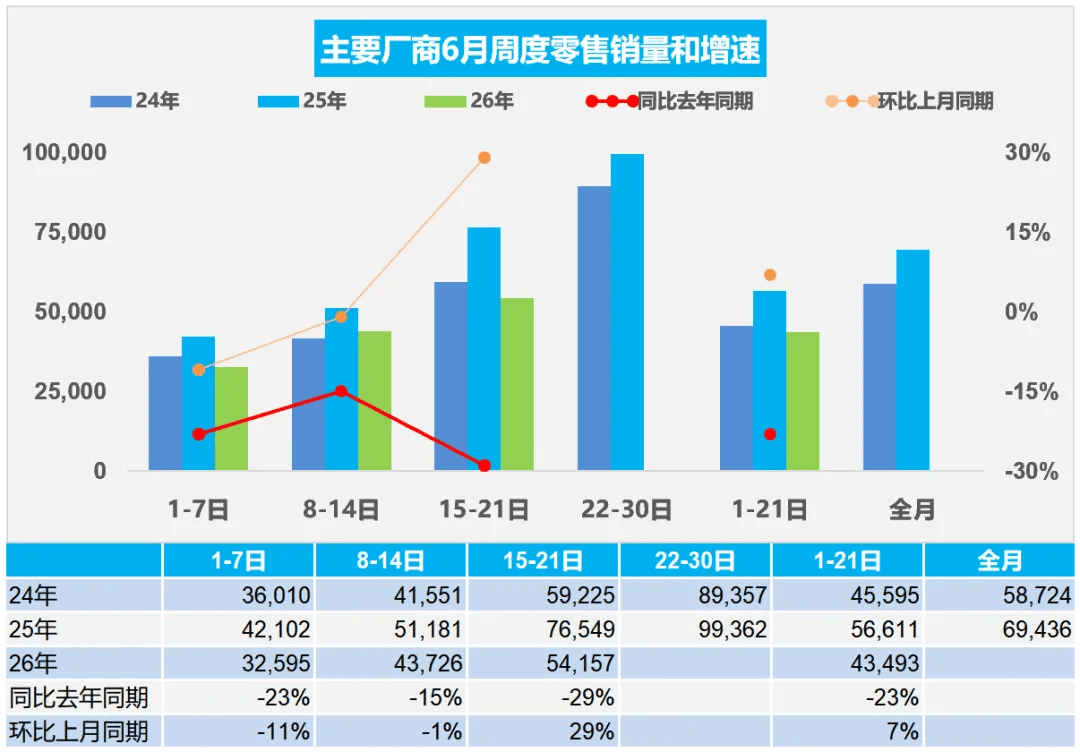

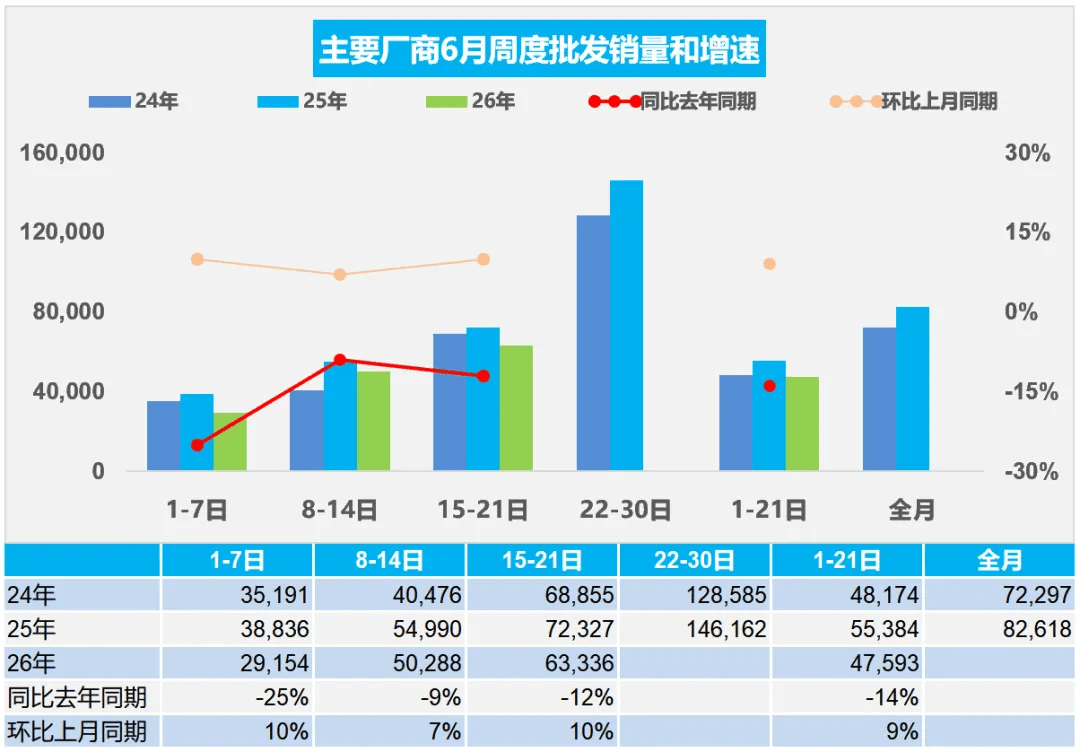

Data released by the China Passenger Car Association (CPCA) showed passenger vehicle retail sales reached 913K units between June 1-21, down 23% year-on-year, though up 7% from the same period in May. Year-to-date retail sales totaled 8.012M units, down 20% from a year earlier, indicating the market remains in an adjustment phase. Weekly trends pointed to a gradual recovery in demand. Average daily retail sales stood at 33K units in the first week, down 23% year-on-year. The second week improved to 44K units per day, with the decline narrowing to 15%. By the third week, daily retail sales had climbed to 54K units. That marked a 29% increase from the corresponding period in May, although volumes remained 29% below year-earlier levels. Weekly sales volume and growth rates in June 2024, 2025, and 2026 Wholesale shipments showed a similar pattern. Passenger vehicle wholesale sales reached 999K units during the same period, down 14% year-on-year, up 9% from the previous month. Cumulative wholesale volume for 2026 reached 11.185M units, down 7%. The third week saw average daily wholesale deliveries rise to 63K units. The year-on-year decline narrowed to 12%, while dealers continued to trim inventory risks by adjusting procurement plans based on market expectations. NEVs remained the industry’s primary growth driver. Retail sales of NEV passenger vehicles reached 583K units in the first three weeks of June, down 10% year-on-year, up 11% from the previous month. NEV penetration remained elevated at 63.8%. Year-to-date NEV retail sales totaled 4.281M units, down 14% from the same