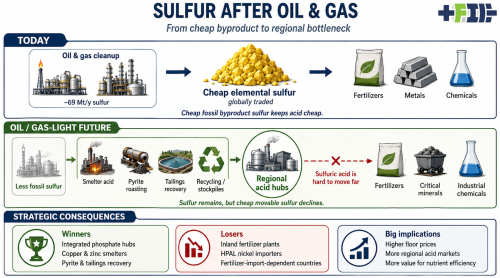

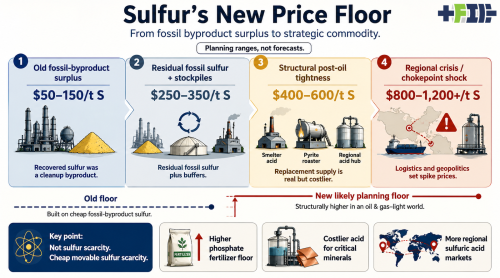

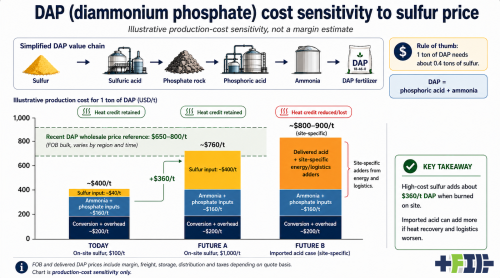

When people think about the Strait of Hormuz, they think about oil tankers, LNG carriers, naval escorts, insurance premiums, and the price of gasoline. They generally do not think about yellow piles of sulfur beside gas plants, phosphate fertilizer complexes, or the acid circuits that keep copper and nickel processing running. They should. The current sulfur price spike is not just another commodity-market twitch. It is a preview of a future in which the cheap sulfur system created by oil and gas cleanup is much smaller, while much of the demand for sulfur remains. Sulfur is not glamorous. It does not have lithium’s battery glow, copper’s electrification story, hydrogen’s marketing department, or uranium’s fan club. It is a basic industrial input that mostly disappears into sulfuric acid. That acid then disappears into phosphate fertilizer, metal leaching, mineral processing, chemical production, wastewater treatment, and a long list of industrial uses. For agriculture, the most important part is phosphate fertilizer. For critical minerals, it is leaching and processing. For the energy transition, it is another reminder that decarbonization changes industrial supply chains in places people were not looking. The Strait of Hormuz matters because it is a chokepoint not only for crude oil and LNG, but also for sulfur flows and the energy inputs that make fertilizer. The Gulf region is one of the large sources of recovered sulfur, and disruptions there hit an already tight market. In the short term, this is about shipping, war risk, inventories, and contracts. In the long term, the more interesting point is that a decarbonized world creates a similar constraint by a slower route. Hormuz imposes suddenly what decarbonization imposes gradually. Less oil refining, less sour gas processing, and less heavy sour crude production mean less recovered sulfur. Infographic of sulfur’s future value chain and implications by author with ChatGPT For roughly fifty years, sulfur has been cheap for a strange reason. Oil refineries and sour gas plants had to remove it anyway. Sulfur in fuels is a pollution problem. Regulations forced the oil and gas industry to take sulfur out of refined products and gas streams, and the industry recovered it as elemental sulfur. The sulfur was not the main product. It was the cleaned-up contaminant. That is a very different cost structure from opening a mine, building a roaster, managing residues, and producing sulfur deliberately. That point is easy to miss because sulfur looks like a normal commodity. It has prices, contracts, ports, piles, and customers. But its modern abundance has been tied to another system’s cleanup requirement. Cheap sulfur was an accident of fossil fuel processing. The world built fertilizer, mining, and chemical supply chains around that accident. That worked while oil and gas volumes were high and heavy, sour, sulfur-rich streams were being processed. It works less well in a future where heavy sour crude is left in the ground first, sweet light oil is directed mostly toward petrochemicals, and natural gas demand declines. The current elemental sulfur market is about 70 million tons per year. The broader sulfuric acid market is much larger by mass because one ton of sulfur makes about 3.06 tons of sulfuric acid. A sulfuric acid market around 285 million tons per year contains roughly 93 million tons of sulfur. Those two numbers are related, but they are not the same market. Elemental sulfur can be moved as a solid. Sulfuric acid is heavy, corrosive, hazardous, and harder to move long distances. That distinction matters a lot. Today’s sulfur chain is simple enough in concept. Oil and gas cleanup produces elemental sulfur. The sulfur is formed, stored, shipped, and burned near users to make sulfuric acid. Phosphate fertilizer complexes use that sulfuric acid to react with phosphate rock, producing phosphoric acid and phosphogypsum. The phosphoric acid is then turned into MAP, DAP, TSP, NPK blends, animal feed phosphates, and other products. Sulfuric acid also goes into copper leaching, nickel HPAL, uranium, rare earth processing, industrial chemistry, and other uses. The largest demand area is phosphate fertilizer. That is where sulfur becomes