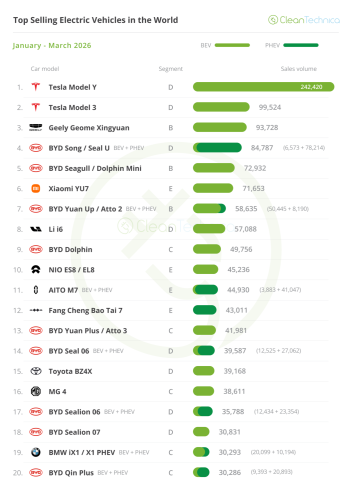

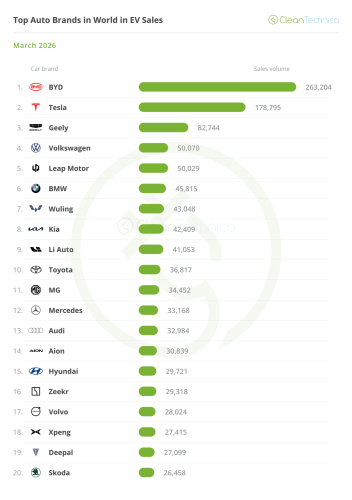

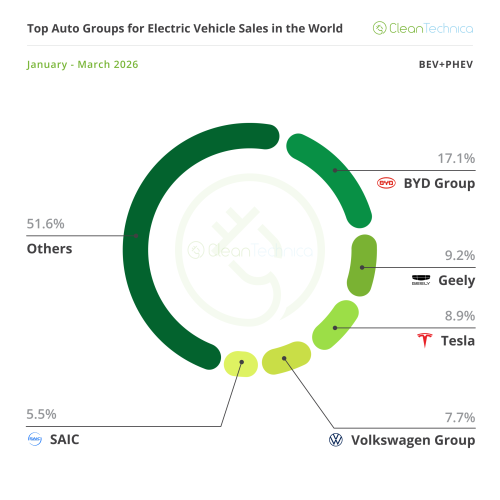

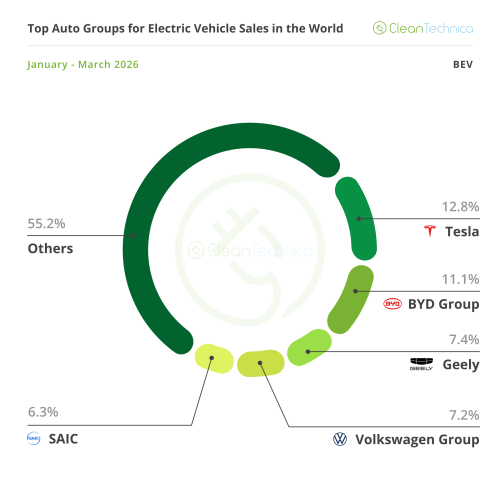

Tesla wins gold and silver in a market running at different speeds. BEVs vs. PHEVs Plugin vehicle registrations were up 5% year over year (YoY) in March, ending the month at around 1.7 million units. Interestingly, BEVs (+12% YoY) and PHEVs (-8% YoY) behaved very differently, with pure electrics back to double-digit growth while plugin hybrids remained in the red, which is the first time since the COVID era that PHEVs remained in the red for a full quarter. This meant that, while the plugin YTD numbers remain negative (-2% YoY), that is solely due to the PHEV blues (-10% YoY), because BEVs are already positive (+2%). And the different dynamics between pure electrics and plugin hybrids are reflected in the BEV vs. PHEV share of plugin sales — in March, BEVs represented 72% of all plugin sales, or about 1.25 million units, one of the best results of the past few years. That led the YTD breakdown to be 69% vs 31% in favour of pure electrics, which is touching the ceiling of BEV share of the past 12 years, as since 2014, BEVs have floated between 70% and 50% of the total plugin share. Does this mean that BEVs are ready to replace PHEVs on the market? With some BEVs (from BMW, Mercedes, Lucid, etc.) now having comparable range to ICE cars, and others (from BYD, Geely, and others) charging as fast as it takes to refuel ICE models, the question is no longer about technology, but scaling up and reducing costs. China and the USA vs. the rest of the world Still, even with numbers out of the red zone, it is undeniable that globally, this year started slow. But there is one easy explanation for this — incentives. Or the end of them. The end of US incentives last October, added to the partial removal of incentives in China at the end of 2025, had an expected impact, as these are the 3rd and 1st largest EV markets, respectively. Actually, if we remove China and the USA from the tally, EVs have jumped 47% YoY globally in March, with BEVs surging even faster (+54%). The same contrasting trends are also visible in the YTD numbers, with the 2% global drop being transformed into a 43% growth rate if we remove the two countries. Just because certain media-friendly markets are down, that doesn’t mean that all markets are down. Here are a few examples of fast growing markets: Croatia is up 282% this year, New Zealand is up 263%, India is doubling its sales, Malaysia is experiencing tripling sales, Australia was up 89% in March, and I am not even mentioning Latin America, where growth is being so well documented by my CleanTechnica colleague Juan Diego…. So, Keep Calm and Carry On — despite contrasting trends in China and the USA, the EV Revolution is in good health, and with what is happening in the Middle East, ICE vehicle sales are going to melt even faster. EV Shares Share-wise, March saw BEVs end the month at 19% share, with the tally increasing to 26% if we add in PHEVs. This performance pushed the 2026 plugin share upward, because BEVs increased their share by two points, to 14%, while plugin hybrids also recovered slightly, going from 5% in February to their current 6% share. Therefore, the 2026 PEV share is now at 20%. For reference, 2025 market share ended with BEVs at 17% share and all plugin vehicles combined at 26%. Although we are still far from those results, comparing where we are now to where we were twelve months ago, the difference is much smaller (21% PEV share then vs. 20% now), so I am expecting that the second half of the year will bring robust growth again, with BEVs probably north of the 20% share barrier by the end of the year. In these less positive months, it is also good to look back and see how far we have come along in the EV Revolution. Five years ago, at the end of Q1 2021, while we were still in the midst of the COVID pandemic, plugins were at 6% share (4% for BEVs alone), less than a third of where we are now. Ten years ago, in the first quarter of 2016, the plugin share was at … 0.9%! Yep, not even 1%. Looking at the best selling models, with the Chinese market still recovering, it was a great opportunity for others to shine, and none have done it better than Tesla, which took the #1 and #2 spots in March! Still, the leader Model Y and runner-up Model 3 had contrasting performances YoY. While the crossover grew 35% YoY to 118,531 units, no doubt helped by the six-seat L version and the mass delivery of the cheaper “Standard” version, the sedan saw its sales drop by 10% YoY — to 53,158 units. So, while mass delivery of the “Standard” version helped sales, I guess the wrinkles of being nine years on the market, no matter the facelifts it’s had in the meantime, are starting to impact sales. Still, this was enough to keep the competition behind it, like the Geely Xingyuan (EX2 in export markets), which completed the podium with some 34,000 registrations. Geely’s small EV is now at cruising speed, compensating for the loss of demand in its domestic market with increased exports. One surprise at the top half of the table was the 5th position of the BYD Yuan Up/Atto 2. Thanks to a recent refresh and the launch of a new PHEV version, it scored a record 33,934 registrations in March, almost becoming the best selling BYD. Within its company tent, it was just surpassed by the BYD Song/Seal U, which is in the midst of a renaissance. The new Ultra body is bringing major innovations, namely the much hyped Flash Charging. Expect the Song to recover sales in the coming months thanks to this new Ultra version. Another highlight in the first half of the table goes to Li Auto’s i6, which scored a record 24,198 registrations, allowing it to reach the 7th spot. Meanwhile, BYD’s pack is back populating the top 10, with six representatives in the top half of the table. Looking at the second half of the table, the tiny Wuling Mini EV is back in the top 20, at #12, but the highlights are elsewhere: Toyota once again placed the BZ4X in the top 20, thanks to 15,683 registrations, it’s second record score in a row. Thanks to the recent refresh, which, among other things, lowered the price and finally gave it decent specs, as well as a global presence, the Japanese SUV was again the best selling legacy model. Sales were distributed across a number of markets, with its three highest volume markets being the USA, Japan, and Canada. Another record scorer was the #13 Deepal S05, with Changan’s premium crossover delivering a best ever 16,395 units, and while most units were delivered in its home China, over 2,000 units were exported and delivered elsewhere, across very different markets, like Israel (329 units), Spain (235), Thailand (501), and Colombia (258). Outside the top 20, the highlights come from Asia. Changan’s mainstream cousin to the Deepal S05, the Qiyuan/Nevo Q05, ended some 400 units behind a top 20 position, thanks to a record 13,122 registrations. The Kia EV3 (10,622 units) had its best result in a year — with the majority of sales coming from just two markets (South Korea and the UK). Meanwhile, the Zeekr 9X land yacht is continuing to rise, having scored its first five-digit result ever (10,073 units). With Geely’s flagship EV set for export markets in the second half of the year, expect this $68,000 mammoth of an SUV to continue scoring 10,000-plus results throughout the rest of the year. Year to date, the big news is that the Tesla Model 3 profited from its peak month of the quarter to jump three positions, into the runner-up spot. That meant Tesla won gold and silver. Still, with the #3 Geely Xinguan fewer than 6,000 units behind and the #4 BYD Song set for a revival soon, it will be difficult for the Model 3 to retain a podium position, let alone the silver medal. Below the podium race, the BYD Seagull was up one position, to 5th, while the BYD Yuan Up jumped seven positions, into the 7th spot. In fact, the top 20 saw a global BYD surge, with six models climbing positions(!) — besides the aforementioned Seagull and Yuan Up, the Dolphin hatcback jumped to 9th, the Seal 06 sedan/station wagon is now #14, the Sealion 06 SUV was up to #17, and there was still time to see the good ol’ Qin Plus return to the table, at #20. Yep, after a small disruption in the first two months of the year, things are returning to normal. Manufacturers: Kia shines in a normal month Nothing really out of the ordinary happened in the top positions, with BYD, Tesla (+18% YoY), and Geely taking over the podium, followed by #4 Volkswagen. Still, behind the German make, Leapmotor is already warming up, ending March in 5th, just 31 units behind Das Auto. With a slew of fresh metal coming in (A10 small crossover, A05 small hatchback, D19 large SUV, D99 large MPV…), expect its sales to grow significantly, not only surpassing the main B-League players (Volkswagen, Wuling, BMW…), but possibly even reaching the back of 3rd placed Geely. Still, the highlight was the Korean Kia, which ended the month in 8th with a record 42,409 registrations. With the EV3 (10,600 units) and EV5 (8,000) being the backbone of Kia’s strength, and with a few models either ramping up (PV5) or being introduced (EV2), one can be optimistic about Kia’s prospects for this year. Regarding the remaining positions on the table, another surprise was Toyota’s 10th position, and with a record to boot (36,817 registrations) thanks to great performances from the BZ4X (15,700 units) and its smaller sibling, the China-based BZ3X (8,000 units). Will 2026 be the year that the giant awakens? I mean, it feels strange to celebrate a top 10 presence in the EV arena when you are the best selling automotive brand in the world…. Still in record-land, #11 MG had a record month, with SAIC’s mainstream brand scoring 34,452 registrations, half of them coming from the MG 4. Finally, we have #20 Skoda. The Czech make scored a record 26,458 registrations, not bad considering you have a lineup with only two BEVs and two PHEVs. But help is on the way, with Skoda launching two new BEVs this year, the small Epiq crossover and the large Peaq SUV. Expect both to add significant volume to the brand’s tally. We should continue to see the Czech brand breaking records and being a familiar face on the table. As for the year-to-date table, there was no major news in the top positions, and we have to go down to the 7th position to see position changes. And there were a lot of them…. Most of them were thanks to the AITO/Xiaomi debacle. Due to a slow March, when both of them were unable to break into the month’s top 20, they lost several positions on the YTD table, to