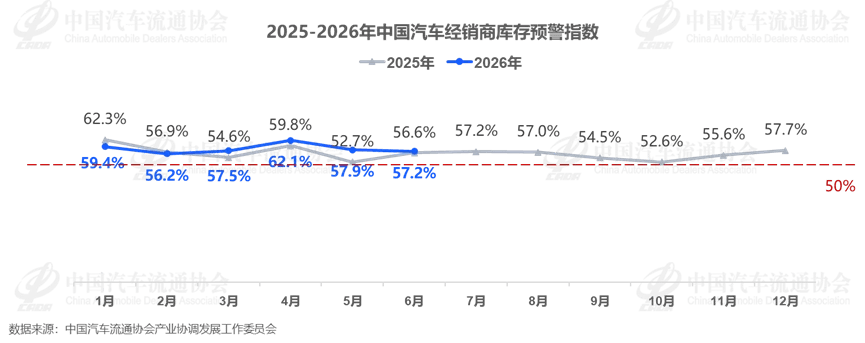

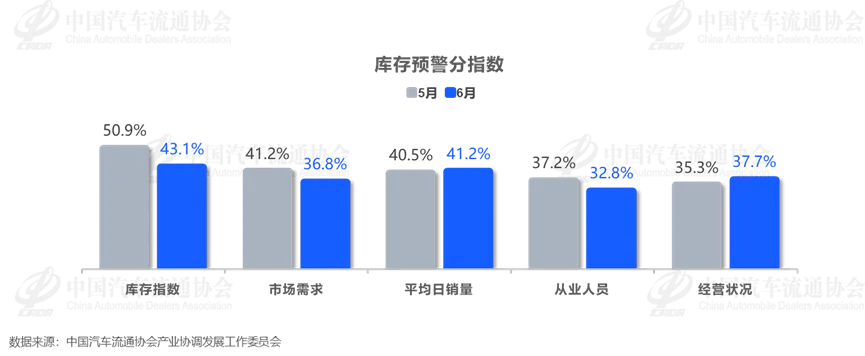

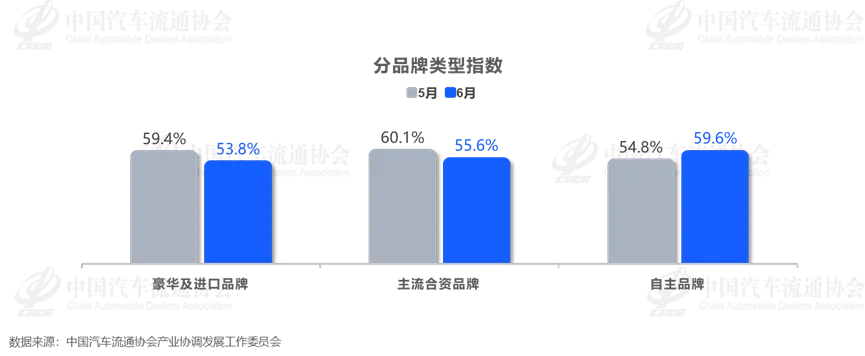

The China Automobile Dealers Association reported that the Vehicle Inventory Alert (VIA) Index for June 2026 stood at 57.2%, up 0.6 percentage points year on year and down 0.7 percentage points month on month, remaining above the 50% threshold that separates expansion from contraction. Market performance in June showed a clear “weak-then-strong” intra-month pattern. The rebound in terminal sales during the second half of the month was largely driven by short-term promotional activity, without materially improving the overall softness in demand. China VIA index trends from 2025 to June 2026 CADA noted that while some dealerships saw sales gains supported by mid-year volume campaigns, new model launches, and local subsidies, the broader market still lacked sustained consumption momentum. By sub-index, inventory levels, market demand, and employment sentiment all declined on a month-on-month basis. Average daily sales and business condition indices recovered to 41.2% and 31.7% respectively, but remained at relatively low levels. China VIA sub-index between May and June 2026 Survey data showed that 57.4% of dealers reported a further increase in consumer hesitation in June. Among them, 37.0% said price comparison behavior became more frequent, while purchasing decision cycles continued to lengthen significantly. Profitability pressure remained more pronounced than sales pressure for dealers. Only 12.0% of dealerships reported meeting their planned first-half sales targets, while another 11.1% achieved 90%–100% completion. This implies that 76.9% of dealers failed to meet half-year targets, with 39.8% achieving less than 70% of their planned volumes. Regional divergence persisted. The western region recorded an index of 61.2%, notably higher than the national average, while the eastern, northern, and southern regions stood at 56.8%, 55.1%, and 53.1% respectively. By brand segment, inventory warning indices for luxury/imported brands and mainstream joint-venture brands fell to 53.8% and 53.6%, respectively, while domestic brands edged up to 59.6%. China’s VIA index across different brand levels between May and June 2026 In recent years, domestic brands have continued to gain market share, but intensified competition and frequent new product launches have increased inventory management pressure across distribution channels. Separately, CPCA estimated June retail sales of narrow passenger vehicles at around 1.65 million units, up 9.3% month on month. New energy vehicle retail sales were expected to reach around 1.05 million units, up 10.5% month on month, with penetration at 63.6%. This indicates that NEVs remain the primary growth driver in the market, although sales momentum has not fully alleviated pressure on dealer operations. Authorities including the Ministry of Commerce have recently introduced a series of measures to support auto consumption, including 17 policies aimed at developing the automotive aftermarket. Looking ahead to July, traditionally a low season for auto sales, dealers remain cautious. CADA expects that with mid-year promotional campaigns ending and weaker seasonal demand during the summer period, both foot traffic and sales are likely to decline on a month-on-month basis.