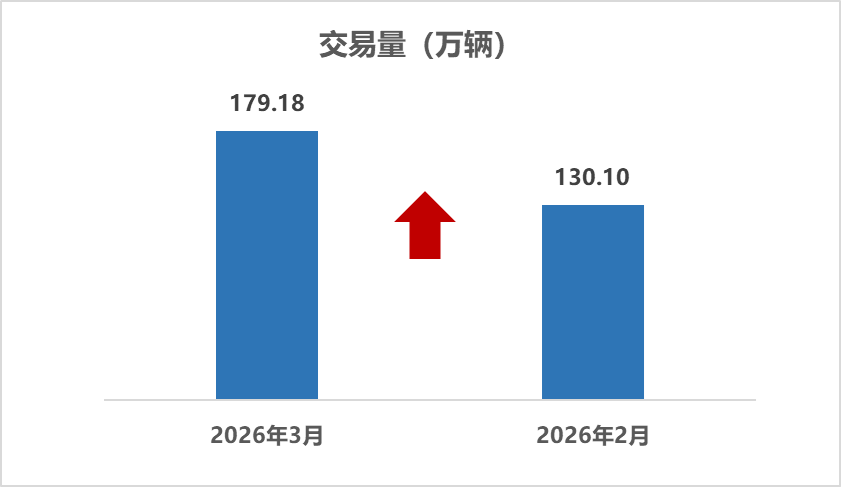

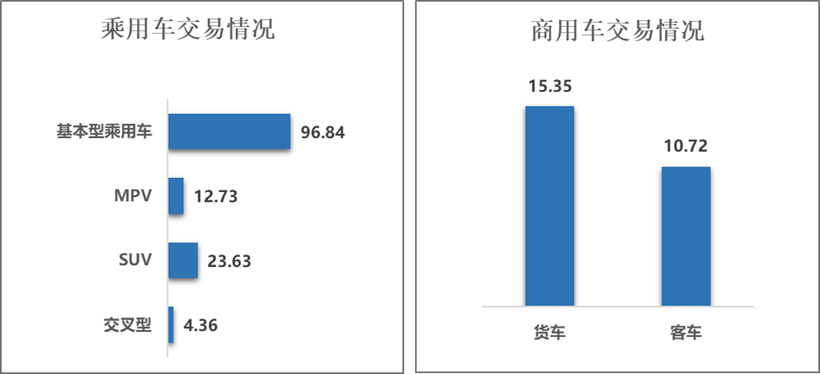

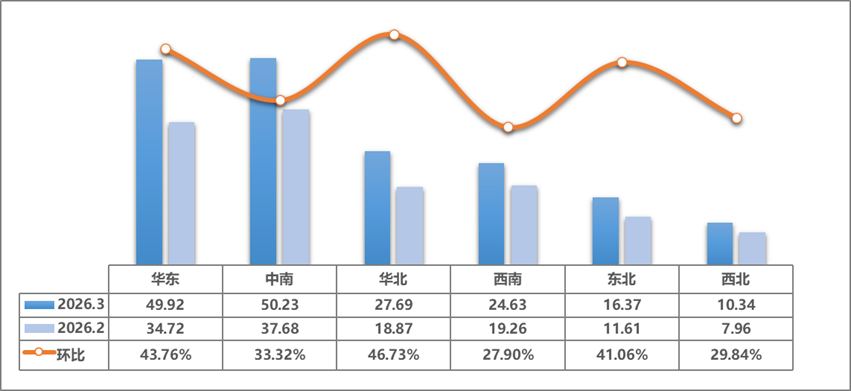

Gasgoo Munich-China's used car market posted a clear rebound in March 2026. With the Lunar New Year holiday in the rearview mirror and dealers fully back at work, pent-up demand was unleashed, setting the market on a steady recovery path. Data from the China Automobile Dealers Association shows March transactions hit 1.79 million units — a 37.73% monthly jump and a 2.11% annual rise. Transaction value reached 117.87 billion yuan.Image Source: China Automobile Dealers Association (same below)Cumulative data for the first quarter tells a similar story. From January to March, used car transactions totaled 4.822 million units, up 4.66% year-on-year, adding 214,600 units compared to last year. Total transaction value came to 312.88 billion yuan. Overall, the market showed mild growth in Q1, with March's strong turnaround providing the momentum needed to offset the holiday slump. Compared to February, March offered a full slate of working days, faster inventory turnover, and a clear rebound in consumer willingness to buy and sell — driving a substantial lift in market activity.Segment Divergence: MPVs and Commercial Vehicles Take the LeadPerformance varied significantly by segment in March. Sedans, the traditional mainstay, saw 968,400 units traded — up 38% month-over-month but down 3.45% annually. SUV volume reached 236,300, climbing 35.43% from February and 1.36% from last year. MPVs were the standout, with 127,300 units sold, a 38.49% monthly surge and a 12.06% annual gain. Cross-type passenger cars reached 43,600 units, up 37.52% month-over-month but slipping 3.22% year-on-year.Commercial vehicles also posted notable gains. Bus transactions hit 107,200 units, up 36% month-over-month and 8.76% year-on-year. Truck volume reached 153,500, climbing 38.1% monthly and 6.64% annually. The year-on-year growth in commercial vehicles extends the positive momentum seen since the start of the year. This is directly linked to the normalization of logistics and transport operations post-holiday, as individual operators update their production tools.Looking at Q1 cumulative data, passenger car transactions totaled 3.7125 million, up 0.88%. Within that, sedans reached 2.6159 million, down 1.17%, while SUVs climbed to 641,300, a 4.05% increase. MPVs surged to 339,000 units, up 12.8%, and cross-type passenger cars edged down to 116,300, a 0.14% decline. Commercial vehicles hit 700,300 units, a 12.21% jump, with trucks up 13.12% to 413,000 units and buses up 10.93% to 287,300 units.MPVs and commercial vehicles were the primary drivers of growth in the first quarter. The rapid rise in MPVs reflects release replacement demand for both family and business use. As two- and three-child families grow, along with weekend travel needs, the practicality of MPVs is winning over more consumers — a shift reflected directly in used car figures. Commercial vehicle growth significantly outpaced passenger cars, indicating a stronger recovery in demand tied to production and operations. Small businesses and self-employed individuals are showing a renewed willingness to invest in tools of the trade. Meanwhile, the slight dip in sedan transactions suggests a structural adjustment: buyers are increasingly favoring functionality and space over traditional sedans.In