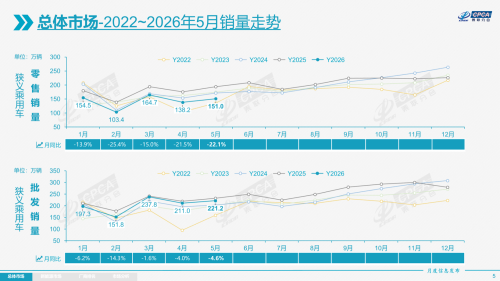

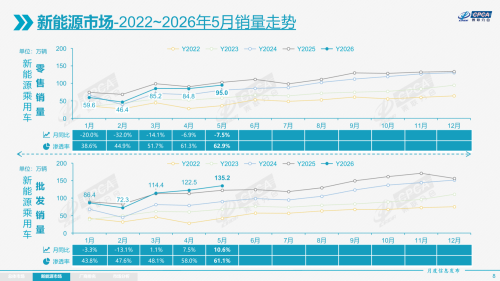

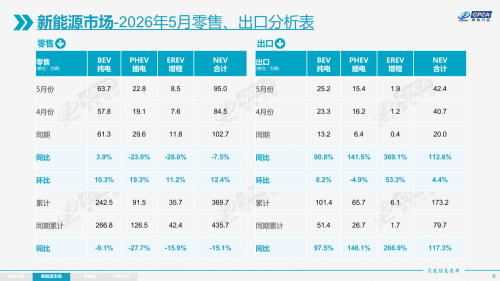

Gasgoo Munich- The May report card for the passenger car market makes for complicated reading.Data from the China Passenger Car Association (CPCA) shows retail sales hit 1.51 million units in May, down 22.1% from a year ago. In any industry, that figure would feel chilling. Yet a 9.2% sequential gain suggests the market isn't dead in the water.Image Source: CPCAThe real story lies in the structural shift behind these numbers: internal combustion engine (ICE) vehicles are accelerating their exit while new energy vehicles (NEVs) are taking the baton. ICE retail sales slumped 39% in May, while the NEV penetration rate climbed to 62.9% — a record high. Between the rise and the fall, the industry landscape is reshaping at speed.Domestic Brands Move Upstream; JVs Accelerate TransformationFor years, domestic brands have leveraged their first-mover advantage in NEVs to deliver a crushing blow to joint ventures (JVs). But in May, the battle grew more complex. A simple narrative of "one rises as the other falls" no longer captures the moment.Overall, domestic brands still hold a firm grip on the market. Retail sales reached 1.04 million units in May. While that's a 17% year-on-year dip, their domestic retail share rose to 68.7%, up 3.8 percentage points. That means more than two out of every three new cars sold now wear a domestic badge. Yet behind that glowing market share lies a hidden concern: the engine of growth for these brands is shifting structurally.Domestic brands, once conquerors of the low-end market, faced a severe test in May. Hit by subsidy rollbacks and sluggish entry-level demand, domestic NEV retail sales fell 10% year on year. This confirms the dilemma of "pressure on low-end economy cars" highlighted by CPCA Secretary-General Cui Dongshu.CPCA data shows wholesale sales of A00-class pure electric vehicles plummeted 44% year on year. The golden age of micro EVs seems to have hit pause. The decline in county and township markets, along with entry-level models, sounds an alarm for the "inclusive electrification" drive.In sharp contrast to the temporary setbacks at the low end, the premium market is becoming a new profit pool and technological high ground for domestic brands.Data indicates domestic brands now command over 50% retail share in segments ranging from 200,000 to 300,000 yuan, 300,000 to 400,000 yuan, and even above 400,000 yuan. From BYD's Yangwang and Denza to NIO, Li Auto, ZEEKR, and Avatr, Chinese brands have used technology and user experience to breach the high-end defenses held by joint ventures and luxury marques. This is no longer just about value-for-money substitution; it is a head-on collision of brand value.Joint ventures, meanwhile, face a more complex predicament.In May, mainstream JV retail sales stood at 310,000 units, down 35% year on year. German brands held 13.4% share, down 2.3 percentage points, while Japanese brands slipped to 10.5%, a drop of 2.1 percentage points. Their ICE foundation is collapsing at a 39% annual rate.Cui Dongshu puts it bluntly: high oil prices are dealing a massive shock to the domestic market. "In May, some ICE users switched to NEVs. Overall passenger car retail sales fell 22%, but NEV retail only dropped 7%, while ICE fell 38%. So some ICE owners are shifting to NEVs, specifically pure electric products. With high oil prices, consumer sensitivity to fuel costs has surged, making people reluctant to use ICE cars and more willing to switch to NEVs."For JV automakers relying on ICE vehicles, this is a significant blow.Notably, JVs — long relegated to the sidelines in the NEV race — finally showed signs of accelerating their catch-up efforts in May. CPCA data shows JV NEV sales jumped 51% year on year, while domestic NEV growth slowed by 10%. That contrast is worth pondering. Although the absolute scale of JV NEVs remains small, with just a 5% domestic retail share, the momentum cannot be ignored.This suggests that after a period of pain, JV giants are finally pouring resources into electrification. Relying on their deeper heritage and brand recognition, they are trying to claw back ground in the pure electric and plug-in hybrid markets. A new battle has begun, shifting from "domestic offense, JV defense" to "domestic high-end breakthrough, JV low-end counterattack."NEV Premium Booms, Entry-Level BucklesIf the decline of ICE vehicles was a script written in advance, then the internal divergence within the NEV