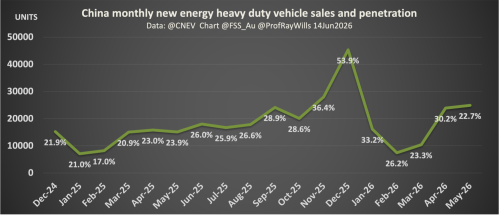

By Ray Wills and Peter Newman If the electric car was the opening chapter of China’s transport transition, battery-electric heavy trucks are the next — and it is now moving from promise to industrial reality. And this is happening inside the fastest energy transition in human history. For global oil, that matters: freight is diesel’s last great stronghold, and China is now eroding it at industrial scale. For years, heavy vehicles were treated as the hard bit: too big, too energy-hungry, too dependent on diesel, too exposed to freight economics. That story no longer fits the facts coming out of China. In late June, SANY Truck shipped 883 battery-electric heavy trucks through Guangzhou Port, the largest single export shipment of Chinese new-energy tractor trucks on record. That one shipment exceeded the entire Chinese industry’s export total for 2025, which stood at 877 vehicles. That is why this matters. It is not just another large order. It looks like a threshold event — the moment when China’s heavy-truck electrification shifts from a domestic experiment to an export industry, as it did for all vehicles six years ago. And we mentioned the fastest energy transition in human history. Targets as trajectories, not endpoints China’s new carbon-peaking action plan targets new energy vehicles at 30% of the national vehicle fleet by 2030, up from 12% at the end of 2025. It also calls for new-energy commercial transport vehicles to reach 25% of the fleet by 2030. Layered onto that is a dedicated heavy-truck implementation plan from 11 ministries aiming for 40% of new heavy-truck sales by 2030, and a fleet of more than 1.6 million new-energy heavy-duty trucks — roughly 20% of all heavy trucks on Chinese roads. The same plan promises about 3,000 dedicated charging and battery-swap stations and “zero-carbon highway” corridors where at least 18% of freight volumes are carried by new-energy trucks, rising to 80% electrification on fixed short-haul routes around Beijing. These are serious numbers. But in China, targets are rarely a destination; they are a trajectory — benchmarks that planning, local experimentation and industrial policy are expected to overshoot, not places to reach and rest. Six months that changed the heavy-truck story Changing incentives 1 January 2026 brought on a subsidy-distorted hangover pulled demand forward in a blockbuster December 2025, when new-energy heavy trucks briefly took more than half the market. Even so, first-quarter 2026 sales of new-energy heavy trucks still rose about 45% year on year to around 44,000 units, and reached roughly 27% of new heavy-truck sales. That penetration would be historic anywhere else; in China it was framed as a dip. Then momentum rebuilt. Between January 2025 and May 2026, cumulative sales of new-energy heavy trucks reached 337,000 units, pushing segment penetration above 29.5%. Other market summaries note penetration back above 30% in April and May after the early-year dip, confirming this is not just a subsidy story but an emerging new normal — one that starts to bite into diesel demand even before heavy trucks fully dominate new sales. This is the crucial point for global freight. China is not simply selling more electric trucks. It is building the industrial ecosystem that makes them cheap enough, rugged enough and scalable enough to take on diesel in ports, mines, construction sites, logistics hubs and, increasingly, line-haul freight. Place-based industrial strategy, not abstract “China” That ecosystem matters. Western commentary often speaks vaguely about “China,” as if it were one giant factory. But China’s industrial transitions happen in specific places. SANY’s trucks were built in Changsha, Hunan, and exported through Guangzhou, Guangdong, linking manufacturing, batteries, logistics and port infrastructure into one working corridor. Treating all this as simply “China” misses how regional industrial clusters drive speed and scale — and it is one small but telling symptom of what we’ve called “Western economists’ disease:” a recurring pattern in mainstream, largely OECD‑based analysis that systematically misreads fast, technological transitions in China, and therefore underestimates the speed and scale of change. In practice, this ‘disease’ turns China’s planned‑market trajectory — set out quite transparently in successive Five‑Year Plans — into evidence‑free macro stories about “failing fossil fuel consumption” proving a “weak economy” or “overcapacity,” when the main reason is an electro‑state clean‑energy transition. The economics are changing fast. Analysts cited in recent coverage say ownership costs for pure electric heavy trucks have moved close to parity with diesel after subsidies, at around 500,000 yuan (US$74,000) per truck. SANY estimates the latest export batch could save customers around 150 million yuan (US$22.1 million) a year in fuel and cut 80,000 tonnes of CO₂, before counting maintenance and noise benefits. Farms, freight, and energy sovereignty The same pattern is starting to appear well beyond Chinese highways, in agriculture and regional freight. China’s policies explicitly encourage new-energy trucks and machinery in mines, ports, airports and construction, and are beginning to touch medium and large farm vehicles as battery, motor and control systems scale and prices fall. Our report for Australian group Farmers for Climate Action’s Energy Sovereignty for Regional Australia makes the parallel point for Australia: looking into the 2030s, farms should be preparing to electrify heavier machinery and longer-haul transport as commercial products become available, and should be planning charging infrastructure and local storage to keep more energy value in regions rather than bleeding it out through diesel imports. China’s experience shows that once industrial clusters exist, suitable vehicles arrive faster than many planners expect. Planning, data and the bigger energy story None of this is accidental. China’s heavy-truck push is built on planning and data: multi-agency targets for sales and fleet shares, binding infrastructure numbers, corridor-level zero-carbon goals, and real-time monitoring of freight economics that can pivot subsidies, trade-in programs and electricity pricing as diesel and LNG markets start to fall away. While fossil prices spiked after the US attacked Iran, those levers further accelerated electrification; the six-month sales data are the result. The wider energy story matters too. China’s oil demand is softening not because its economy is collapsing, but because electrification is now large enough to bite into diesel as well as petrol, alongside renewables meeting all growth in electricity demand and pushing coal generation into decline. Heavy trucks are emerging as the next big lever in that shift. Western economists’ disease is key: if we keep reading China only as “weak demand for oil” instead of as “strong supply of electric freight solutions,” we will mis-diagnose the transition and mis-design our response. We will argue about export volumes while the next freight system is being built somewhere else. Heavy trucks are emerging as the next big lever in that shift. For the oil system, that means the last big block of diesel demand is now exposed to the same kind of rapid, China‑driven disruption that hit petrol cars and coal‑fired power. What seemed improbable only a few years ago — battery-electric heavy trucks outselling diesel in the world’s largest market — is now normal enough to be loaded onto ships by the hundreds. China’s electric truck moment has arrived. And if the trajectory so far is any guide, this chapter of the transition is only just getting started. Ray Wills is an adjunct professor at UWA and director of Future Smart Strategies, where he spends his days chasing charts that prove the dragon really has woken up delivering clean tech. Peter Newman is a professor of sustainability at Curtin University and IPCC lead author, still happily providing evidence that electric wheels are rewriting the world’s transport story.