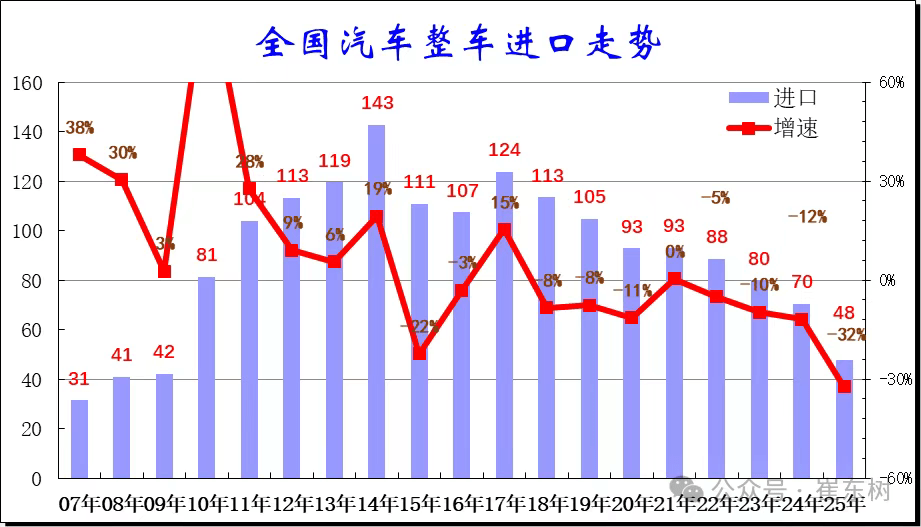

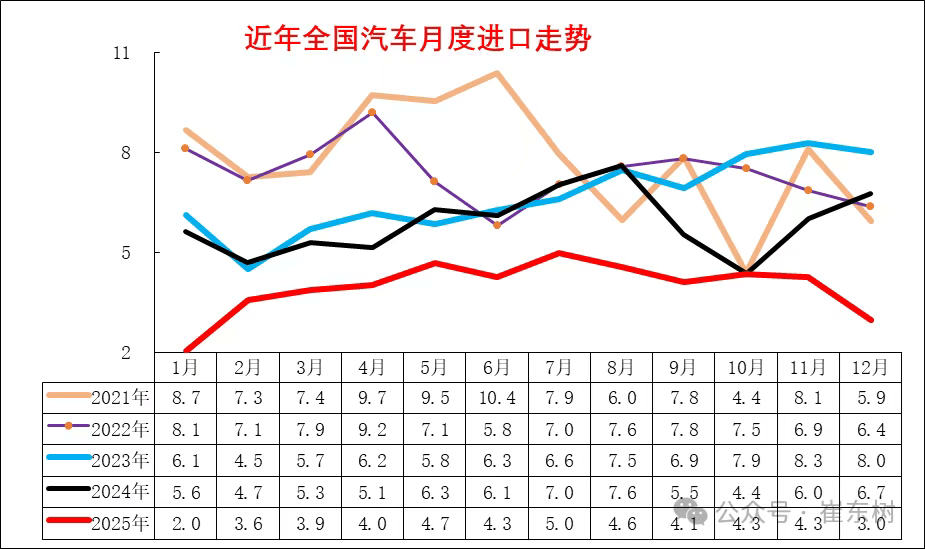

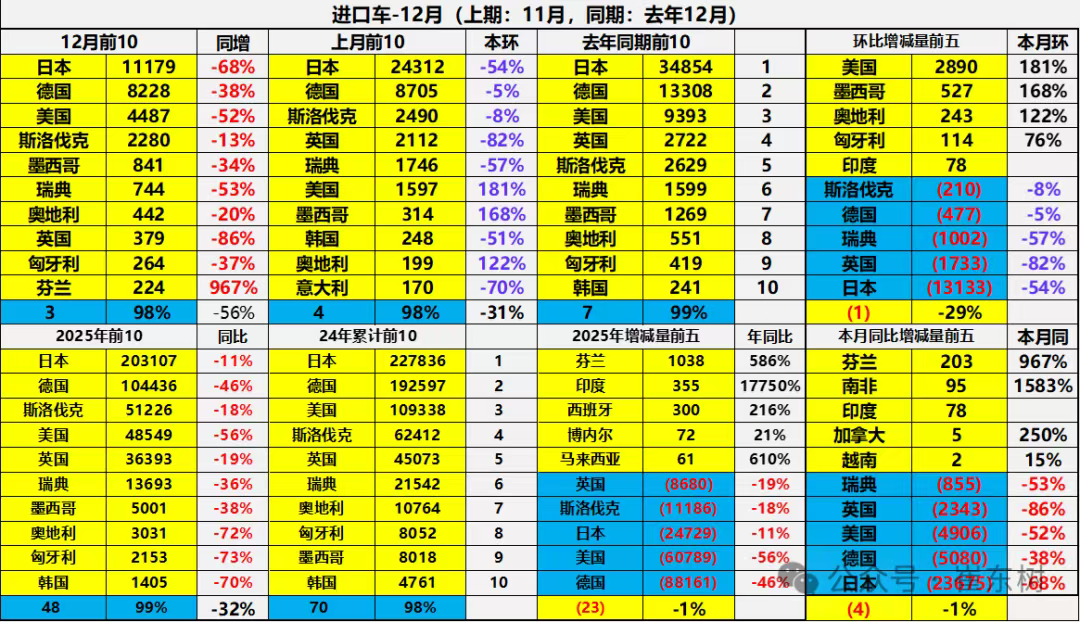

Japan, Germany, the United States, Slovakia, and the United Kingdom remain the core source markets for China’s passenger car imports. Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA), released an analysis report on China’s imported vehicle market for the period from January to December 2025. The data shows that from January to December 2025, 480,000 vehicles were imported, a year-on-year decrease of 32%. This represents a rare and significant decline for a full January-December period in recent times. Specifically, 30,000 vehicles were imported in December, reflecting a 56% year-on-year drop and a 30% decrease compared to November. Looking at the overall market trend, imported vehicle numbers peaked at 1.43 million units in 2014 before entering a downward phase. The import volume continued to shrink sharply in 2024, with only 700,000 vehicles imported for the full year, a 12% year-on-year decline. Trend of National Vehicle Imports Examining more detailed monthly data, the first half of 2024 showed normal seasonal trends, with a relatively good recovery in imports from June to December. However, as expectations for additional import tariffs did not materialize, imports plunged sharply in September and October 2024, indicating significant pressure on high-end consumption. Many dealers had been waiting to destock in anticipation of potential tariff hikes. The report points out that entering 2025, import vehicle data at the beginning of the year showed a shocking decline. As China-U.S. trade relations became more predictable, imports gradually recovered, hitting a new high for the year in July. However, with the rise of domestic high-end brands, imported vehicle numbers remained sluggish from August to November, followed by an abnormal drop again in December. Monthly Trend of Vehicle Imports This Year In the new energy vehicle sector, from January to December 2025, imported pure electric passenger vehicles