terms of vehicle age, models aged 3 to 6 years dominated the market in March, accounting for 43.13% of transactions. Nearly-new cars under three years old made up 29.88%, up 2.29 percentage points year-on-year. Vehicles aged 7 to 10 years comprised 16.28%, while those over 10 years accounted for 10.72%. The rise in nearly-new vehicles is directly linked to trade-in policy incentives, bringing higher-quality inventory into the market and lifting overall circulation standards. Still, the 3-to-6-year bracket commands nearly half the market, suggesting these vehicles offer the best balance between value and reliability — remaining the core trading range for now.Nationwide Rebound: All Six Regions Rally, Cross-Border Trade AcceleratesTransaction volumes surged across all six major regions in March, signaling a broad-based recovery. Data from the China Automobile Dealers Association shows the Central-South region led the nation with 502,300 units, up 33.32%. The East followed with 499,200 units, posting the fastest growth at 43.76%. Shanghai saw its volume double, while Jiangsu and Fujian surged 52.3% and 42.4%, respectively. As the nation's economic engine, the East's volume and growth rate serve as a bellwether — and March's performance only solidified its leading position.The North region posted the fastest growth among the six, with 276,900 units traded — a 46.73% monthly jump. Beijing also saw its volume double, completely reversing February's slump. Gains in Tianjin, Inner Mongolia, Shanxi, and Hebei ranged between 31% and 43%, highlighting a coordinated recovery in the Beijing-Tianjin-Hebei area. After February's seasonal lull, the northern market saw a strong release of demand, driven by both seasonal factors and aggressive post-holiday marketing and inventory acquisition by dealers.The Southwest region recorded 246,300 units, up 27.90%, with Sichuan and Tibet posting impressive gains of 35.2% and 38.6%, respectively. The Northeast followed with 163,700 units, a 41.06% increase led by Heilongjiang's 45.4% surge. The Northwest reached 103,400 units, up 29.84%, with Qinghai jumping 42.4% and Gansu and Ningxia rising around 32%. All six regions posted positive growth, with most exceeding 25% — a rare feat in monthly data over the past two years, suggesting March's recovery has a solid foundation.Cross-regional trade also picked up speed. The used car transfer rate climbed to 32.08% in March, up 1.41 percentage points month-over-month and 2.57% year-on-year. Total transferred volume reached 574,900 units, surging 44.04% monthly and 10.99% annually. The rising transfer rate indicates smoother cross-regional circulation and improving resource allocation efficiency in a unified national market. This helps balance supply and demand across regions, particularly as nearly-new vehicles flow from Tier 1 and Tier 2 cities to meet consumer needs in Tier 3, Tier 4, and rural markets.Overall, March marked a broad-based recovery for China's used car market. Transaction volumes rebounded sharply month-over-month, with MPVs and commercial vehicles providing structural highlights. Regional markets rallied in sync, and cross-regional circulation accelerated. The March figures set a positive tone for the second quarter. As local consumption policies take effect and consumer acceptance of used cars continues to rise, the market is poised to maintain its steady momentum.