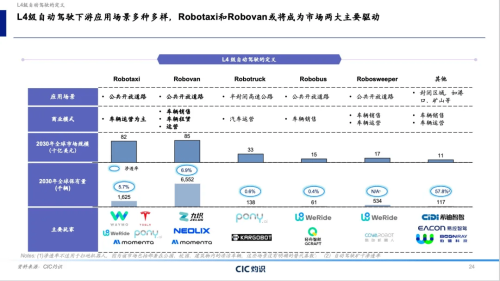

On June 15, research firm CIC Consulting released its “Autonomous Driving Industry Bluebook – Urban NOA: The Turning Point in Commercialization of Autonomous Driving.” The report shows that penetration of new energy vehicles (NEVs) in China has increased from 13% in 2021 to 54% in 2025. As electrification moves into its next phase, intelligent driving systems are becoming the key competitive focus for automakers, with urban Navigation on Autopilot (NOA) emerging as one of the most commercially viable intelligent driving capabilities. From a market size perspective, the global production-level autonomous driving market is expected to grow from approximately $16.5 billion in 2025 to $70.3 billion in 2030. Global and Chinese automotive market projections for different levels of automated vehicles Within this, the China market is projected to expand from $10.4 billion to $38.6 billion over the same period, representing a compound annual growth rate (CAGR) of around 29.9%, making it one of the largest autonomous driving markets globally. Against this backdrop, urban NOA penetration is rising rapidly. The Bluebook shows that between March 2025 and February 2026, in China’s third-party urban NOA supplier market, Momenta ranked first with a 65% market share, while Huawei ranked second with 18%. Together, the two companies account for more than 80% of the market, indicating a clear concentration structure in the third-party urban NOA segment. Market share of major suppliers in China’s NOA market This consolidation is closely linked to the rapid expansion of urban NOA adoption. According to the report, penetration of urban NOA solutions in China is expected to increase from 11.3% in 2025 to 62.4% in 2030. Over the same period, annual sales of vehicles equipped with urban NOA are projected to rise from 2.6 million units to 18.2 million units, representing a CAGR of 47.8%. In terms of adoption pathways, urban NOA is moving from high-priced models into the mass market. Penetration rates of global smart phones, China NEVs, and China’s urban NOA The report estimates that by 2030, penetration in the 100,000–200,000 yuan ($14,750–$29,500) price segment will rise from 3.8% to 62.7%, while the 200,000–400,000 yuan ($29,500–$59,000) segment is expected to approach 97%. In terms of competitive structure, Momenta and Huawei represent two distinct development paths. Momenta follows an open-platform model, providing autonomous driving solutions to multiple automakers. The company currently partners with 9 of the world’s top 10 automakers, with its production-ready solutions deployed across more than 10 countries and regions in Asia, Europe, and Oceania. Huawei, meanwhile, operates through a dual-track strategy: Huawei Inside (HI) and Harmony Intelligent Mobility Alliance (HIMA). Huawei Inside (HI) and HIMA automotive solutions Leveraging brands such as Avatr, Deepal, and Voyah, as well as Aito and Luxeed, the company continues to expand its smart driving deployment base. Urban NOA is also increasingly viewed as a transitional stage toward higher-level autonomous driving. The report notes that it has already established foundational capabilities for Level 4 autonomy in terms of data, models, and engineering systems. Various applications of Level 4 autonomous vehicles Future commercialization of Robotaxi, Robovan, and Robotruck services will largely depend on the data feedback loop formed through urban NOA deployment. The Bluebook projects that by 2030, China’s Robotaxi market will reach approximately $38.1 billion, with penetration rising to 11.9%, above the global average. In terms of technical pathways, high-definition map-based systems led by Waymo are developing in parallel with data-driven, mapless approaches promoted by Tesla and Momenta.