fell by 79%, accounting for only 1% of the share; plug-in hybrid models dropped by 52%, also holding a 1% share; while hybrid models decreased by 25%, accounting for a 16% share. Regarding specific countries of origin, Japan, Germany, the United States, Slovakia, and the United Kingdom remain the core sources for China’s passenger car imports. Among these, Finland emerged as the fastest-growing market during this period, with an astonishing growth rate of 609%. The data shows that the top 10 source countries for imports from January to December 2025 are: Japan (203,107 vehicles), Germany (104,436 vehicles), Slovakia (51,226 vehicles), the United States (48,549 vehicles), the United Kingdom (36,393 vehicles), Sweden (13,693 vehicles), Mexico (5,001 vehicles), Austria (3,031 vehicles), Hungary (2,153 vehicles), and South Korea (1,405 vehicles). The report indicates that domestically produced vehicles were highly competitive in 2025. Imports of new energy vehicles from the major source countries declined by 62%. Monthly Trend of Vehicle Imports by Country From the perspective of specific imported brands, ultra-luxury imported models have shown a declining trend since 2023, which continued into 2025. Several brands, including BMW, Mercedes-Benz, Audi, and Porsche, all experienced negative growth in 2025. In contrast, Lexus’s import insurance retail data reached 184,000 units, representing a 3% year-on-year increase and achieving sales higher than in 2022. Cui Dongshu stated that the key factors behind Lexus’s sales success are its timely product adjustments and the strong performance of its hybrid models, which enjoy high recognition among consumers.

![[Gasgoo Express] NIO's William Li Discusses ES9 Design, Saying Originality is Difficult but Must Be Done; March Passenger Vehicle Exports Reach 695,000 Units](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pbWFnZWNuLmdhc2dvby5j-b20vbW9ibG9nby9OZXdzL1VFZGl0b3Iv-aW1hZ2UvMjAyNTA2MTAvNjM4ODUxNzAw-MTkzODM1OTU2NTQxNDEzNi5qcGc/c06991c2ffe2e05fe81c97062ebd8cf3.jpg?t=20260807&post_id=14615)