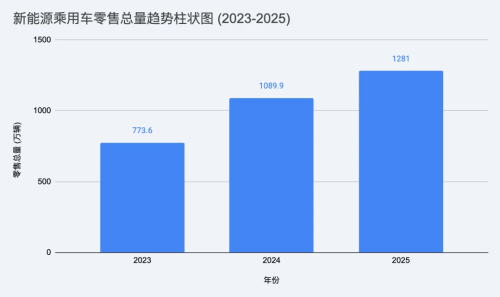

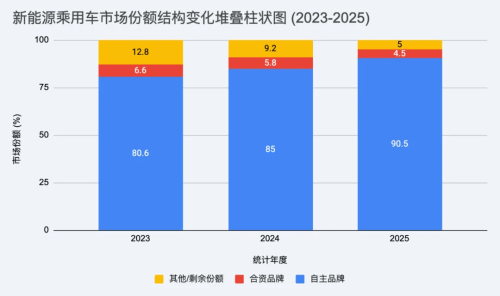

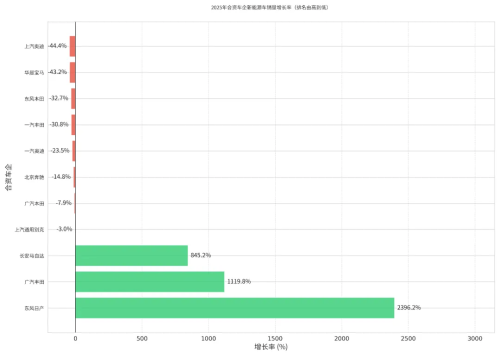

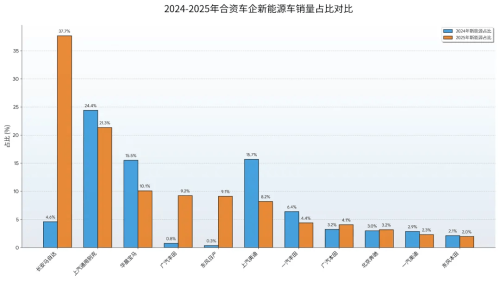

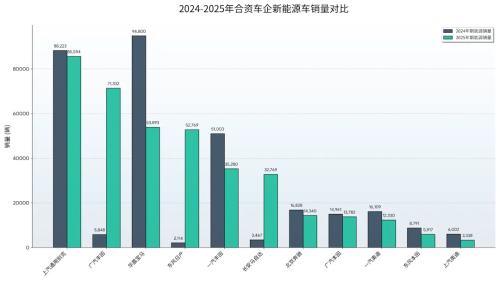

Joint ventures in China’s automotive market face challenges, adapting to local EV strategies while seeing declining market shares. One widely circulated story about the “awakening” of joint-venture carmakers in China resembles the plot of a triumphant web novel. In 2023, Dongfeng Nissan invited senior executives from Nissan Motor, including its CEO, to Guangzhou, where they reviewed more than 30 locally developed new energy vehicles in a single session. The lineup included flagship products from BYD and leading startups such as NIO, Xpeng and Li Auto. Under Nissan’s traditional internal benchmarking approach, the script would typically involve testing competitors’ vehicles, identifying their shortcomings, and reaffirming the strengths of Nissan’s own products. But in 2023, according to LatePost, the scene unfolded differently: the wave of Chinese EVs reportedly left the Japanese executives in stunned silence. Dongfeng Nissan later guided the delegation through the 2023 Shanghai Auto Show, where the dazzling array of Chinese new energy vehicles delivered yet another shock to executives from Nissan headquarters. That experience ultimately paved the way for the dramatically revamped Nissan N7. Whether other joint-venture carmakers experienced similarly dramatic turning points remains unclear. What is certain, however, is that 2025 marked a pivotal year in which joint ventures broadly shifted direction and began studying Chinese domestic automakers in earnest. Beyond Nissan, FAW-Volkswagen and SAIC Volkswagen, SAIC-GM Buick, GAC Toyota, the German “BBA” trio, and even Korean brands all initiated moves. Slower players entered negotiations with Chinese technology firms, while faster ones launched products incorporating Chinese automotive technologies and achieved initial market traction. This model—joint ventures relying on Chinese domestic technology to develop new products—has earned a shorthand label: “JV 2.0.” Its emergence signals that large-scale joint-venture automakers have embarked on a difficult, protracted and challenging transformation. In its first year, the market indeed saw several standout products. In addition to the N7, models such as GAC Toyota’s bZ3X, Buick’s Encasa and Buick Electra L7, Mercedes-Benz’s all-electric CLA, and Audi’s Q6L e-tron all attracted significant market attention. Now that the first full year has passed, which major joint-venture players have truly executed a strategic turnaround? Or at least shown tangible signs of changing course? At its core, the question is whether “JV 2.0” can genuinely boost new energy vehicle sales. As joint ventures draw closer to Chinese EV startups at the product level, are their sales trajectories converging as well? Perhaps the data from 2025 offer the answer. No cooperation, no joint venture Before examining the 2025 performance of joint-venture EV businesses, it is useful to understand current cooperation models between joint ventures and Chinese automakers and suppliers. Classified by product definition, joint ventures’ “JV 2.0” strategies can be broadly divided into three models, based on the depth of Chinese technological involvement. Different paths, same destination The first category comprises products that adopt Chinese technologies for intelligent functions and other core features, while overall vehicle architecture and exterior design remain led by the joint venture. Some models are localized upgrades of global platforms. A representative example is the Mercedes-Benz all-electric CLA. As a global model, the electric CLA in China largely mirrors its overseas counterpart in driving dynamics and interior space, aside from an extended wheelbase. To address Chinese consumers’ strong focus on intelligent features, it incorporates solutions from Chinese suppliers to close the gap with domestic rivals. Such products are common among brands with established market influence, including the German “BBA” trio. In addition to the