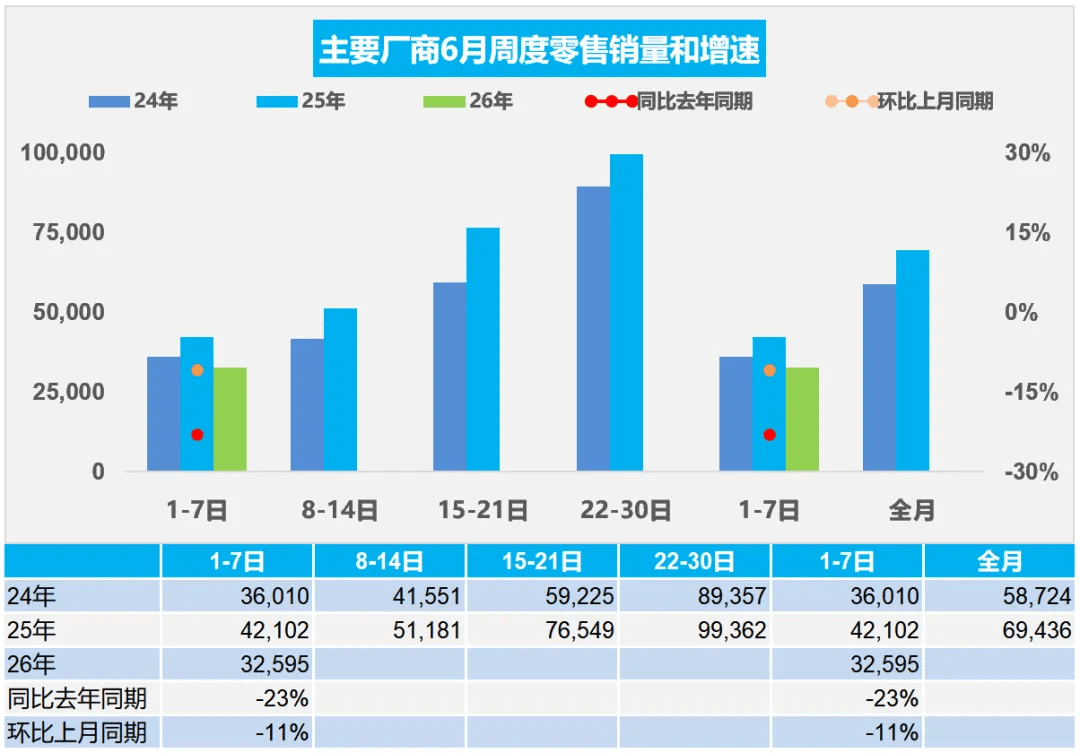

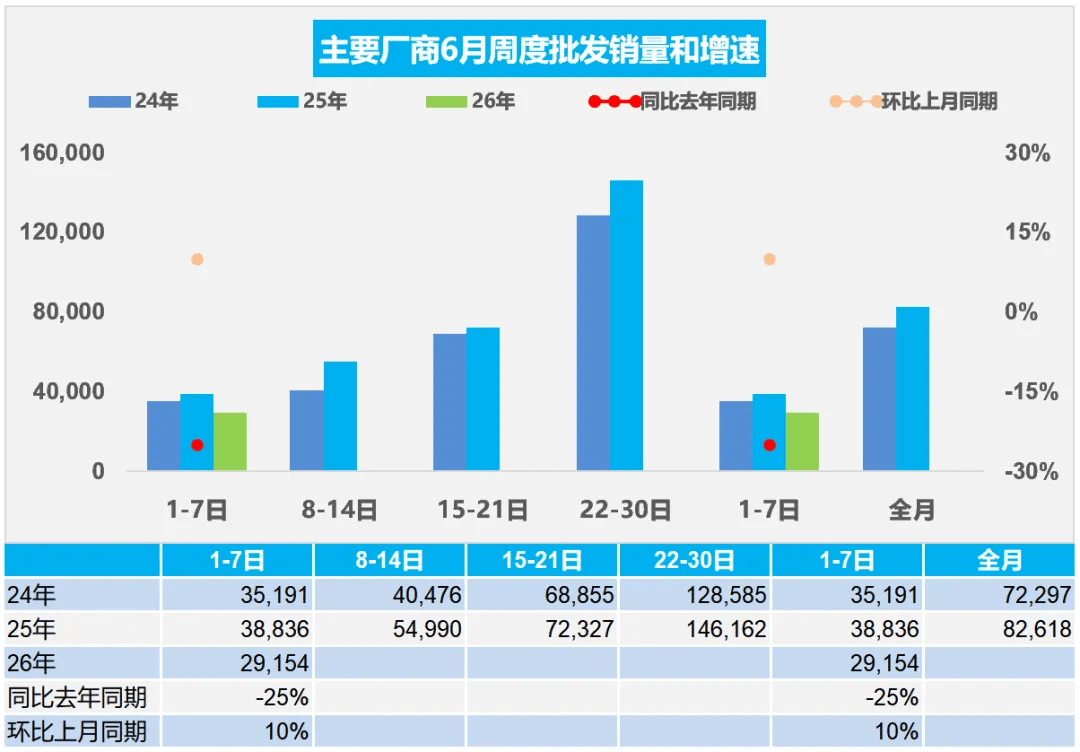

According to the latest data released by CPCA, nationwide passenger vehicle retail sales totaled 228,000 units during June 1–7, down 23% year-on-year and 11% from the same period last month. On a cumulative basis, retail sales reached 7.327 million units so far this year, down 20% year-on-year, indicating that the broader market remains in an adjustment phase. Weekly sales volume and growth rates in June 2024, 2025, and 2026 During the same period, passenger vehicle wholesale sales totaled 204,000 units, down 25% year-on-year but up 10% from the previous month. Cumulative wholesale volume reached 10.39 million units, down 6% year-on-year. Despite weakness in the overall market, NEVs remained the primary pillar supporting vehicle demand. NEV passenger vehicle retail sales reached 152,000 units in the first week of June, down 14% year-on-year but up 8% from the corresponding period of the previous month. More notably, NEV penetration rose to 66.7%, surpassing the previous record high of 62.9% set in May. The wholesale market also maintained a high NEV share. NEV passenger vehicle wholesale volume reached 137,000 units during the week, down 6% year-on-year but up 17% month-on-month, with penetration reaching 67.2%. Weekly wholesales volume and growth rates in June 2024, 2025, and 2026 The figures suggest automakers are continuing to allocate a larger share of production capacity and channel resources toward electrified models. On a year-to-date basis, cumulative NEV passenger vehicle retail sales reached 3.85 million units, down 15% year-on-year, while cumulative wholesale sales totaled 5.444 million units, up 2%. From the production side, output of conventional internal-combustion-engine light vehicles fell to 108,000 units during the first week of June, down 39% year-on-year while rising 8% from the previous month. By comparison, production of hybrid and plug-in hybrid vehicles reached 69,000 units, down 15% year-on-year and 6% month-on-month. As traditional gasoline-powered vehicle production continues to contract, NEVs are increasingly becoming the focal point of automakers’ investment and capacity allocation strategies. Since the start of the second quarter, factors including rising raw material prices, fuel price fluctuations and supply-chain cost changes have continued to affect automakers’ operating conditions. The CPCA expects the overall market to maintain a pattern of sequential improvement but year-on-year weakness in June, suggesting that a strong short-term rebound remains unlikely.