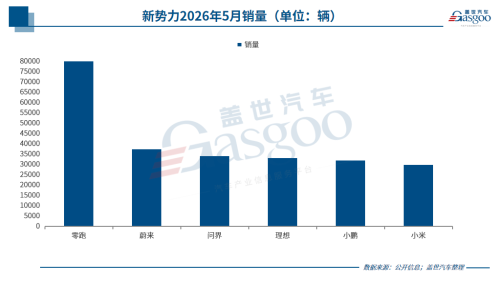

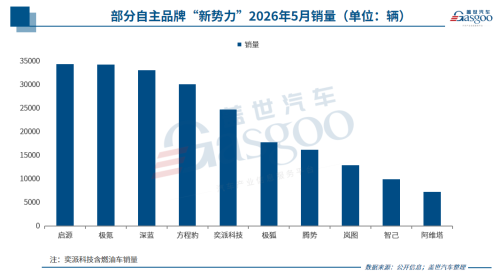

Gasgoo Munich- As June began, automakers released their sales scorecards for May 2026. Forecasts from the China Passenger Car Association (CPCA) on May 23 project Chinese retail sales of new energy passenger vehicles at 950,000 units, with a penetration rate of roughly 62.5% — a record high. The data underscores the deepening electrification transition, as the NEV market shifts steadily from policy-driven growth to market-driven demand.A closer look at the numbers reveals a sharp divergence among the top startups in May: Leapmotor surged past 80,000 monthly sales, establishing a commanding lead. Meanwhile, traditional automakers like BYD, Changan, and Geely saw their self-incubated NEV brands collectively gain traction, accelerating the payoff of their multi-brand matrix strategies.Startup Matrix: Leapmotor Clears 80,000 to Lead the Pack, While Rivals Crowd the 30,000 BracketThe startup market in May displayed a distinct tiered structure. Leapmotor broke the 80,000-unit barrier to claim the top spot, while NIO leveraged a three-brand strategy to reach 37,700 units. Li Auto, XPENG, Xiaomi, and AITO clustered in the 30,000 to 35,000 range, forming the fiercely competitive core of the battlefield.Image Source: LeapmotorLeapmotor emerged as the undisputed highlight in May. Official data shows deliveries across its entire lineup hit 81,569 units — an 81% year-on-year surge and a 14.26% month-on-month increase. This marks a new monthly record for the brand, making Leapmotor the first Chinese startup to crack the 80,000-unit delivery threshold in a single month.By model, the Leapmotor A10 surpassed 20,000 deliveries in a single month, while new orders for the D19 remained above 10,000. Global cumulative sales of the C-series have exceeded 800,000 units. By the end of May, Leapmotor's cumulative deliveries for the first five months of the year had surpassed 300,000 units.Leapmotor has set an ambitious sales target of 1.05 million units for 2026, driven by Chairman Zhu Jiangming's strategic goal of "sprinting to a million units" by that year. With the refreshed C-series launching in June, the D99 opening for pre-orders, and the Lafa5 scaling up for export, Leapmotor is poised to challenge the 90,000-unit monthly delivery milestone.Image Source: NIONIO also delivered a solid performance in May. Data shows the company delivered 37,705 new vehicles — a 62.3% year-on-year jump and a 28.4% increase from April.NIO's growth stems from the synergistic effect of its three-brand strategy. The main NIO brand delivered 20,013 units, up 50.8%; the Onvo brand delivered 12,029 units, surging 91.5% year-on-year and a massive 124.8% month-on-month; and the Firefly brand delivered 5,663 units, up 53.9%.On the product front, the flagship NIO ES8 sold 11,475 units, maintaining competitiveness in the premium market above 400,000 yuan. By the end of May, NIO's cumulative deliveries for the year reached 150,500 units, a 68.7% increase, bringing its total historical deliveries to 1.148 million units.Li Auto delivered 33,350 units in May, pushing its historical cumulative total to 1.703 million units by the end of the month. Chairman and CEO Li Xiang noted that deliveries have been on a growth trajectory since the first quarter. The Li i6 has surpassed 20,000 deliveries for three consecutive months, securing a spot in the top three for pure electric SUVs. In May, the all-new Li L9 was officially released and deliveries began, marking the start of a new replacement cycle for the L-series; the new L9 Livis garnered over 10,000 orders within two weeks of launch.Image Source: XPENGXPENG delivered 32,158 units in May, up 3.7% from April and marking its highest monthly delivery figure since 2026. This growth was driven by sustained momentum across its existing product lineup. The 2026 P7+, G6, G9, and G7 Super Range Extender versions have completed their production ramps, while the MONA M03 continues to sell well in the 150,000-yuan pure electric market.On May 20, the new tech flagship XPENG GX officially launched and began deliveries. Offering both pure electric and super range-extender powertrains across eight models, the vehicle secured 24,863 firm orders within 12 hours, with the Ultra flagship variant accounting for over 80% of the total.Xiaomi Auto's deliveries remained above 30,000 units in May, holding firm above the 30,000 mark for a second consecutive month. The company has evolved from relying on the single SU7 model to a dual-line product structure featuring both the SU7 and YU7 series.By the end of May, Xiaomi Auto's cumulative deliveries for the first five months reached approximately 140,000 units, fulfilling 25.5% of its annual 550,000-unit target. While maintaining monthly sales above 30,000 units is impressive for a player that entered the market just over two years ago, the company still faces challenges: it will need to average roughly 55,000 monthly deliveries in the second half to meet its full-year goal.Image Source: Harmony Intelligent