CLA, FAW Audi’s Q6L e-tron is already on sale, and the next-generation BMW iX3, set to enter China in 2026, also falls into this category. The second category features deeper application of Chinese technologies, extending from surface-level intelligent features to core components such as power batteries and drive systems. Typical examples include SAIC-GM’s new energy vehicles, such as Buick Electra Encasa and Buick Electra L7. It is worth noting that Renault, which has temporarily exited the Chinese market, sourced batteries from CATL and motors from Shanghai Edrive for its global Twingo E-Tech—an unusual but illustrative case. The third category involves products so deeply rooted in Chinese automotive technology that, as industry observers describe it, “only the badge remains foreign.” Representative models include the Nissan N7 and GAC Toyota bZ3X. Their underlying architectures were fully developed by Chinese teams, and core electric and intelligent systems largely originate from China’s domestic technology ecosystem. The Nissan N7’s design language also diverges markedly from Nissan’s traditional styling. Full-width lighting and large in-car displays reflect near pixel-level emulation of Chinese EV aesthetics. Aside from the Nissan badge, the N7’s first impression is that of a quintessential Chinese new energy vehicle. Similar products include the Mazda EZ-6 and EZ-60, SAIC Audi’s E5 Sportback, and Yuzhong 06. Across these three categories, deep cooperation with Chinese partners is the unifying theme, distinguishing these vehicles from earlier joint-venture EVs and enhancing their competitiveness. Viewed from another dimension—the breadth of collaboration—the close ties between joint ventures and Chinese companies have become pervasive across the industry, extending to nearly every segment and reflecting an irreversible market trend. Embracing China China’s automotive supply chain has long been globally recognized and embedded in multiple critical links of the global industry. The turning point came in the new energy era, when joint ventures began entrusting core components—the “chips” and the “soul”—to Chinese suppliers. Examples abound. Horizon Robotics has forged deep cooperation with Volkswagen Group, promoting mass production in 2025 of advanced driver assistance systems based on its Journey 6 chip series. On the software front, certain FAW Audi models have adopted Huawei’s ADS solutions. Momenta is another frequent partner. Beyond Volkswagen, new models from SAIC-GM Buick, GAC Toyota, Dongfeng Nissan and Beijing Benz have integrated Momenta’s driver assistance systems. Cooperation extends further to vehicle architectures. The Yuzhong 08, scheduled for launch in 2026, is built on the “CEA” architecture co-developed by Volkswagen Group and Xpeng. The Nissan N7 is rumored to be redesigned based on the Dongfeng eπ 007 architecture. The AUDI E5 Sportback is built not on the PPE platform but on the ADP platform, jointly developed by Audi and SAIC Group. GAC Toyota’s bZ3X and Mazda’s EZ-6 are even more thoroughly localized. Industry insiders suggest the former is effectively a sibling model to GAC’s new-generation AION V, with Toyota primarily contributing styling input. Similarly, the Mazda EZ-6 shares nearly identical driving experience with the Changan Deepal SL03. Beyond individual products, joint ventures and Chinese partners are deepening cooperation at the foundational capability level, aiming to feed these capabilities back into global markets. Toyota’s two Chinese joint ventures are implementing a “Regional Chief Engineer” system, shifting R&D leadership to Chinese engineering teams. Even core global models such as the Corolla may eventually be led by Chinese engineers. SAIC-GM’s Pan Asia Technical Automotive Center, established jointly with SAIC Group, has long served as a cradle for Chinese automotive engineers and was one of the earliest joint-venture R&D institutions in China. The “Xiaoyao” vehicle architecture and “Zhenlong” powertrain series used in the Buick Electra brand originate there. Volkswagen’s equity investment in Xpeng to co-develop electronic and electrical architectures