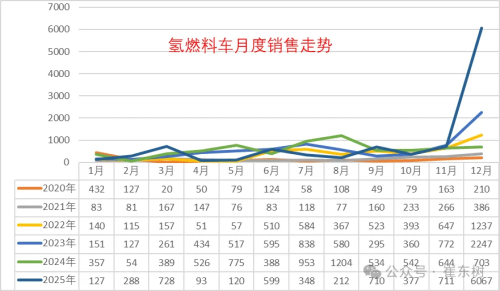

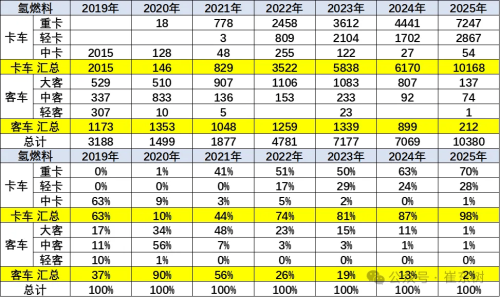

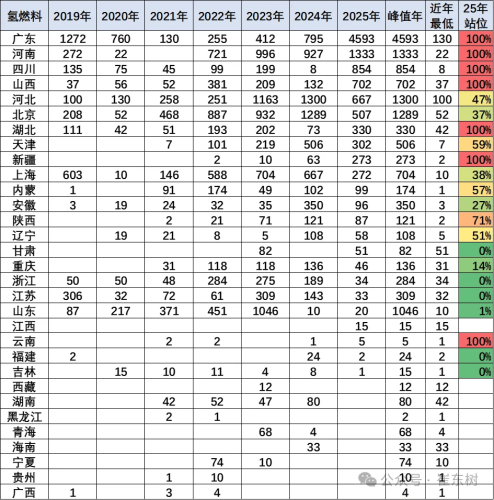

The 2025 hydrogen fuel cell vehicle market saw uneven quarterly distribution, with sales heavily reliant on a year-end policy push. Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA), released the “2025 Hydrogen Fuel Cell Vehicle Analysis Report.“ Trend of Fuel Cell Vehicles Data shows that insurance registrations reached 10,380 units in 2025, a year-on-year increase of 47%. However, actual market demand fell short of expectations, with sales heavily reliant on a year-end policy-driven surge. Monthly Trend of Fuel Cell Vehicles Looking at the monthly trend, although hydrogen fuel cell vehicle sales achieved nearly 50% growth in 2025, the quarterly distribution was extremely uneven. The market remained sluggish from Q1 to Q3, with monthly sales fluctuating between 93 and 728 units, indicating a clear weakness in the industry’s capacity to sustain demand. However, sales in December alone surged to 6,067 units, accounting for nearly 60% of the annual total. This phenomenon highlights the industry’s heavy reliance on policy subsidies. Reviewing recent trends: from 2020 to 2022, the industry was in its infancy, with annual sales below 5,000 units. In 2023, sales exceeded 7,000 units, a 50% year-on-year increase. In 2024, affected by policy adjustments, sales slightly decreased by 2% to 7,069 units. In 2025, stimulated by high subsidies, the market returned to a growth trajectory, but the structural characteristic of “year-end sales sprint” remained unchanged, indicating that the market’s self-regulating mechanism has not yet formed. Market Structure of Fuel Cell Vehicles In terms of market structure, the application of hydrogen fuel cell vehicles is highly concentrated in the commercial vehicle sector. Heavy trucks accounted for 70%, light trucks for 28% (totaling 98% for trucks), while buses made up only 2%. Cui Dongshu pointed out that this structural shift stems from the combined effects of policy orientation and scenario-specific economics. Regarding regional distribution, the market for hydrogen fuel cell vehicles is highly concentrated in policy demonstration city clusters. The top five provinces for sales in 2025 were Guangdong (4,593 units), Henan (1,333 units), Sichuan (854 units), Shanxi (702 units), and Hebei (667 units), together accounting for over 70% of the total. Notably, regions with concentrated steel industries, such as Tianjin and Hebei, show higher acceptance of hydrogen fuel cell vehicles due to their specific industrial transportation needs. This highly concentrated regional distribution also reflects the strong dependence of hydrogen vehicle development on local fiscal subsidies and industrial policies. Regional Market Trends of Fuel Cell Vehicles From the perspective of corporate landscape, leading manufacturers include Dongfeng Liuzhou Motor, Zhengzhou Yutong, Sinotruk, Dongfeng Special Vehicle, and Sany Heavy Industry. It is worth mentioning that due to OEMs’ limited accumulation of core fuel cell stack technology and their primary reliance on an assembly model, the industry’s technical barriers are relatively low. While various manufacturers can produce vehicles, forming a differentiated competitive advantage remains difficult. The report emphasizes that during the 2026-2027 period, with the adjustment of the new energy vehicle purchase tax exemption policy, hydrogen fuel cell vehicles will face a more severe market test.