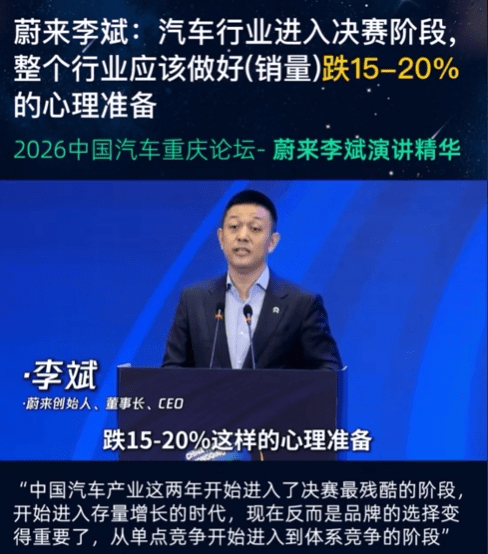

“China’s auto industry has entered a new stage,” Li said at the Chongqing Auto Forum on June 13. “The entire sector should prepare for domestic retail sales to decline 15% to 20% from last year.” William Li’s statements at the 2026 China Auto Forum His forecast aligns closely with recent market data. Passenger vehicle retail sales fell 22.1% year-on-year in May. Total vehicle sales reached 8.15M units in the first five months of 2026, down 20.6%. Passenger vehicle retail sales dropped 19.5% to 7.09M units over the same period. The weakness has continued into June. Weekly market data showed passenger vehicle retail sales totaled 228K units during June 1-7, down 23% year-on-year, down 11% from the same period in May. Most major indicators now point to declines near the 20% level, broadly matching Li’s full-year outlook. Several factors sit behind the slowdown. Over the past three years, China’s EV market benefited heavily from purchase-tax exemptions, local subsidies, trade-in incentives. Part of that support has begun to fade in 2026. Some local subsidy programs have expired, while national EV tax incentives have entered a gradual phase-down period. As a result, demand previously pulled forward by policy support has started to weaken. Heavy foot traffic at the 2026 Greater Bay Area Auto Show. The market is also becoming increasingly saturated. China’s vehicle parc approached 366M units by the end of 2025. A total of 103 cities now have more than one million registered vehicles. Roughly one in every four people already owns a car. Rising ownership levels have made it harder for automakers to rely on first-time buyers as a growth engine. Operating costs have also increased. Prices for 92-octane gasoline have climbed nearly 20% since the beginning of 2026. Public charging service fees have also risen across multiple regions, adding pressure on both gasoline vehicle owners and EV users. Viewed in that context, Li’s remarks reflect a broader assessment of market fundamentals rather than a bearish call on China’s auto industry itself. A decade-long sales curve published by Zhineng Auto illustrates the challenge. China’s passenger vehicle market fluctuated between 19.83M units and 24.08M units annually from 2016 through 2026. Sales bottomed at 19.83M units during the pandemic in 2020, then recovered to 23.36M units in 2024, the second-highest level of the decade. Annual China Passenger Car Terminal Sales, 2016–2026 (10K units) Should Li’s forecast materialize, the implications would be significant. A 15% decline would reduce annual passenger vehicle sales to roughly 19.77M units, slipping below the pandemic-era trough. A 20% decline would push sales down to approximately 18.60M units, near levels last seen before 2016. Such an outcome would amount to one of the steepest contractions in modern Chinese automotive history, effectively erasing a decade of market growth.