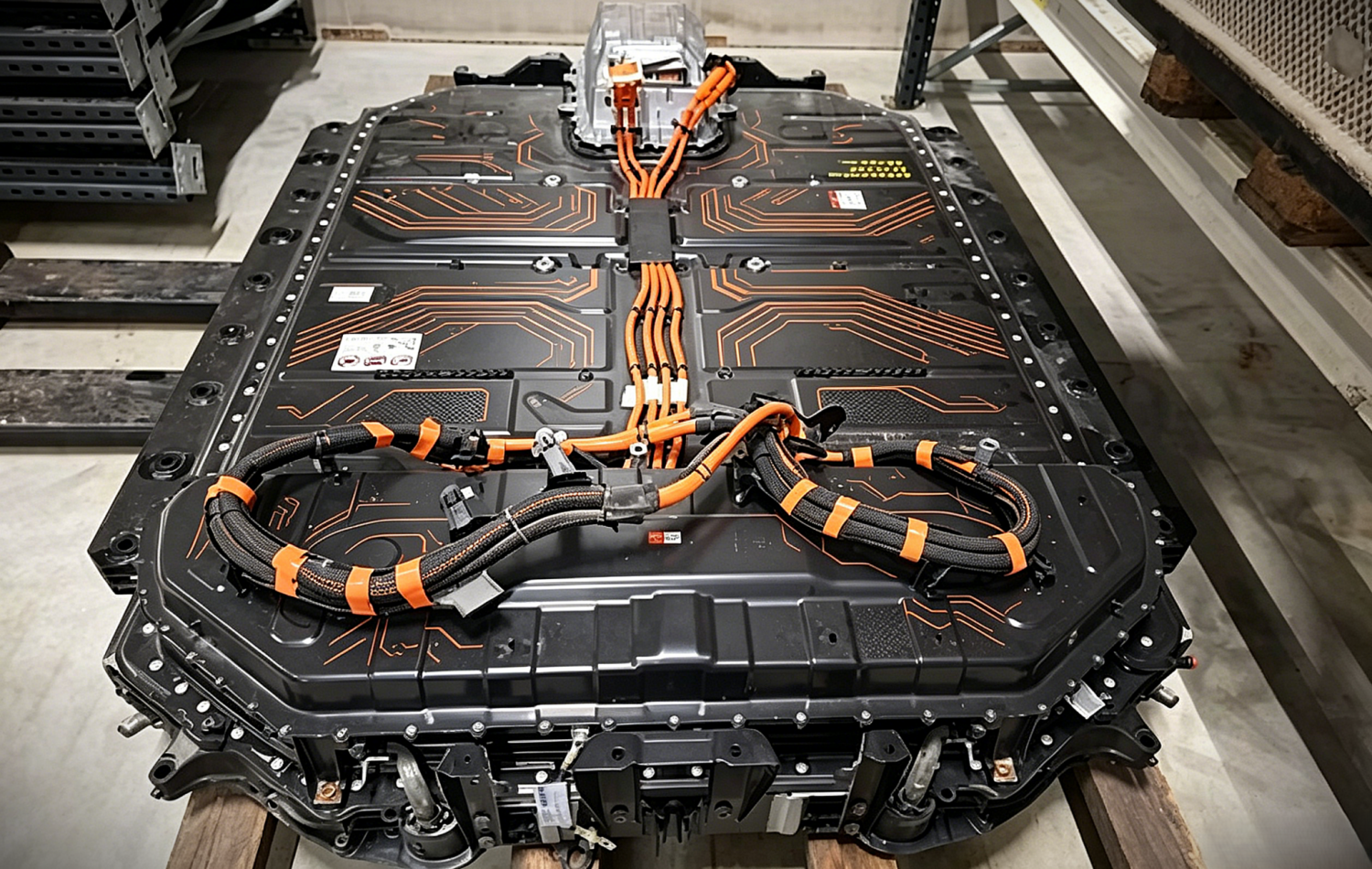

A critical supply bottleneck in Southeast Asian coconut shells forces automakers to scale anthracite anodes. Credit: CES Understand China EV’s Market Real-time notifications when critical EV data is released All important data in one place 2,000,000+ data points Become a member Sodium-ion automotive battery architectures are entering an intensive phase of raw-material re-engineering as Chinese vehicle manufacturers seek local components. The technical transition aims to achieve complete self-reliance from volatile foreign lithium supply lines. Initial volume deployment has commenced through new pipeline integration across low-cost budget passenger vehicle segments and localised grid storage utility networks. The microstructural layout of larger sodium ions prevents conventional graphite electrodes from maintaining stable intercalation during rapid charging cycles. Cells require a specialised hard-carbon negative electrode to ensure clear transport paths without structural degradation. This hardware constraint forces tier-1 manufacturers to completely overhaul their upstream chemical processing and material sourcing. The agricultural crisis Biomass precursors derived from charred Southeast Asian coconut shells became the early manufacturing baseline for hard carbon production. This chemical path created an immediate risk because premium agricultural materials remain concentrated outside China. Domestic resource tracking indicates that local tropical coconut supplies can support a maximum capacity of only 6.3 GWh annually. This resource ceiling conflicts directly with upcoming scaling projections across the broader electric vehicle industry. Component planners expect total sodium cell market demand to exceed 100 GWh by 2027. Consequently, continuing to rely on foreign tropical agriculture introduces an unsustainable material bottleneck that threatens to halt mass vehicle assembly lines. The coal solution To eliminate this agricultural vulnerability, domestic material companies are shifting factory lines toward fossil inputs. Heavy chemical enterprises are deploying regional anthracite coal to synthesize high-purity non-graphitizable carbon arrays. This engineering pivot underpins the affordable electric transport segments that recently initiated high-volume assembly operations within specialised domestic factory infrastructures. The industrial choice between organic and fossil inputs relies heavily on material yield optimisation. Turning agricultural coconut waste into battery-grade carbon yields a minor 2.5% of the raw starting mass. Conversely, specialised high-temperature processing of domestic coal delivers a much higher 45% manufacturing yield, securing an independent local asset supply chain. Reaching cost parity Rapid commercial-scale anthracite processing has already dismantled previous manufacturing price floors. Hard-carbon anode costs have dropped below 30,000 yuan (4,416 USD) per ton, a level not seen in prior history. Automotive supplier roadmaps confirm an ultimate pricing target under 20,000 yuan (2,944 USD) per ton to guarantee long-term market viability. Lower material thresholds are accelerating the commercial validation of mass-produced sodium-ion battery products across entry-level passenger models. Market tracking indicates polyanion cathode configurations captured 77% of total industry shipments last year due to superior lifecycle stability. This expanding production infrastructure establishes a dual-track architecture that safely powers next-generation vehicle fleets with locally produced coal-derived battery packs.Sources: Jrj, STCN