period last year. Wholesale performance was more resilient. NEV wholesale deliveries reached 673K units during the period, up 8% year-on-year, up 17% from the previous month. Cumulative NEV wholesale sales reached 5.979M units in 2026, representing a 2% increase from a year earlier. The figures suggest automakers continue to prepare for stronger demand in the second half of the year. Production data highlighted the ongoing shift away from traditional combustion vehicles. Output of conventional gasoline-powered light vehicles totaled 225K units in the first two weeks of June, down 44% year-on-year, down 1% from the previous month. Hybrid-electric vehicles and plug-in hybrids recorded production of 160K units, down 16% year-on-year, up 1% sequentially. Weekly wholesales volume and growth rates in June 2024, 2025, and 2026 As electrification accelerates, the market space available to traditional gasoline vehicles continues to shrink. Hybrid and plug-in hybrid models remain important for automakers seeking to stabilize sales volumes while serving customers transitioning from internal combustion vehicles. CPCA analysts attributed June’s weak market performance to several factors. Last year’s market benefited from a surge in purchases ahead of the expiration of local subsidies, creating a high comparison base. This year, policy support has remained stable, with no major additional stimulus measures. High fuel prices, weaker-than-expected “618” shopping festival promotions, consumer spending shifts linked to the World Cup have also weighed on vehicle demand. The result has been a market characterized by strong enthusiasm for football, weaker momentum in car showrooms.