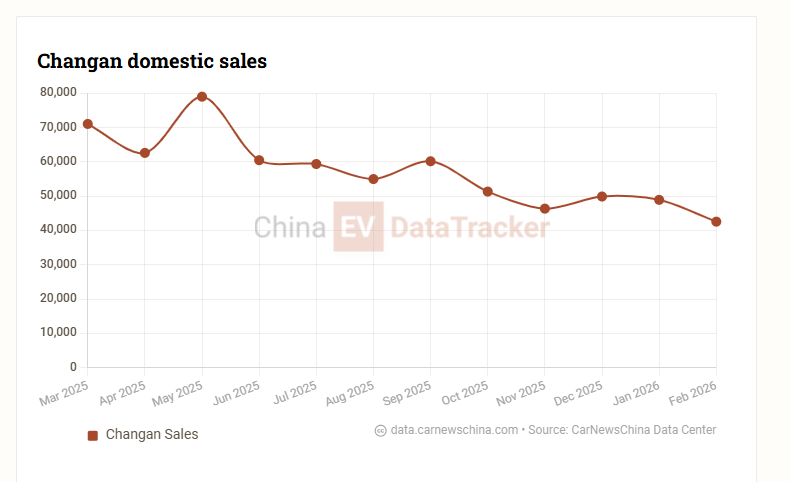

Blue Core Super Engine from Changan. Credit: Changan Understand China EV’s Market Real-time notifications when critical EV data is released All important data in one place 2,000,000+ data points Become a member Hybrid electric vehicles (HEVs) have re-emerged as a strategic focus for Chinese automakers in 2026, with companies including Changan, Geely, and Chery announcing new systems and products, according to 36kr. The renewed push comes as Toyota continues to dominate global hybrid sales, while BYD expands its presence with plug-in hybrid and battery-electric vehicles. Different technical paths Toyota’s hybrid system (THS) remains based on a planetary gear power-split device that mechanically links the engine and wheels. This allows the engine to operate within an efficient range, with electric motors assisting when needed. This approach prioritises fuel efficiency and smoothness, but limits peak electric drive output due to the constant mechanical coupling. Chinese automakers are adopting a different architecture. Their HEV systems are typically based on series-parallel layouts combined with multi-gear dedicated hybrid transmissions (DHT). In these systems, electric drive often dominates, with the engine operating primarily in efficient conditions or acting as a generator. For example, Changan’s Blue Core HEV uses a dual-motor setup with multiple operating modes, including pure electric drive at low speeds, engine-assisted acceleration, and direct engine drive at highway speeds. Compared with Toyota systems, Chinese HEVs typically use larger drive motors, ranging from 130 to 180 kW, enabling stronger acceleration performance. Urban fuel consumption is claimed to reach around 2–3 L/100 km under certain conditions. Narrowing cost gap One of the main drivers behind the shift toward HEV is cost structure. HEVs typically use batteries sized at 1–2 kWh, significantly smaller than plug-in hybrids (10–20 kWh) or battery electric vehicles (50 kWh or more). This reduces exposure to battery material costs, which have remained relatively high despite volatility in lithium prices. As vehicle pricing continues to decline in China’s competitive market, smaller battery systems offer a way to maintain margins. Changan’s annual sales data in China. Credit: China EV DataTracker Crossover by 2027 Chinese brands are positioning HEVs as complementary solutions rather than replacements for BEVs or PHEVs Globally, Toyota’s performance highlights the continued relevance of hybrids. The company sold 11.3 million vehicles in 2025, with hybrids accounting for about 42 percent, or roughly 4.4 million units. At the same time, BYD’s strategy shows a different direction. The company delivered 4.6 million vehicles in 2025, split almost evenly between plug-in hybrids and pure-electric models. This positions BYD closer to electrification-heavy pathways, while still relying heavily on hybridisation. Scaling up Multiple Chinese automakers are preparing HEV launches. Geely has announced its i-HEV system targeting fuel consumption of around 3 L/100 km. Chery is experimenting with larger battery HEVs, including configurations around 5 kWh, which blur the line between traditional HEVs and plug-in hybrids. Changan has also begun promoting test drives for its latest HEV models, indicating near-term commercialisation. Industry push The renewed interest in HEV reflects both domestic and global considerations. In international markets where charging infrastructure remains limited or electricity costs are high, hybrids remain a practical alternative to full electrification. Toyota’s strong hybrid sales in such regions support this positioning. Domestically, China still has a large base of internal combustion vehicle users, providing a transition market for hybrids that do not require charging. Policy backdrop Policy changes are also influencing the shift. From 2026, China’s purchase tax incentives for plug-in hybrids have been reduced from full exemption to partial relief. While HEVs do not receive similar incentives, the policy gap between the two technologies is narrowing. At the same time, industry expectations suggest that tax incentives for all powertrains could gradually phase out in the coming years, potentially improving the relative attractiveness of HEVs. Market positioning The current wave of HEV development among Chinese automakers does not replicate Toyota’s approach but instead reflects a different technical route that emphasises electric drive and system flexibility. Rather than a reversal of electrification trends, the move toward HEV appears to be a parallel strategy shaped by cost pressures, export requirements, and policy adjustments.