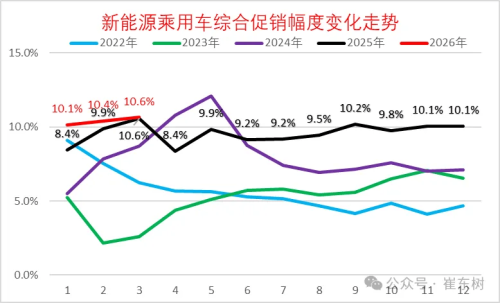

Latest data released by Cui Dongshu, Secretary General of the China Passenger Car Association, shows that in March 2026, the average price of discounted new energy vehicles stood at RMB 286,000 ($41,470), with an average price reduction of RMB 34,000 ($4,930), representing a decline of about 12%. Average price cus for new passenger vehicles in China from 2020 to Mar 2026 This level is broadly in line with the overall passenger vehicle market decline of 12.1%, indicating that the price war is shifting from rapid price cuts to a more stable phase. By comparison, internal combustion engine vehicles saw slightly larger declines. The average transaction price was RMB 257,000 ($37,265), with a reduction of RMB 32,000 ($4,640), or about 12.5%. In terms of the number of discounted models, 18 models saw price cuts in March, down by seven from a year earlier but up by nine from February. New vehicle price adjustments for different vehicle types from 2020 to Mar 2026 Among them, six were internal combustion and hybrid models, one fewer year-on-year, while five were battery electric models, eight fewer than the same period last year. Specifically, the five battery electric models with price reductions in March included the Arcfox Alpha S5, Denza Z9, JMC Yi, XPeng X9, and Aeolus L7. The model with the largest price cut was the JMC Yizhi EV, with its starting price reduced from RMB 129,800 ($18,821) over the past two years to RMB 79,800 ($11,571), marking a 39% decline. Denza Z9 and Aeolus L7 followed with price reductions of 24%. XPeng X9 and Alpha S5 saw price cuts of RMB 50,000 ($7,250) and RMB 11,000 ($1,595), corresponding to declines in the range of 9% to 14%. NEV price cut percentages in Mar 2026 In contrast, plug-in hybrid and range-extended models showed more restrained pricing adjustments, mostly around 6%. For example, the Yangwang U8 saw a price reduction of RMB 90,000 ($13,050), while the Aion i60 dropped by RMB 7,000 ($1,015), reflecting largely structural adjustments. Beyond direct price cuts, promotional strategies are also evolving. In March, overall promotional intensity for NEVs reached 10.6%, remaining at a relatively high level, broadly flat year-on-year and up slightly by 0.2 percentage points from the previous month. Promotional discounts of China’s NEVs from 2022 to Mar 2026 Hybrid models saw promotional intensity of 19.9%, while plug-in hybrid, range-extended, and battery electric vehicles recorded 10.6%, 9.3%, and 11.1% respectively. Meanwhile, dealers are increasingly adopting low-interest financing schemes and other incentives in place of direct price reductions to alleviate margin pressure. Promotional strategies also vary across different groups. European brands showed the highest promotional intensity at 38.7%, significantly above the industry average. Other joint-venture brands were around 24%, while domestic brands maintained a more restrained level at approximately 19%.