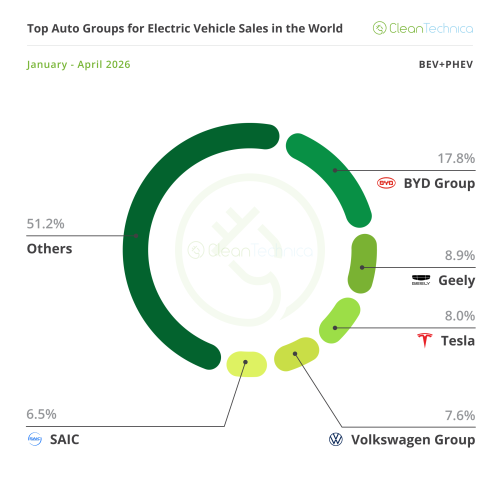

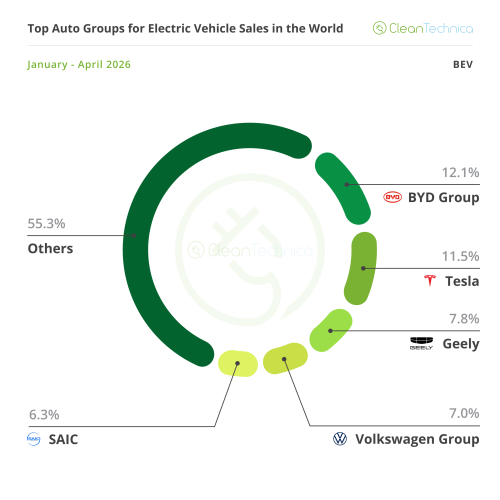

BEVs on the way up, PHEVs on the way down Plugin vehicle registrations were up 9% year over year (YoY) in April, ending the month at around 1.6 million units. Interestingly, BEVs (+19% YoY) and PHEVs (-9% YoY) behaved very differently, with pure electrics back to double-digit growth while plugin hybrids remained in the red. This is the first time since 2019 that PHEVs remained in the red for four consecutive months. This meant that, while the plugin YTD numbers are barely positive (+1% YoY), that is solely due to the PHEV blues (-10% YoY), because BEVs are already on the way back to normal (+7%). And the different dynamics between pure electrics and plugin hybrids are reflected in the BEV vs. PHEV share of plugin sales — in April, BEVs represented 72% of all plugin sales, or about 1.15 million units, one of the best results of the past few years. That led the YTD breakdown to be 70% vs. 30% in favour of pure electrics, which is touching the ceiling of BEV share of the past 12 years. Since 2014, BEVs have floated between 70% and 50% of the total plugin share. The global BEV takeover vs. China and the USA With numbers out of the red zone, it is undeniable that globally, this year started slow. But there is one easy explanation for this — incentives. Or the end of them. The end of US incentives last October, added to the partial removal of incentives in China at the end of 2025, had an expected impact, as these are the 3rd and 1st largest EV markets, respectively. Actually, if we remove China and the USA from the tally, EVs jumped 50% YoY globally in April, with BEVs surging +63% YoY, their highest growth rate since June 2023. Funny enough, PHEVs are also underperforming in this metric, as the 23% PHEV growth rate in April, excluding China and the USA, is the lowest for the technology in over a year. It is starting to look like PHEVs’ current slowdown is more structural than expected…. Just because certain media-friendly markets are down, that doesn’t mean that all markets are down. Here are a few examples of fast growing markets: BEVs jumped 157% in Australia, to 16% share; In Italy, BEVs surged +99% YoY, bringing their share to 9%; In Argentina, BEVs experienced exponential growth, going from less than 100 units in April 2025 to over 1.300 units last month; As for Ireland, BEVs doubled their sales to 3,000 units, or 27% share; In South Korea, BEVs surged 160% YoY, to 36,000 units, or 24% share; In Vietnam, BEVs tripled to 26,000 units, or 43% share; As for Japan, BEVs more than doubled their sales YoY, to 7,000 units, or 2% share; In Indonesia, EV sales were up 93% to 15,000 units, or 18% share; Finally, in Malaysia, BEVs jumped 104% YoY to 6,000 units, or 8% share; So, Keep Calm and Carry On — the EV revolution is in good health, and with what is happening in the Middle East, ICE vehicle sales are going to melt even faster. EV shares Share-wise, April saw BEVs end the month at 17% share, with the tally increasing to 24% if we add in PHEVs. This performance pushed the 2026 plugin share upward, because BEVs increased their share by one point, to 15%, while plugin hybrids remained at 6% share. Therefore, the 2026 PEV share is now at 21%. In 2026, plugless hybrids represent 15% of total sales, one point above of where we were a year ago, which means that over a third (36%) of total car sales globally already have some form of electrification. The global automotive market remains firmly on the path to electrification. Looking at the best selling models, one can see that the Chinese market is recovering fast. There were no legacy OEM representatives in the top 20, and