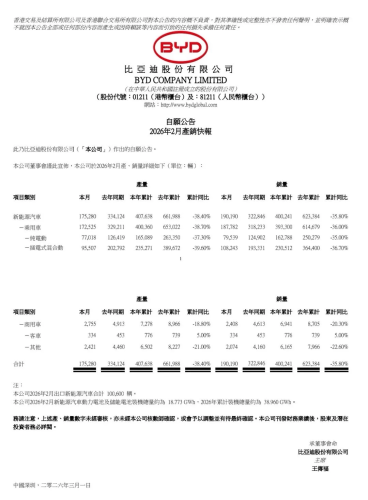

February saw stagnant sales for NEV makers, with mixed year-on-year growth and market preparation ahead. The Lunar New Year has passed and spring has arrived. For the auto sector, however, February remains a traditional low season. The broadly weak market backdrop showed little change and no clear signs of recovery. From a macro perspective, most new energy vehicle (NEV) makers saw limited month-on-month change in February sales compared with January, likely marking one of the lowest points of the year. Year on year, however, shifts in market structure enabled some companies to post solid growth and climb the rankings, while others recorded declines. In any case, February is a pivotal transition month. Carmakers are not attempting to defy seasonality but rather conserving strength during the downturn and waiting for opportunities to counterattack. Looking ahead, most automakers have begun warming up new models in preparation for the April auto show. Others, including Tesla and NIO Inc., have sought to stimulate demand through more aggressive financial incentives. The year-long competitive campaign has only just begun. NIO Inc. NIO Inc. said its three brands delivered a combined 20,797 vehicles in February. NIO Inc.’s delivery data in Feb 2026 Deliveries fell 23.5% from January but rose 57.6% year on year from February 2025. Of that total, the NIO brand accounted for 15,159 units, with the all-new ES8 contributing 11,260 units. Despite being on the market for some time, the updated ES8 continues to show strong momentum. Reliance on higher-value models as sales pillars also implies improved profitability. In its statement, NIO noted that following the Lunar New Year holiday it introduced a series of incentives. For the NIO brand, buyers of the ES8 can receive a RMB 10,000 ($1,400) purchase tax subsidy. The ONVO brand has rolled out more aggressive terms, including a seven-year low-interest financing plan and a purchase tax guarantee under the battery-as-a-service (BaaS) model. On the product front, NIO is not pursuing an aggressive model rollout in 2026. Only the ES9 and L80 have been clearly confirmed. That means existing models will remain the core sales drivers this year, making sustained demand for the ES8, L90 and others critical. Xpeng Xpeng reported relatively muted February deliveries of 15,256 units, down 23.8% month on month and 49.9% year on year. Xpeng’s delivery data in Feb 2026 Since the start of 2026, Xpeng has moved proactively. In January it launched the P7+ and G7 equipped with its “Super Extended Range” system, expanding its product portfolio. Financially, Xpeng has followed Tesla in offering seven-year low-interest installment plans. For now, however, the dual decline suggests that its recent initiatives have yet to deliver the intended impact. In March, Xpeng will launch the next-generation all-electric X9, aiming to strengthen its position in the RMB 300,000 ($42,000) MPV segment. At the higher end, a flagship SUV codenamed GX—priced above RMB 300,000—will offer both Super Extended Range and pure electric variants. Currently, Xpeng has yet to find a second growth driver beyond the M03. Its hit-model strategy has not been sustained, leaving overall sales heavily dependent on a single product and vulnerable to volatility. Whether its Super Extended Range models can gain traction in 2026 may prove decisive for Xpeng’s trajectory. Li Auto Li Auto delivered 26,421 vehicles in February, down 4.5% from January but up 0.6% year on year from February 2025. Li Auto’s delivery data in Feb 2026 Combined January–February data indicate relatively stable performance, suggesting that its battery electric lineup—particularly the i6—has maintained steady delivery volumes without sharp swings. That stability is positive for Li Auto. According to its product plan, the company will refocus on extended-range models in 2026. A stable BEV sales base allows it to concentrate on reviving its extended-range lineup. Its first new model this year will be the next-generation L9. In addition to the standard version, the L9 will offer a more advanced “Livis” variant featuring cutting-edge technologies including the “Mach chip,” described by founder Li Xiang as an “embodied intelligent robot.” For now, greater attention may be on the full-year earnings due March 12. From both capital markets and operational perspectives, 2026 is set to be a challenging year for Li Auto. Leapmotor Leapmotor, the 2025 sales champion among startups, delivered 28,067 vehicles in February, down 12.5% month on month but up 11% year on year. Leapmotor’s delivery data in Feb 2026 Overall, under its current product portfolio, Leapmotor has maintained relatively solid and stable sales without significant fluctuations. Notably, while seven-year low-interest financing has swept the Chinese auto market, Leapmotor is among the few that have not followed suit. That it can maintain leading monthly volumes under such conditions suggests growing customer stickiness. This is also linked to its core price band around RMB 150,000 ($21,000). Higher-end D-series models have been in pre-launch marketing for some time, with the D19 yet to debut and the D99 still in early preview stages. The main upcoming model is the A10, an entry-level vehicle priced below RMB 100,000 ($14,000), expected to launch around the Beijing auto show. It will shoulder the task of replacing the T03 and reestablishing Leapmotor in the entry compact segment. Whether expanding at both ends of the market can help Leapmotor achieve its ambitious one-million-unit annual sales target remains to be seen. Zeekr With 23,867 deliveries, Zeekr may be February’s standout performer among NEV makers. Zeekr’s delivery data in Feb 2026 Deliveries rose 0.1% month on month and surged 70% year on year. Zeekr did not disclose