food system infrastructure. A ton of DAP contains 46% P2O5 and needs roughly 0.4 tons of sulfur in the upstream acid chemistry. That means every $100 per ton increase in sulfur adds about $40 per ton to DAP production cost before logistics, conversion, financing, and margin effects. When sulfur is $100 per ton, that is an annoyance. When sulfur is $500 per ton, the sulfur input is about $200 per ton of DAP. When sulfur approaches $1,000 per ton, the sulfur input alone is about $400 per ton of DAP. That is not a rounding error in fertilizer economics. The old low-price regime put sulfur in the $50 to $150 per ton range for long stretches. That world was built on fossil byproduct abundance. A managed transition world might put sulfur in the $250 to $350 per ton range. A structurally tighter oil and gas-light world could easily live in the $400 to $600 per ton range. Regional crises, shipping disruptions, export restrictions, or sudden HPAL nickel demand can push sulfur into the $800 to $1,200 per ton range. The point is not that every future year looks like a crisis. The point is that the old fossil byproduct floor is unlikely to be the future floor. Infographic of sulfur structural price regime future by author with ChatGPT Sulfur is not scarce in the geological sense. The United States Geological Survey and other mineral sources are clear that sulfur exists in crude oil, natural gas, sulfide ores, evaporites, gypsum, anhydrite, coal, oil shale, and other geological forms. But agriculture and mining do not need sulfur atoms somewhere in the crust. They need tens of millions of tons of sulfur or sulfuric acid in the right form, in the right place, on the right contract, at the right price. The credible replacement sources are real, but none are as easy as recovered fossil sulfur. Smelter acid from copper, zinc, lead, and nickel sulfide processing is the strongest non-fossil pathway. Sulfide ores release sulfur dioxide during smelting, and modern plants capture it into sulfuric acid. That acid is already a large part of global acid supply. It can grow as more metals are processed, especially copper and zinc. But smelter acid is tied to smelter locations. It appears where the metals are processed, not necessarily where phosphate fertilizer plants, nickel laterite projects, or farmers need it. Pyrite and pyrrhotite roasting are also real. Pyrite is iron sulfide, and roasting it makes sulfur dioxide that can be converted into sulfuric acid. This was historically important before recovered sulfur from oil and gas became cheap and abundant. It could return in some regions, especially where pyrite is already present in tailings, waste rock, or polymetallic deposits and where local acid demand is high enough. But this is not a magic switch. Pyrite roasting needs mines, concentration, roasters, gas cleaning, arsenic and impurity management, residue handling, water, permits, energy, and acid customers. Stockpiles, recycling, residual fossil sulfur, and geological backstops all matter, but they are not the same kind of answer. Western Canadian sulfur piles can buffer shocks, but stockpiles are not annual production. Spent acid regeneration and industrial recycling should expand, but they are small compared with a 70 million ton per year elemental sulfur market. Residual petrochemical and gas processing will continue to produce sulfur for decades, but not enough to anchor the system if oil and gas volumes decline deeply. Evaporites, gypsum, anhydrite, and native sulfur are long-run backstops, not the first cheap replacements. The logistics problem is the part that deserves more attention. Today’s model works because elemental sulfur moves better than sulfuric acid. A fertilizer producer can import sulfur, burn it on site, integrate the acid plant with heat and steam systems, consume the sulfuric acid immediately, manage phosphogypsum in a permitted stack, and ship finished fertilizer. That is a coherent industrial system. It is not elegant, but it is practical. In the oil and gas-light future, more sulfur appears as sulfuric acid near smelters or pyrite roasters. That sounds convenient until the map is opened. The acid may be near a copper smelter in one region. The phosphate rock may be in another. The ammonia may come through a port somewhere else. The gypsum stack has to be permitted at the plant. The farmers may be