the Tesla Model 3 (20,436 units, down 29% YoY) dropped to 10th. Still, the leader remained the Tesla Model Y (71,510 units, up 31% YoY), which has found a renewed youth thanks to the standard versions and the L three-row body. This was enough to keep the Chinese competition behind it, like the Geely Xingyuan (EX2 in export markets), which completed the podium with some 42,000 registrations. Geely’s small EV is now at cruising speed, compensating for the loss of demand in its domestic market with increased exports. A surprise in the top half of the table was the 3rd position of the BYD Song, no doubt rejuvenated by the new generation Ultra body. Flash charging capabilities promise to recharge the Song’s sales. Another surprise was the 4th position of the BYD Yuan Up/Atto 2. Thanks to a recent refresh and the launch of a new PHEV version, the Up is becoming a star player in the BYD lineup. Rank Model Segment April % 1 Tesla Model Y D 71,510 4.4% 2 Geely Xingyuan / EX2 B 41,617 2.6% 3 BYD Song / Seal U (BEV+PHEV) D 36,103 2.2% 4 BYD Yuan Up / Atto 2 (BEV+PHEV) B 27,097 1.7% 5 Xiaomi SU7 E 26,826 1.7% 6 BYD Seagull / Dolphin Mini B 25,978 1.6% 7 BYD Dolphin C 22,162 1.4% 8 BYD Sealion 06 (BEV+PHEV) D 21,067 1.3% 9 Li i6 D 21,024 1.3% 10 Tesla Model 3 D 20,436 1.3% 11 MG 4 C 17,509 1.1% 12 Qiyuan / Nevo Q05 C 16,334 1.0% 13 Deepal S05 (BEV+PHEV) C 15,911 1.0% 14 BYD Seal 06 (BEV+PHEV) D 15,014 0.9% 15 Leapmotor A10 B 14,372 0.9% 16 FCB Tai 7 (BEV+PHEV) E 14,216 0.9% 17 BYD Yuan Plus / Atto 3 C 13,647 0.8% 18 Xpeng Mona M03 C 13,595 0.8% 19 BYD Qin Plus (BEV+PHEV) C 13,292 0.8% 20 Wuling Mini EV A00 13,238 0.8% Others 1,194,217 73.9% TOTAL 1,615,040 100% Another highlight in the first half of the table is the Xiaomi SU7. Thanks to a recent refresh, it scored 26,826 registrations, allowing it to reach the 5th spot. Looking at the second half of the table, the Xpeng Mona M03 is back in the top 20, at #18, but the highlights are elsewhere: Leapmotor placed its new baby, the A10 small crossover, in 15th, in only its second month on the market, the best career start ever for a model from the startup. That could mean that Leapmotor has found its star player, joining a lineup of consistent performers. Another record scorer was the #12 Qiyuan Q05, with Changan’s mainstream crossover delivering a best ever 16,334 units. Outside the top 20, there wasn’t much to talk about, with the highlight being the fact that the best selling legacy model belonged to BMW. The iX1/X1 PHEV twins registered 11,837 units, ahead of the Skoda Elroq (11,000 units), and two Toyotas (BZ4X and BZ3X, both at around 10,000 units each). Year to date, the leader Tesla Model Y is really in its own league, selling almost three times as much as the runner-up Geely Xingyuan. In fact, looking at overall global sales, the Texan crossover is the only EV present in the top 10, and it is close to the top, just behind the leader Toyota Corolla. Oh, and by the way, next year there will be a Toyota Corolla BEV…. With Toyota now warming up to EVs, this could be huge news. In other news, as expected, the Geely Xingyuan surpassed the Tesla Model 3 and is the new runner-up. Still, not all was lost for the Tesla sedan, as it remained ahead of the #4 BYD Song. But with the Chinese SUV on its way to a new generation and the small Geely Xingyuan said to have a refresh soon, it will be difficult for the Model 3 to retain a podium position, something it held since 2018. Rank Model Segment January–April 2026 % 1 Tesla Model Y D 314,942 5.6% 2 Geely Xingyuan / EX2 B 136,495 2.4% 3 Tesla Model 3 D 119,734 2.1% 4 BYD Song / Seal U (BEV+PHEV) D 119,555 2.1% 5 BYD Seagull / Dolphin Mini B 98,570 1.7% 6 BYD Yuan