market is the key point worth reflecting on from May.Image Source: CPCABehind the 62.9% penetration rate lie two very different stories.One story plays out in the premium market. In May, wholesale sales of B-segment pure electric vehicles surged 42% year on year, becoming the core engine driving the pure EV market. B-segment cars now account for 31% of pure EV wholesale volume, up 4.3 percentage points from last year. Consumers are willing to pay more for longer range, smarter driving tech, and extreme performance. Tesla, NIO, ZEEKR, and BYD's premium series have all found their growth trajectory in this lane.The other story is at the low end. A00-class pure EVs, once hailed as the "people's commuter," saw wholesale sales crash 44% in May, with market share shrinking from over 20% to just 10%. This is a warning signal. Low-end economy EVs — the category with the most potential to replace ICE vehicles — face a survival crisis due to subsidy rollbacks, rising raw material costs, and the trend of consumption downgrading.Technologically, pure electrics remain the mainstream, but range-extended vehicles (EREVs) are cooling off significantly. CPCA data shows pure EV wholesale sales reached 886,000 units in May, up 16.6%, while plug-in hybrids (PHEVs) hit 372,000, up 10.5%. In contrast, EREV sales dropped 24.9% to 95,000 units.In other words, May's rebound wasn't a broad-based rise, but a clear structural divergence.Fortunately, the export market has absorbed much of the pressure for Chinese NEVs.CPCA data reveals NEV passenger car exports hit 424,000 units in May, soaring 112.6% year on year and accounting for 54.1% of total passenger vehicle exports — another record high. BYD alone exported over 155,000 units, followed by Chery, Geely, and Tesla. Cui Dongshu emphasized: "Exports achieved explosive growth, accounting for 54%, forming a dynamic driven by NEVs and domestic brands."Image Source: CPCAStructurally, pure electrics still dominate exports, but the share of plug-in hybrids is rising fast. In May, pure EVs made up 59.3% of NEV exports, while plug-in hybrids accounted for 36.2%, a notable increase from 31.9% a year earlier. This signals growing international recognition for Chinese plug-in hybrid technology.Notably, plug-in hybrid models are growing rapidly in developing markets. This suggests Chinese NEVs are shifting from "product exports" to "industry exports" — not just selling cars, but exporting the capabilities of the entire supply chain.From a global perspective, China's lead in NEVs remains solid. CPCA data shows that from January to April 2026, China captured 71% of the global plug-in hybrid market and 56% of the pure electric market. China is not just the world's largest NEV market; it is an exporter of core technologies.The performance of new forces confirms this structural divergence.In May, new forces captured 24.9% of the retail market, up 4.5 percentage points year on year. Leapmotor, NIO, Li Auto, and Xiaomi have all secured their footing in their respective segments.Automaker performance shows clear concentration at the top. CPCA data lists 20 manufacturers with monthly NEV wholesale sales exceeding 10,000 units, accounting for 93.4% of total NEV passenger volume. BYD Auto led with 377,000 units, followed by Geely Auto at 131,000, Chery Auto at 95,000, Tesla China at 86,000, and Leapmotor at 82,000.Competition in the NEV market has entered the stage of "systemic warfare." The era of conquering the world with a single hit model is over; technology, distribution, service, and cost control are now indispensable.While joint ventures are accelerating their transformation, as Cui Dongshu noted, "The changes aren't particularly obvious yet." In May, the NEV penetration rate of mainstream JVs rose only to 14.5%, leaving a massive gap compared to domestic brands' 81.4%.June Market: Seeking Stability Amid UncertaintyLooking ahead to June, can the Chinese auto market sustain its sequential recovery from May? The answer doesn't look optimistic. A special "distraction" and an ongoing "storm" are casting a shadow of uncertainty over the coming month.Image Source: IM MotorsThe World Cup returns for its once-every-four-years run. This seemingly unrelated factor cannot be ignored when assessing its impact on the auto market.Cui Dongshu stated: "For June's trend, we expect a sequential recovery but year-on-year pressure. However, we aren't sure how strong the recovery will be. The biggest feature of June is the World Cup. Remember, during the June 2018 World Cup, the passenger car market