on another continent. Moving sulfuric acid long distances is possible, but it is not like moving sulfur prills, ammonia, potash, wheat, or finished DAP. It requires specialized tanks, railcars, ships, handling systems, storage, insurance, and safety controls. It is a dangerous and expensive liquid to move at large scale. That means the future sulfur constraint is geographical as much as chemical. The winners are likely to be integrated hubs with two or three of the required pieces in the same place. Phosphate rock plus sulfur access plus port logistics is powerful. Smelter acid plus local mining demand is powerful. Pyrite waste plus acid demand plus permits can be powerful. A lonely inland fertilizer plant that depends on imported acid is not powerful. It is exposed. Phosphate fertilizer is the main place where this meets food. Wet-process phosphoric acid starts with phosphate rock and sulfuric acid. The process produces phosphoric acid and large volumes of phosphogypsum. A 1 million ton per year P2O5 phosphoric acid complex can need roughly 2.6 to 3.5 million tons of phosphate rock and around 2.3 million tons of sulfuric acid, containing about 0.75 million tons of sulfur. It can also produce about 5 million tons of phosphogypsum per year. These are giant industrial material movements with permitting, water, waste, and transport attached. For DAP and MAP producers, the sulfur price swing is direct. Using the 0.4 tons of sulfur per ton of DAP rule of thumb, moving from $100 sulfur to $500 sulfur adds about $160 per ton of DAP. Moving from $100 sulfur to $700 sulfur adds about $240 per ton. Moving from $100 sulfur to $1,000 sulfur adds about $360 per ton. If DAP is selling for $650 to $800 per ton, those numbers can erase margins or force fertilizer prices higher. The impact then reaches farm budgets through higher phosphate costs. Infographic of DAP fertilizer price sensitivity by author with ChatGPT This does not mean food prices rise one-for-one with sulfur. Farmgate crop prices, inventories, subsidies, exchange rates, ammonia prices, potash, diesel, shipping, credit, weather, and demand all matter. But sulfur sets a higher floor under phosphate fertilizer. When phosphate fertilizer gets more expensive, farmers respond. Some reduce applications where soil phosphorus is high. Some draw down soil fertility for a year or two. Some shift crop mixes. Some invest more in soil testing, variable-rate application, manure logistics, digestate, and agronomy. Some simply absorb lower margins until they cannot. The ammonia overlap matters because DAP and MAP use ammonia as well as phosphoric acid, while nitrogen fertilizers are even more directly exposed to gas and ammonia. The same Strait of Hormuz shock that exposes sulfur also exposes LNG, natural gas, ammonia, and urea. Sulfur and ammonia are different commodities, but they meet in the same fertilizer complex and the same farm budget. That is why the shock feels larger than a single commodity move. The structural implication is not agricultural collapse. Farmers are adaptive, fertilizer markets adjust, production shifts, and nutrient efficiency improves when inputs are expensive. The more likely outcome is a higher cost floor for high-input agriculture, more volatility in fertilizer-import-dependent countries, and higher value for nutrient efficiency. Corn, wheat, and rice are more exposed than soybeans and pulses. Soybeans fix much of their nitrogen, but they still need phosphorus and potassium. Pulses become more attractive in some rotations, but they do not replace the calorie and feed roles of maize, wheat, and rice. Precision agriculture gains value in this world, although not in the simplistic way technology vendors sometimes claim. Expensive inputs make better application more valuable. A 10% saving on a $220 per acre fertilizer bill is worth more than a 10% saving on a $120 per acre bill. Variable-rate nutrient application, better soil maps, optical nitrogen sensing, split applications, nitrification inhibitors, manure integration, digestate, and agronomic advice all become easier to justify. But low farm margins also reduce farmers’ ability to buy expensive equipment. The likely winners are tools with short payback periods, service models, retrofits, and trusted agronomy, not only shiny capital-intensive systems. Industrial winners and losers become