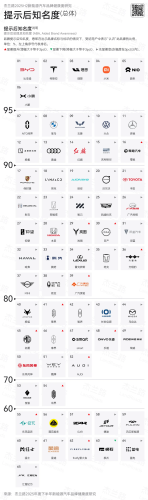

LandRoads’ report reveals stable NEV brand rankings, highlighting gains for mid-tier brands and evolving consumer perceptions. On January 5, market research firm LandRoads released its “H2 2025 New Energy Vehicle Brand Health Report”. This marks the eighth consecutive edition of the study since its launch in 2021. The survey covers 65 NEV brands and is based on responses from more than 12,000 NEV owners. It assesses public perception across dimensions including aided brand awareness (ABA), preference, perceived positioning, confidence in future development, and brand image. The report shows that brands ranked in the top 50% for ABA saw little change from the first half of the year, with the leading group remaining largely stable. However, several mid- to lower-tier brands recorded notable gains, including Shangjie, Maextro, Stelato, firefly, AUDI, and Hyptec. Overall, the top six brands by ABA are BYD, Tesla, Li Auto, Xiaomi, NIO, and Xpeng. H2 2025 NEV Brand Health Survey based on ABA In terms of the preference index per 100 respondents, the average NEV consumer is now familiar with nearly 10 brands, a record high. Tesla continues to rank first, followed by AITO, BYD, the NIO brand, Li Auto, and Xiaomi. Xiaomi and Li Auto, however, experienced a phase of correction. Xiaomi’s “dislike” ratio rose by around 10 percentage points within a single survey cycle, accompanied by a decline in its “like” ratio, representing one of the most pronounced shifts in the sample. H2 2025 NEV Brand Health Survey based on preference index per 100 respondents Perceived brand positioning remained broadly stable, though some brands saw structural changes. Dongfeng M-Hero was affected by the M817 entering the mainstream price segment, influencing its overall positioning perception. New models such as the Nissan N7 and Wey Gaoshan helped lift perceived positioning for their respective brands. ONVO drew particular attention for showing a clear “repositioning” effect in this survey. With the launch of the ONVO L90 and a rebound in market attention, its positioning within the NIO Inc. ecosystem has been re-recognized by the market, correcting the internal perception inversion seen in the previous period. H2 2025 NEV Brand Health Survey based on perceived positioning In terms of confidence in future development, overall market sentiment improved compared with the previous survey. AITO, Tesla, and BYD remained in the “very strong confidence” tier, while Li Auto and Xiaomi saw notable declines amid sustained negative public opinion. By contrast, the NIO ecosystem showed signs of recovery, with the NIO brand, ONVO, and firefly all moving from the “weak confidence” category to “relatively weak confidence”, easing extreme pessimism in market expectations. H2 2025 NEV Brand Health Survey based on development confidence Within brand image labels, “open innovation” remains the most competitive dimension, with Xiaomi, Xpeng, and AITO representing three distinct approaches. “Traditionalism” continues to be dominated by legacy brands such as Volkswagen, Hongqi, Mercedes-Benz, and Toyota. In the “rigorous and restrained” category, Tesla, Volkswagen, and BYD appeared most frequently. Wey and Volvo ranked near the top in the “safety” label. H2 2025 NEV Brand Health Survey based on brand image labels The concentration of the “success-oriented” label increased further, with Mercedes-Benz maintaining a clear lead. New premium brand Maextro ranked first across several high-end labels. The NIO brand entered the top three for “taste”, while Yangwang and Denza led in the luxury and business-oriented categories, respectively. LandRoads concluded that as NEV penetration continues to rise and the number of brands expands rapidly, mere brand recognition is no longer a core competitive advantage. Preference, perceived positioning, confidence in development, and brand image attributes are increasingly becoming the key factors that differentiate brands in the market.

![BYD launches 4-seat ultra-luxe flagship SUV for $215,000 [Images]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pMC53cC5jb20vZWxlY3Ry-ZWsuY28vd3AtY29udGVudC91cGxvYWRz-L3NpdGVzLzMvMjAyNi8wOC9CWUQtWWFu-Z3dhbmctVThMLTQtc2VhdC5qcGVnP3c9-MTUwMCZhbXA7cXVhbGl0eT04MiZhbXA7-c3RyaXA9YWxsJmFtcDtzc2w9MQ/968bb80271e248ee95003667e96d87fa.jpeg?t=20260808&post_id=52016)