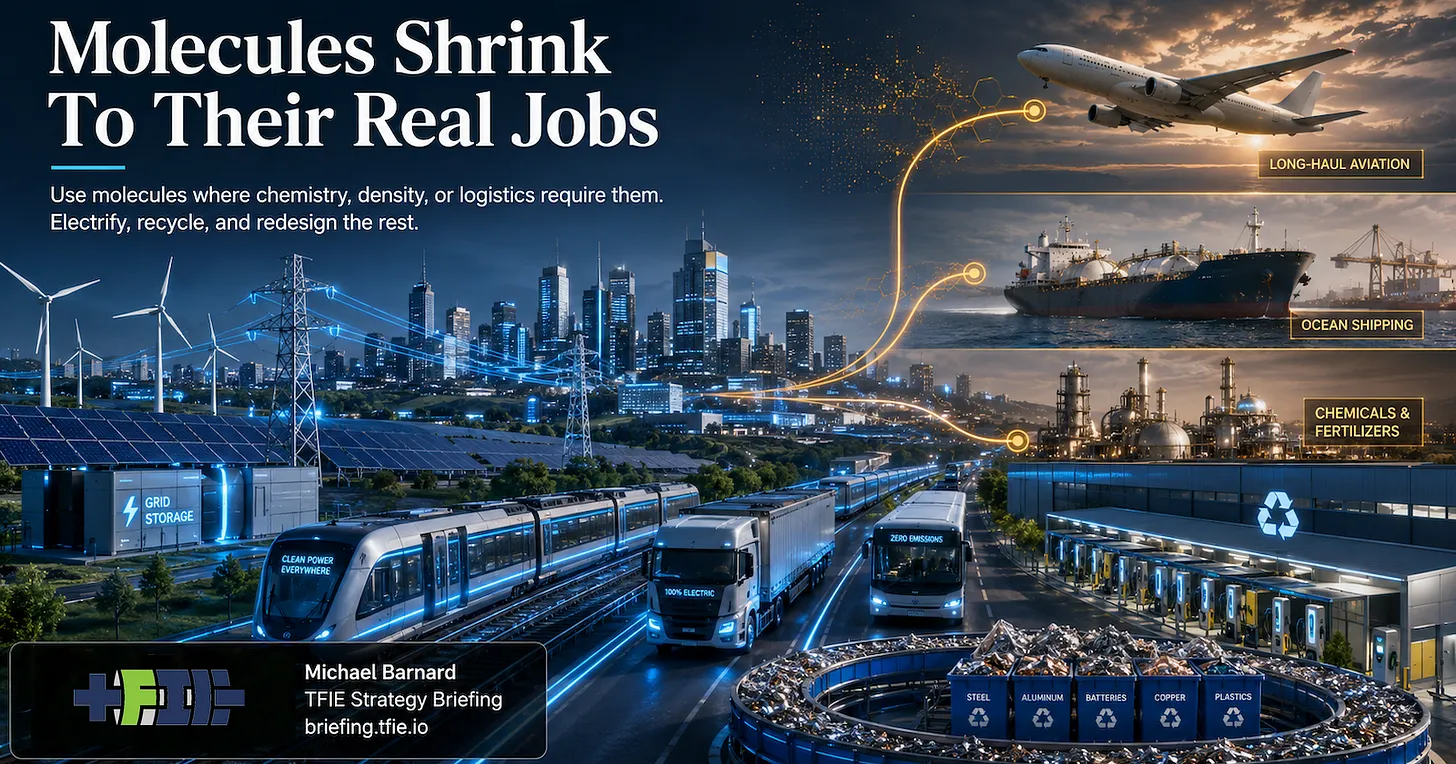

A lot of energy-transition arguments begin with today’s fossil fuel demand. Coal, oil, and gas still dominate global primary energy, so it is tempting to draw a straight line from the current fuel system to a future molecule system. Replace natural gas with hydrogen. Replace bunker fuel with ammonia or methanol. Replace jet fuel with synthetic liquids. Replace diesel with biofuels. Keep the basic market map and change the label. That is attractive for project decks, but it is a poor way to think about the transition. The better starting point is the service being delivered. Buildings need heat, not gas. Cars and trucks need motion, not gasoline or diesel. Grids need reliability and storage, not necessarily hydrogen. Industry needs heat, force, separations, chemistry, and materials, not a generic bucket called “molecules.” Once the question is framed around useful work instead of existing fuel sales, direct electricity, efficiency, demand shifts, and system redesign remove a large share of the apparent market before alternative fuels get to compete. Buildings are the simple example. A gas furnace does not create a permanent market for renewable gas or hydrogen. It creates a heat demand. Heat pumps serve that demand with electricity and move several units of heat for every unit of electricity consumed. Insulation, district systems, and better controls help in the right places, but the big decarbonization move is usually replacing combustion with an electric machine. The future molecule market for ordinary building heat is therefore much smaller than today’s gas market. Road transport follows the same pattern. Internal combustion vehicles created a vast liquid-fuel market because oil was energy-dense, portable, cheap, and backed by a century of infrastructure. Electric drivetrains change the physics and the economics. They are more efficient, mechanically simpler, and increasingly supported by cheaper batteries and expanding charging networks. There are edge cases, slow-moving segments, and regional differences, but the main direction is clear. Most road transport is moving to batteries rather than waiting for hydrogen, synthetic diesel, or biofuels to become cheap. Electricity storage is another place where the molecule story often gets ahead of the system case. Hydrogen can store energy, but capability is not the same as a large market. Round-trip losses, compression, storage, reconversion, infrastructure, maintenance, and safety all have to be paid for. Batteries have taken much of the short-duration market. Pumped hydro remains the bulk-storage reference class where geography allows it. Transmission, demand response, interregional balancing, and renewable overbuild reduce the size of the residual problem. Hydrogen may have some roles, but it does not inherit the storage category simply because it is a molecule. Industry is more mixed, which is why it attracts so many vague claims. Many