Mobility AllianceIn May 2026, Harmony Intelligent Mobility Alliance (HIMA) achieved 46,122 deliveries, marking year-on-year and month-on-month growth. AITO delivered 34,320 units across its entire lineup in May, up 48.2% from April, with cumulative January-to-May sales rising 28.7% year-on-year.The all-new AITO M9 garnered over 20,000 firm orders within 24 hours of launch, with immediate deliveries available. Meanwhile, the AITO M6 surpassed 20,000 deliveries in its first month on sale.In terms of competitive dynamics, excluding Leapmotor, the delivery gaps among the other startups are narrow, with rankings liable to swap at any time in a highly fluid landscape. This "30,000-unit cluster" reveals that breaking through 30,000 is one thing, but standing firm at 40,000 is another hurdle — one that tests the depth of product matrices as well as supply chain management and delivery systems.Chinese NEVs: Multi-Brand Synergy Drives Shift into Fast LaneThe in-house NEV brand matrices of traditional automakers also turned in a strong performance in May. Overall data released by major vehicle groups indicates that the steady rise in penetration rates is translating into tangible sales volume.Image Source: BYDBYD sold 383,000 vehicles in May, leading the industry, with passenger car sales totaling 377,000 units. The Dynasty and Ocean networks sold 330,200 units, remaining the cornerstone of BYD's sales. Fang Cheng Bao sold 30,186 units; Denza sold 16,303 units; and Yangwang sold 286 units.Overseas, BYD exported a total of 160,600 new energy vehicles in May, an 80.7% year-on-year jump and another record high.Geely Auto's total group sales reached 238,000 units in May, marking three consecutive months of both year-on-year and month-on-month growth. New energy vehicle sales for the month hit 133,000 units, accounting for 56.1% of total sales and staying above the 50% threshold for four months running.Its ZEEKR brand delivered 34,377 units in May, an 81.8% year-on-year surge and another record high. Models like the ZEEKR 009, 9X, and 8X accounted for nearly 50% of the mix, driving the brand's average transaction price up by 52.4% year-on-year, solidifying its position in the luxury camp.The Lynk & Co brand sold 20,732 units in May, with new energy sales reaching 14,688 units — a 17% month-on-month increase. New energy vehicles accounted for a staggering 71% of its sales.Image Source: Changan AutoChangan Auto delivered 209,000 units globally in May, including 92,000 new energy vehicles. Its electrification transformation is characterized by multiple brands advancing in parallel: Changan NEVO delivered 34,528 units, with the new Q05 contributing 15,812 units and securing over 3,000 orders within three days of launching in Thailand. Deepal recorded global sales of 33,243 units in May, up 30% year-on-year, with overseas sales for January through May totaling 28,704 units, a 167% jump. Avatr delivered 7,336 units in May, maintaining an upward trend. Reviewing monthly data, Avatr has climbed steadily from 2,216 units in January to 7,336 in May, demonstrating clear growth momentum.SAIC Motor sold 349,000 vehicles in May, including 182,000 new energy vehicles, a 46.49% year-on-year increase. Its IM Motors brand delivered 10,023 units in May, holding steady above the 10,000-unit mark for a second month, with cumulative January-to-May sales up 115%. SAIC Passenger Vehicle's NEV sales reached 174,000 units in the first five months, surging 195%, while the MG4 family surpassed 10,000 sales in eight months.Image Source: eπ TechnologyDongfeng's in-house new energy brands also performed well. Dongfeng eπ Technology delivered 24,830 units in May, up 42% year-on-year, with cumulative deliveries of 109,600 units for January through May and overseas sales up 194%. Voyah delivered 13,003 units in May, a 30% increase, bringing its cumulative five-month total to 62,041 units, up 35%.The HYPTEC Aion BU recorded sales of 33,140 units in May, up 23.76%, with the Aion i60 consistently selling over 10,000 units monthly. Arcfox sold 17,943 units in May, up 32.82%, delivering steady performance driven by models like the Alpha S5 and Koala. The pre-launch of the Arcfox Beta S3 and the release of the V9 in May are expected to further bolster overall sales.Conclusion:Across the industry, the NEV penetration rate hit roughly 62.5% in May, another record high. Domestic brands have become a major market force, with traditional automakers demonstrating their late-mover advantage: Geely's NEV share exceeded 56%, Changan's NEV sales approached 100,000 units, and SAIC's NEV sales grew by over 46%. Yet one issue cannot be ignored: while multi-brand matrices cover diverse market segments, they also face the challenge of resource integration and managing internal competition.Looking ahead, as multiple new models enter the delivery cycle, the NEV market is poised for continued growth. Can Leapmotor hold onto its dominant position? And which brand will be the first to break away from the 30,000-unit cluster? These will be the key storylines to watch.