has been widely discussed. Its subsidiary also formed a joint venture with Horizon Robotics, named CARIZON, to lead driver assistance system development. Nissan, for its part, established Nissan Technology Development (Shanghai) Co., Ltd. These developments indicate that joint ventures’ collaboration with Chinese firms is expanding in both depth and scope, moving beyond intelligent systems into core platform architectures. In other words, EV standards shaped by China’s industry are increasingly becoming a shared benchmark recognized by joint ventures. With this background, the key question is: how well are these new-generation joint-venture EVs selling? Decline, not rise From a macro perspective, 2025 remained a painful year for joint-venture carmakers. According to the China Association of Automobile Manufacturers (CAAM), Chinese brands accounted for 69.5% of total passenger vehicle sales in 2025, implying that joint ventures’ market share fell to roughly 30%. Twelve years earlier, in 2014, joint ventures were at their peak, with market share reaching 66.1% (CAAM data). Six years ago, in 2020, they experienced a second peak at 64% (CPCA data), just before the explosive rise of new energy vehicles. The direct cause of the collapse in joint-venture share is the continued decline of their core internal combustion engine business. In 2020, fuel vehicles accounted for 92.3% of total sales; by 2025, that share had dropped to 46% (CAAM data). Meanwhile, joint ventures failed to fully capitalize on the rapid growth of new energy vehicles. According to the China Passenger Car Association (CPCA), domestic new energy passenger vehicle sales (excluding exports) reached about 12.81 million units in 2025, up roughly 17.5% year-on-year from 10.899 million units in 2024. In terms of market share, domestic brands expanded from about 85% in 2024 to around 90.5% in 2025. Joint-venture brands slipped from 5.8% to approximately 4.5%. These figures underscore two points: joint ventures remain at a structural disadvantage in the new energy passenger vehicle market, and the “JV 2.0” strategy has yet to deliver the anticipated counteroffensive. Despite robust overall market growth, their performance declined rather than improved. However, such outcomes cannot be generalized across all players. A Sustainable Solution? Examining annual changes in new energy passenger vehicle sales among joint ventures, the first year of “JV 2.0” implementation produced striking results for some. Dongfeng Nissan, GAC Toyota and Changan Mazda emerged as major beneficiaries in 2025. Dongfeng Nissan’s new energy vehicle sales surged 2,396.2% year-on-year, GAC Toyota rose 1,119.8%, and Changan Mazda increased 845.2%. Correspondingly, the share of new energy vehicles in total sales rose sharply. Dongfeng Nissan’s ratio climbed from 0.3% to 9.1%, GAC Toyota from 0.8% to 9.2%, and Changan Mazda from 4.6% to 37%. Amid an overall sales downturn, Changan Mazda was one of the few joint ventures to achieve year-on-year growth in both new energy and total sales. Its 2025 total sales reached 87,006 units, with new energy vehicles accounting for 37%, driven largely by the EZ-6 and EZ-60. Yet most joint ventures saw declines in annual new energy passenger vehicle sales. FAW Audi, SAIC Audi, Beijing Benz, BMW Brilliance, SAIC-GM Buick, FAW Toyota, GAC Honda and Dongfeng Honda all recorded year-on-year declines in new energy vehicle sales, with several exceeding 30%. The steepest drop was at SAIC Audi, down 44.4%, followed by BMW Brilliance at 43.2%. A key factor appears to be that many of these underperforming joint ventures did not introduce deeply localized products aligned with the “JV 2.0” model in 2025. BMW’s next-generation electric models will not reach consumers until later in 2026. Dongfeng Honda continues to introduce EVs defined by its Japanese headquarters without substantial localization of intelligent cockpit or driver assistance features. FAW Toyota’s bZ3 has seen intelligent upgrades, but not to the same comprehensive extent as the bZ3X. SAIC Audi launched a new brand, AUDI, in partnership with SAIC Group in 2025, introducing the E5 