industrial loads are motors, pumps, compressors, low- and medium-temperature heat, material handling, and process steps that can be electrified directly. Some high-temperature processes and chemical feedstocks still require molecules or specific reductants, but those are narrower claims than the broad “industry is hard to abate” framing used in many pitches. Hard to abate should be the beginning of the analysis, not the conclusion. Shipping and aviation are where molecules keep more real work. Long-haul aviation will need high-energy-density liquid fuels for the foreseeable future. Some long-range shipping will continue to need liquid fuels, especially where batteries and shore power cannot cover the operational profile. Chemical feedstocks also remain real. Fertilizers, petrochemicals, some steel pathways, parts of cement, and other industrial systems have specific chemistry and process constraints that cannot be wished away with a charging cable. There are molecule jobs that direct electricity does not do well, and those deserve serious attention. That is precisely why the denominator matters. The residual molecule market is not today’s fossil fuel market with different labels. It is what remains after heat pumps remove most building combustion, electric vehicles remove most road liquid fuels, electric motors and grids remove large amounts of industrial combustion, batteries and pumped hydro take major storage segments, ports and rail electrify, and efficiency reduces total energy throughput. The remaining molecule pool is smaller, more specific, and more expensive to serve well. The policy implication is straightforward. Governments should not treat every low-carbon molecule as strategically important merely because fossil fuels are strategically important today. Hydrogen for fertilizer feedstock is not hydrogen for home heating. Sustainable aviation fuel is not synthetic diesel for cars. Biomethanol for some shipping niches is not a broad claim that all marine fuel becomes green molecules. Renewable gas for a narrow industrial process is not a reason to keep gas distribution networks alive for ordinary buildings. The investment implication is just as direct. A pitch that starts with today’s fossil fuel consumption and claims even a small percentage of it as the future market may still be overstating the opportunity. The correct market is not today’s fuel demand. It is residual molecule demand after electrification, efficiency, infrastructure maturity, and system redesign have reduced the fuel pool. Molecules do not disappear in the transition. They shrink to their real jobs, and that is a much harder market for weak hydrogen, ammonia, synthetic fuel, biofuel, and LNG claims to survive. A longer maintained version of this analysis is available at TFIE Strategy Briefing: Molecules Shrink To Their Real Jobs, part of Michael Barnard’s broader WorldView work on the assumptions underneath serious 2100 transition scenarios.