the profit of many other brands. As such: Li Auto profited from that debacle and the i6 success to jump three spots and go up to 7th; Kia profited from its record month and surged five spots, into 8th; #9 Toyota and #10 Mercedes also profited from strong results and the AITO/Xiaomi’s fall to jump two positions; As for Zeekr, the 9X success is propelling the brand upwards, having climbed three positions to #11. Below all these changes, Audi and MG were up also, with the German going up two spots, to #13, and MG going up three spots, to #15. A final mention to Fang Cheng Bao, which ended at #21 with 62,542 registrations. With exports now starting to gain relevance, BYD’s premium arm could gain enough momentum to join the table soon. Looking at OEMs, BYD (17.1%, down from 17.3% in February 2026) is stable in the lead, while runner-up Geely (9.2%, down 1.3%) lost significant share, as a number of its brands (Volvo, Lynk & Co, Smart…) aren’t performing as expected. On the other hand, Tesla (8.9%, up from 7.8% in February) profited from its March quarterly peak to recover lost ground, having surpassed Volkswagen Group (7.7%, down 0.5%) and returned to the OEM’s podium. #5 SAIC remained in 5th, despite losing some share (5.5%, down from 5.8% in February). This could serve as an incentive to those outside the top 5, namely #6 Hyundai–Kia (4.2%), which is closer to the Shanghai OEM than #7 Chery, #8 BMW Group, and #9 Changan. Comparing with Q1 2025, the top 5 was exactly the same, but BYD’s market share was far higher (24.2% then vs. 17.1% now). Below it, Geely was also in a better place (11.2% then vs. 9.2% now), unlike Tesla, which improved its market share by 0.7% (8.9% now vs. 8.2% then). Has Tesla bottomed out? As for #4 Volkswagen Group and #5 SAIC, they are roughly in the same place as they were a year ago. Looking at the German OEM in particular, this performance could mean that in a fully plugin automotive market, they could sell some six million units every year, which doesn’t sound bad … until you consider that Volkswagen Group sold close to nine million units in 2025. So, a third of it sales lost. Still, it’s painful, but it’s not life threatening. Others (GM, Stellantis, Honda, Nissan) are quite worse — for these, the next few years will be a matter of life or death. Looking just at BEVs, there were 2.8 million registrations in the first three months of 2026, or 69% of total plugin sales. Will they end the year above 70%? If so, that would be a first since 2014. At the top, Tesla (12.8%, up 1.1%) profited from its peak month of March to extend its lead to 1.7% share more than runner-up BYD (11.1%), which itself was up 0.5% share in March, and should continue rising in the coming months. Tesla’s lead shouldn’t last long, though. It could even end during Q2…. With buyers waiting for BYD to launch the second generation of its Blade Battery, expect sales to pick up again soon, as it seems the Shenzhen OEM is all in on its new battery tech and that should allow it to easily regain the leadership position. In 3rd place we have a receding Geely (7.4%, down from 8.8% in February), which is placing it within the target range of #4 Volkswagen Group (7.2%, down 0.5% share). Meanwhile, #5 SAIC (6.3%, down 0.3% compared to February) should start keeping a close eye on #6 Hyundai–Kia (5% share), which is steadily closing the gap to it. Comparing to where we were a year ago, the biggest change is that Tesla is now in the lead, while a year ago, it was BYD holding that position. The remaining top 5 looked the same as now.