fell 7% sequentially, and in 2010 and 2014, it also fell 4%. During the World Cup, people only watch football, not cars, which brings some pressure to June."Beyond the World Cup, there is another disruptive factor this June. According to CPCA analysis, the Dragon Boat Festival falls on June 19 this year, significantly later than last year's May 31 slot. Holiday traffic and consumption diversion will disrupt the market this month, slightly dampening booking heat in the middle of the month.Setting aside these short-term disruptions, more fundamental pressure comes from the macroeconomic environment and the challenge of consumer confidence.The "high oil prices" Cui Dongshu repeatedly emphasizes have become a Sword of Damocles hanging over the entire auto market. International oil prices are running high, driving up domestic refined oil prices. This has directly caused a spike in ICE operating costs, greatly suppressing the willingness of potential buyers to purchase. Even as some consumers switch to NEVs, the erosion of overall purchasing power by high oil prices will cause price-sensitive buyers to stay on the sidelines.Profitability is also under pressure. CPCA data shows that from January to April 2026, the auto industry generated sales revenue of 3,312.9 billion yuan, up 1.1% year on year, but profit was only 111.9 billion yuan, down 17%. The sales profit margin fell further to 3.4%, a historical low. With rising raw material costs upstream and terminal pressure downstream, automakers are squeezed from both sides.As a result, the industry finds it hard to offer an optimistic outlook for June.According to the CPCA outlook, June will likely see a "weak recovery" pattern: sequential warming but year-on-year pressure. On one hand, the tradition of pushing for performance at the half-year mark persists, automakers will increase terminal promotions, and negative policy factors have largely played out, so a slight sequential gain is expected. On the other hand, June has 21 working days, one more than last June, providing a year-on-year advantage in days that supports production and sales. However, with the combined effect of the World Cup and high oil prices, a significant positive year-on-year turn is almost impossible.Yet, there are bright spots in the darkness.The biggest bright spot remains exports. With domestic demand soft, exports have become the core pillar supporting confidence. May's strong performance is likely to continue into June. The expansion of domestic brands overseas is effectively offsetting growth pressure at home. The pattern of "weak domestic demand, leading external demand" will become clearer in June.Image Source: CheryIn terms of overseas layout, Chinese automakers are diversifying. CPCA data shows that from January to April 2026, the top three destinations for Chinese auto exports were Brazil, Russia, and the UK. Brazil saw year-on-year growth of over 200,000 units, becoming the fastest-growing single market. With blooms across Latin America, Europe, and Southeast Asia, risks are effectively spread across multiple markets.Additionally, there is little doubt that the NEV penetration rate will hold steady above 60%. High oil prices continue to drive consumer preference toward electric vehicles, and with the concentrated delivery of several new NEV models in June, the dominant position of electrification will only solidify.This means that even if overall market growth slows, the structural upgrade within the industry will not stop.In terms of inventory, the industry is actively destocking, laying the foundation for healthy development in the second half. CPCA data shows overall passenger vehicle industry inventory fell by 350,000 units from January to May, compared to a growth of about 10,000 units in the same period of 2025. While dealers face survival pressure, the inventory burden is easing.For automakers, June's test is practical: How to reach target customers accurately during the World Cup? How to resist cost pressure through product structure optimization? How to find growth in a zero-sum game?The rules of the elimination game are becoming clear: Those relying on ICE dividends will face mounting pressure; those sticking to the low-end market must find a path to transformation. Only players who insist on technology-based survival, brand upward mobility, and global layout will have the initiative in the next round of competition.In the summer of 2026, the Chinese auto market is destined to move through uncertainties. But within those variables, the trend is irreversible.