Sportback outside its traditional brand framework. However, the AUDI E5 Sportback remains in an early ramp-up phase, with cumulative sales below 10,000 units. The contrasting performance data seem to support the argument that the more thoroughly “JV 2.0” is implemented and the more localized the products, the greater the boost to new energy vehicle sales. At a broader level, constrained by global market considerations and strategic inertia, joint ventures are unlikely to rapidly elevate the share of new energy vehicles in the near term. Internal combustion models remain their core volume drivers. The pace and depth of “JV 2.0” implementation will therefore continue to face uncertainties. Nevertheless, the emergence of several “JV 2.0 darlings,” even as global automakers slow their overall electrification transitions, may serve as a catalyst encouraging joint ventures to intensify their new energy strategies in the Chinese market. “JV 2.0” darlings “What were the 10 best-selling joint-venture new energy vehicles in 2025?” That question was recently examined by ChinaEV Home. A brief recap shows that, ranked by annual sales in 2025, the top joint-venture new energy models were GAC Toyota bZ3X, Buick GL8 plug-in hybrid, Nissan N7, Volkswagen ID.3, BMW i3, FAW Toyota bZ3, smart #1, Volkswagen ID.4 Crozz, Mazda EZ-6 and Mazda EZ-60. A closer look reveals that only four of the top ten truly fit the “JV 2.0” definition—models built around core experiences powered by Chinese technology companies—less than half the list. Many others, such as the Volkswagen ID.3 and BMW i3, belong to the previous generation of joint-venture EVs. From another perspective, however, the flagship “JV 2.0” models—bZ3X and Nissan N7—ranked near the top and significantly outperformed other joint-venture EVs in absolute sales. Over the past year, bZ3X sold 70,007 units, while Nissan N7 recorded 45,382 units. The next model, ID.3, posted fewer than 40,000 units, and from the fifth-ranked BMW i3 onward, annual sales clustered between 20,000 and 23,000 units, highlighting a clear gap. It is also worth noting that neither bZ3X nor Nissan N7 was on sale for a full 12 months, making their results indicative of strong market acceptance. Looking back, what distinguishes these “JV 2.0” models represented by bZ3X and Nissan N7? Learning from the right playbook Their electrical architectures may not be the most advanced, nor do they necessarily lead their segments in charging speed, range or acceleration. However, both models excel in interior space, cabin design and intelligent convenience features. The most prominent strength lies in their infotainment systems. Both bZ3X and Nissan N7 adopt design aesthetics and user interaction logic closely aligned with mainstream Chinese EVs, lowering the learning curve for new buyers and enhancing product accessibility. A counterexample is a certain Japanese brand’s EV that insists on using its in-house infotainment operating system without adapting interaction logic or visual design to Chinese consumer preferences. In addition, both bZ3X and Nissan N7 emphasize high equipment levels, echoing a hallmark of Chinese EVs. For instance, Nissan N7 offers an onboard refrigerator system in models priced below RMB 150,000 ($21,000), a rarity in its segment. Its front seats feature 14-point massage functions, an unusually rich configuration at this price level. Space—arguably the top priority for Chinese consumers—is another key advantage. The bZ3X measures 4600*1850*1660 mm with a 2,765 mm wheelbase. While its length matches the Toyota Wildlander, its wheelbase significantly exceeds it and even surpasses the larger Toyota Harrier, traditionally positioned in the RMB 200,000 ($28,000) class. Considering that the bZ3X starts in the RMB 100,000 ($14,000) range, it effectively delivers interior space comparable to RMB 200,000-class gasoline vehicles, alongside an intelligent experience previously unavailable in Toyota’s fuel-powered lineup. Nissan N7 pushes further, with a length of 4,930 mm and a 2,915 mm wheelbase, both exceeding Nissan’s benchmark sedan, the Teana. Although price reductions for the Teana narrow N7’s