model-level breakdowns or February sales of the 9X. Based on January’s 6,600 units, the 9X is likely its current mainstay. High average selling prices combined with steady, meaningful volumes have made Zeekr’s early-2026 performance notable. Upcoming launches include the 8X and refreshed 007/GT, which could lift volumes further and push Zeekr into a more leading position. On market expansion, Zeekr has begun deliveries in Germany, making 2026 a pivotal overseas year. It has also introduced seven-year low-interest financing across most models. Refocusing on the premium segment, Zeekr remains competitive in China. Xiaomi Auto Xiaomi Auto’s February deliveries fell 48.7% from January to just over 20,000 units, roughly flat year on year versus February 2025. Xiaomi Auto’s delivery data in Feb 2026 The explanation is straightforward. Its mainstay SU7 ceased production in early January, and the updated SU7 is not expected to launch and begin deliveries until April at the earliest. As a result, most February sales were generated by the YU7 alone, with SU7 Ultra volumes negligible, making the sharp decline unsurprising. As noted earlier, February—and even March—will be a period of consolidation for Xiaomi Auto. For the YU7, Xiaomi moved quickly to match Tesla’s policies by offering a seven-year low-interest financing plan. At the recent Mobile World Congress (MWC), Xiaomi also drew attention with its Vision GT concept, attracting global interest. Ultimately, the refreshed SU7 this spring and the potential YU9 (tentative name) later this year will be critical in determining whether Xiaomi’s momentum continues in 2026 or levels off. Voyah Dongfeng-backed Voyah did not disclose standalone February sales, stating only that January–February deliveries totaled 18,873 units. Voyah’s delivery data in Feb 2026 By calculation, February deliveries were 8,358 units, down 20.5% month on month and 47.8% year on year. Compared with peers, Voyah’s performance was subdued, partly due to weaker-than-expected sales of the Voyah Taishan. In recent months, Taishan has averaged about 2,000 units per month, peaking at 3,100 units in December before dropping back to 1,600 in January. Other key models, including the Zhuiguang L and Free+, have not established clear sales advantages, leaving the Dreamer MPV as the mainstay and exposing limited risk resilience. In March, Voyah will launch the Dreamer “Champion Edition,” equipped with Huawei’s Qiankun intelligent driving system, with a pre-sale price of RMB 319,900 ($44,786). While the Dreamer remains a benchmark in the high-end NEV MPV segment, rising competition will intensify pressure. IM Motor IM Motor did not disclose February deliveries, nor did it provide cumulative January–February figures, stating only that January–February sales rose 69.4% year on year. IM Motor’s delivery data in Feb 2026 In January–February 2025, IM delivered 7,037 units, implying roughly 11,921 units in the first two months of 2026. With 5,017 units delivered in January, February deliveries are estimated at 6,904 units, up 37.6% month on month. On that basis, IM’s February performance was relatively solid, making it one of the few brands to post sequential growth. IM noted that cumulative deliveries of the LS6 have reached 100,000 units, forming a stable foundation for the brand. In 2025, IM bet heavily on its “Hengxing Super Extended Range” system, launching models including the LS6 and LS9, which achieved strong results in certain months. In 2026, IM plans to roll out the Hengxing system across more models, including the core L6 sedan. Like Xpeng, IM is wagering on extended-range technology to expand its sales base. Its success or failure will be a key storyline in 2026. Geely Galaxy Geely Galaxy delivered 73,125 vehicles in February, down 11.9% month on month and 3.9% year on year. Geely Galaxy’s delivery data in Feb 2026 In a traditional off-season month, such fluctuations are normal. With no major product offensives in January or February, stable base volumes suggest Galaxy has built solid fundamentals. The main pre-launched model is the Galaxy M7, a five-seat family SUV targeting the RMB 150,000 ($21,000) segment. It is expected to compete directly with the BYD Song Plus family and replace the Galaxy L7, standardizing product naming. Using the M7 as a pivot, Galaxy appears set in 2026 to streamline its lineup, at least in terms of naming consistency. Relying on the Xingyuan to sustain volumes is not a long-term solution. In mainstream sedan and SUV segments, Galaxy urgently needs a true breakout model to support ambitious growth targets. Overseas, Geely Group’s February exports rose 138% year on year, suggesting 2026 could mark a major inflection point for Chinese NEV global expansion. BYD BYD sold 187,782 passenger vehicles in February, down about 8.6% from January and down 41% year on year from 2025. BYD’s delivery data in Feb 2026 Together with January’s performance, the dual month-on-month and year-on-year declines in the first two months are rare for BYD, underscoring intensifying competition. BYD’s sales figures include exports. In February, overseas exports of NEVs reached 100,600 units, implying that domestic monthly NEV sales may have fallen below 100,000 units. On the positive side, BYD has reduced reliance on the domestic market ahead of peers, and February exports edged up from January. On the product front, BYD is warming up two higher-end models, “Da Han” and “Da Tang,” expected to be priced around RMB 300,000 ($42,000). For mass-market entry models, updates are likely to be incremental. BYD appears to be seeking greater success in higher-value segments to offset challenges in the entry market. With a forthcoming “Technology Day” that may unveil next-generation fast-charging and advanced driver-assistance systems, a broader counteroffensive could be in the making.