Up / Atto 2 (BEV+PHEV) B 86,073 1.5% 7 Xiaomi YU7 E 81,538 1.4% 8 Li i6 D 78,112 1.4% 9 BYD Dolphin C 71,642 1.3% 10 NIO ES8 / EL8 E 58,255 1.0% 11 FCB Tai 7 (BEV+PHEV) E 57,227 1.0% 12 BYD Sealion 06 (BEV+PHEV) D 56,787 1.0% 13 MG 4 C 56,194 1.0% 14 BYD Seal 06 (BEV+PHEV) D 54,610 1.0% 15 BYD Yuan Plus / Atto 3 C 54,573 1.0% 16 AITO M7 (BEV+PHEV) E 53,600 0.9% 17 Toyota BZ4X D 50,097 0.9% 18 Deepal S05 (BEV+PHEV) C 45,876 0.8% 19 BMW iX1 / X1 PHEV C 42,532 0.8% 20 BYD Qin Plus (BEV+PHEV) C 42,211 0.7% Others 3,970,018 70.3% TOTAL 5,648,641 100% Below the podium race, the BYD Yuan Up was up one position, to 6th, thus placing three BYDs in the top 6 positions. In fact, there were a couple more BYDs on the rise, with the Sealion 06 jumping five positions, into 12th, while BYD’s premium arm Fang Cheng Bao saw its Tai 7 SUV climb one position, to 11th. The full size yacht, in fact, is now just some 1,000 units behind the category’s reference model, the successful #10 NIO ES8. Elsewhere, the MG 4 compact hatchback jumped three positions, to #13, while we have a new face in the top 20, with the Deepal S05 joining the table at #18. Manufacturers: Leapmotor & Toyota(!) shine Nothing really out of the ordinary happened on the podium, with BYD, Tesla (+11% YoY), and Geely taking over the top three spots. But behind these three, something remarkable has happened — Leapmotor scored a record result, more than 71,000 registrations, ending April in 4th. It thus beat the all-mighty Volkswagen. With a slew of fresh metal coming (A10 small crossover, A05 small hatchback, D19 large SUV, D99 large MPV…), expect the startup’s sales to continue growing significantly, possibly reaching the back of 3rd placed Geely soon. Another highlight was Toyota, which ended the month in 5th with a record 43,944 registrations, fewer than 1,000 units behind #4 Volkswagen! With the BZ3X and BZ4X EVs being the backbone of Toyota’s strength, and with a few models ramping up (C-HR+ EV and BZ7), one can actually be optimistic about Toyota’s prospects for this year. Especially when one thinks that Toyota has that rare thing — selling in large volumes in all three main EV markets (China, Europe, and the USA), and using tailor-made models for each of them (BZ3X and BZ7 in China, C-HR+ and Urban Cruiser in Europe, and BZ4X and Highlander EV in the USA). Rank Brand April % 1 BYD 273,448 16.9% 2 Tesla 96,129 6.0% 3 Geely 91,001 5.6% 4 Leapmotor 71,387 4.4% 5 Volkswagen 47,770 3.0% 6 Toyota 43,944 2.7% 7 BMW 39,935 2.5% 8 Wuling 39,530 2.4% 9 Kia 37,303 2.3% 10 Xiaomi 36,711 2.3% 11 Li Auto 34,085 2.1% 12 Mercedes 33,877 2.1% 13 Deepal 33,187 2.1% 14 Qiyuan / Nevo 32,118 2.0% 15 Zeekr 31,787 2.0% 16 MG 31,107 1.9% 17 Xpeng 31,011 1.9% 18 Aion 29,829 1.8% 19 Audi 29,280 1.8% 20 FCB 29,138 1.8% Others 610,710 37.8% TOTAL 1,615,040 100% With the Japanese make already close to the legacy leader, Volkswagen, the next big target for Toyota will be a podium position. Will it be able to get there? Please place your bets. Regarding the remaining positions on the table, another surprise was the record scores of Changan’s EV brands, the mainstream Qiyuan and its premium sister Deepal. The first was 14th, with 32,118 registrations, while the second was 13th, with 33,187 registrations. Both made it here thanks to the success of their compact crossovers, the S05 in the case of Deepal, and the Q05, in the case of Qiyuan. As for the year-to-date table, there was no major news in the top positions, and we have to go down to the 6th position to see position changes. But what a change we got…. Leapmotor jumped six positions, to … 6th. It should continue to climb positions in the coming months, with the next victim