pricing advantage, the N7 maintains a substantial lead in intelligent features. This strategy—competing across segments with asymmetric strengths—mirrors tactics once favored by China’s EV startups. In essence, bZ3X and Nissan N7 do not rely on secret weapons. Their primary success factor is straightforward: emulating Chinese competitors effectively. By aligning size, intelligence, range and pricing with domestic rivals, they secure a place in consumers’ consideration sets. In contrast, joint-venture EVs that remain unchanged or adhere to legacy thinking operate on a different track—one that assumes brand premium alone can justify comparatively outdated experiences. The 2025 sales data suggest that such a track is narrowing rapidly. Full-scale battle in 2026 Looking ahead to 2026, a new wave of joint-venture offensives is imminent, and the market appears unlikely to grant hesitant players additional time. GAC Toyota has begun pre-launch promotion for the bZ7. Current information suggests a B+ segment sedan comparable in size and positioning to the Camry or Avalon, potentially competing in the RMB 200,000 ($28,000) range and exerting fresh pressure on the joint-venture market. Dongfeng Nissan has already launched the second N-series model, the N6, switching to a plug-in hybrid system with slightly reduced dimensions and lower positioning than the N7. The N-series SUV, NX8, has also entered pre-launch publicity, reportedly larger than the Murano and offering both battery-electric and plug-in hybrid powertrains. If the NX8 is priced between RMB 150,000 ($21,000) and RMB 200,000 ($28,000), replicating the N7’s sales success may not be unrealistic. At SAIC-GM Buick, the 2026 focus centers on the Electra lineup. According to regulatory filings, the SUV E7 will debut first. Positioned alongside the Electra L7, it measures 4,850 mm in length with a 2,850 mm wheelbase and adopts the “Zhenlong Pro” plug-in hybrid system, offering a pure-electric range of 210 km and a projected combined range of 1,600 km. Based on L7 pricing, the E7 is unlikely to exceed RMB 250,000 ($35,000), suggesting competitive potential within the joint-venture mid-size new energy SUV segment. The year 2026 will also mark a concentrated push by the German “BBA” brands. Mercedes-Benz has confirmed the launch of an all-electric GLC built on the MB.EA platform, alongside a potential electric C-Class sedan on the same architecture. The C-Class and GLC SUV are core pillars of Mercedes-Benz’s China portfolio. Built on a new dedicated EV platform and enhanced by intelligent features from Chinese suppliers, these models are expected to gain substantial appeal. As previously noted, BMW will introduce the long-wheelbase electric iX3 based on its Neue Klasse platform in 2026. One of the key highlights among joint ventures will be the direct competition between the electric GLC and electric iX3. Audi will continue expanding its AUDI brand with two additional E-series EVs, while FAW Audi will rely on PPE-platform electric models and advance its “fuel-electric intelligence parity” strategy across both EVs and combustion vehicles. This concentrated effort will likely propel “JV 2.0” to a new peak while accelerating reshuffling within the joint-venture EV market, phasing out legacy models with generational disadvantages. The contribution of “JV 2.0” extends beyond iterative product upgrades. More fundamentally, it reflects a reshaping of joint ventures’ understanding of the Chinese market, user expectations and product definitions. Whether such changes will be sufficient in the long term to sustain competition against wholly foreign-owned EV players—most notably Tesla—and domestic brands remains uncertain. Joint-venture EV volumes are still relatively small, and their structural position remains one of operating within narrow margins. For now, adaptation appears to be the most pragmatic response joint ventures can offer amid intensifying competition. The rapid course corrections demonstrated by some players over the past year have at least added momentum to what promises to be a prolonged counteroffensive. The ultimate outcome remains far from decided.