clearer. Integrated phosphate hubs win if they have rock, sulfur access, ammonia links, gypsum management, and ports. Copper, zinc, and lead smelters win if their sulfuric acid has local or regional value. Mining districts win when they can use acid near where it is produced. Pyrite and tailings recovery projects win if they can meet environmental standards and connect to acid demand. Countries with residual sulfur recovery or stockpiles gain strategic leverage. Fertilizer plants far from sulfur, acid, ports, or phosphate rock lose. HPAL nickel projects dependent on imported sulfur lose. Fertilizer-import-dependent countries face more food-system exposure. This also changes how critical-minerals projects should be valued. Nickel HPAL is already acid-hungry. Copper leaching needs sulfuric acid. Some rare earth, uranium, and battery-material processing chains need acid too. If a project’s cost model assumes sulfur returns to $100 per ton as a permanent normal, it is probably understating risk. A serious project finance model should include sulfur at $400 to $600 per ton as a structural case and $800 to $1,000 per ton as a regional stress case. The key question is not only the acid price. It is where the acid comes from, how it gets to site, whether the contract is long term, and what happens when shipping or geopolitics interfere. Policy makers should be paying attention because sulfur sits in the awkward space between agriculture, mining, trade, and decarbonization. Countries should map sulfur and sulfuric acid dependency. They should identify where smelter acid, pyrite, tailings recovery, phosphate fertilizer, and mineral processing can be linked in real industrial hubs. They should stress-test fertilizer and critical-mineral projects against sulfur prices far above the old fossil byproduct norm. That is not glamorous policy, but neither is fertilizer. Both matter. The policy answer is not to keep burning oil and gas to get cheap sulfur. That would be a poor answer to a real problem. The answer is to recognize that fossil fuels provided more than energy. They also created byproduct economies. Sulfur is one of them. As fossil fuel use declines, those byproducts either shrink, reprice, or have to be replaced deliberately. Deliberate production is usually more expensive than accidental abundance. That is not a case against decarbonization. It is a case for sober industrial planning. There are wrong conclusions to avoid. The world is not running out of sulfur. Pyrite is not a frictionless replacement for recovered fossil sulfur. Smelter acid is not automatically available where phosphate fertilizer plants need it. Stockpiles are not a permanent supply chain. High sulfur prices do not guarantee a permanent food crisis. But low sulfur prices from the fossil cleanup era should not be assumed either. This is not depletion. It is repricing. The Strait of Hormuz shock is useful because it makes an invisible dependency visible. It shows what happens when sulfur is no longer treated as an abundant cleanup byproduct and starts behaving like a strategic industrial input. In a decarbonized world, sulfur will still exist. Fertilizer will still be made. Copper, nickel, and industrial chemicals will still use sulfuric acid. But the system will be more regional, more capital-intensive, more exposed to logistics, and more expensive than the fossil byproduct system it replaces. The central lesson is simple. Modern agriculture and mining were built in part on cheap sulfur from oil and gas. As the world moves away from oil and gas, sulfur does not disappear, but the cheap arrangement does. The future price of sulfur is unlikely to be the old $50 to $150 per ton world. It is more likely to sit structurally closer to today’s stressed market than most fertilizer, mining, and policy models assumed a few years ago. The sooner that is treated as a supply-chain design problem instead of a temporary commodity spike, the less painful the adjustment will be.

![Great News, The Strait Of Hormuz Is Now Open To Anyone Willing To Pay A Multi-Million-Dollar Toll To The Iranian Government [Update]](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly93d3cuamFsb3BuaWsuY29t-L2ltZy9nYWxsZXJ5L3N0cmFpdC1vZi1o-b3JtdXotbm93LW9wZW4tbWlsbGlvbi1k-b2xsYXItdG9sbC1pcmFuL2ludHJvLTE3-NzU2NzY0OTQuanBn/f4f44f9f5e2cbd0f58e74f25a5a5d408.jpg?t=20260721&post_id=12330)