being #5 BMW, fewer than 100 units ahead. Even #4 Volkswagen is within target range, so I wouldn’t be surprised to see the German brand fall to 5th in the second half of the year. Or even drop to 6th … because behind Leapmotor, we have another rising power. Toyota was up to 8th in April, and seems sure to continue climbing positions throughout the year. The Japanese make currently seems to be the legacy brand with most potential. Rank Brand January–April 2026 % 1 BYD 853,253 15.1% 2 Tesla 452,959 8.0% 3 Geely 339,479 6.0% 4 Volkswagen 169,144 3.0% 5 BMW 153,529 2.7% 6 Leap Motor 153,475 2.7% 7 Wuling 142,105 2.5% 8 Toyota 134,371 2.4% 9 Kia 131,079 2.3% 10 Li Auto 129,227 2.3% 11 Mercedes 118,275 2.1% 12 Xiaomi 117,557 2.1% 13 Zeekr 114,275 2.0% 13 MG 109,481 1.9% 15 Audi 108,566 1.9% 16 Aion 105,098 1.9% 17 Hyundai 103,439 1.8% 18 Volvo 98,831 1.7% 19 AITO 96,027 1.7% 20 Xpeng 93,693 1.7% Others 1,924,778 34.1% TOTAL 5,648,641 100% Looking at the second half of the table, Xiaomi was up one spot, to 12th, while Volvo climbed one position, to 18th, despite having a slow month — not even joining April’s top 20. Lucky for them, AITO had an even worse month (it’s like that saying — to escape a lion, you don’t have to run fast, you just need to be faster than the guy running next to you). Therefore, it allowed the Swedish make to surpass it. A final mention goes out to Fang Cheng Bao, which ended at #21, some 2,000 units behind #20 Xpeng. With exports now starting to gain relevance, BYD’s premium arm could gain enough momentum to join the table soon. And even #22 Deepal, with its current record streak, can hope to join the table in the coming months…. Looking at OEMs, BYD (17.8%, up from 17.1% in March 2026) is stable in the lead, while runner-up Geely (8.9%, down 0.3%) continues in the slow lane, as a number of its brands (Volvo, Lynk & Co, Smart…) aren’t performing as expected. #3 Tesla (8%, down from 8.9% in March) had its expected drop from an off-peak month, but stayed ahead of Volkswagen Group (7.6%, down 0.1%), so it seems that the OEM is guaranteed a podium position this year. Rank OEM (BEV+PHEV) 2026 % 1 BYD 1,003,093 17.8% 2 Geely 504,650 8.9% 3 Tesla 452,959 8.0% 4 Volkswagen Group 430,286 7.6% 5 SAIC 366,043 6.5% Others 2,891,610 51.2% TOTAL 5,648,641 100% #5 SAIC remained in 5th, gaining some ground over newly 6th placed Chery (4.3%, up 0.8%), which is gaining significant traction in export markets thanks to its multiple brands (Jaecoo, Omoda, Jetour, iCar, etc.). #8 Changan (3.9%) is also on the rise, thanks to EV brands Qiyuan and Deepal, and Toyota is also starting to appear on the radar, with the Japanese OEM now in 10th with 2.8% share, having surpassed Stellantis in April. Looking just at BEVs, there were about 4 million registrations so far this year, or 70% of total plugin sales. Will they end the year above 75%? If so, that would be their best result since 2012.... At the top, Tesla (11.5%, down 1.3%) lost the leadership position to BYD (12.1%, up 1%), with the question now being — will Tesla recover the lead in June? I doubt it. With BYD ramping up deliveries of the second generation of its Blade Battery, expect sales to pick up, allowing the Shenzhen OEM to easily regain the leadership position. Rank OEM (BEV) 2026 % 1 BYD Group 478,765 12.1% 2 Tesla 452,959 11.5% 3 Geely 307,138 7.8% 4 Volkswagen Group 276,326 7.0% 5 SAIC 247,863 6.3% Others 2,187,926 55.4% TOTAL 3,950,977 100% In 3rd place we have Geely (7.8%), keeping #4 Volkswagen Group at bay (7%, down 0.2% share). Meanwhile, #5 SAIC (6.3%) is comfortable in the last position of the top 5, as #6 Hyundai–Kia (4.9% share, down 0.1%), seems to have slowed down in April.