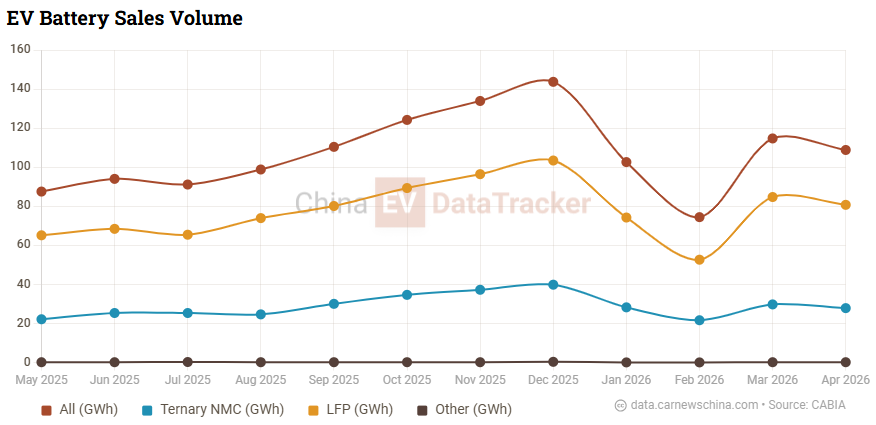

Ganfeng targets EV, robotics, and low-altitude battery applications. Image enhanced by CNC Understand China EV’s Market Real-time notifications when critical EV data is released All important data in one place 2,000,000+ data points Become a member Ganfeng Lithium said its 400 Wh/kg solid-state battery has exceeded 1,100 charge cycles and completed engineering validation, while the company’s 500 Wh/kg-class 10Ah lithium-metal battery has entered small-batch production, according to Sina. Ganfeng described the 500 Wh/kg-class 10Ah cell as the world’s first product of its type to achieve small-batch production. The update was disclosed in an investor relations activity record published on May 20. The company said it is advancing both silicon-carbon and lithium-metal anode routes simultaneously as part of its solid-state battery strategy. Lithium-metal push According to Ganfeng Lithium, the 400 Wh/kg battery has achieved a cycle life of over 1,100 cycles and has demonstrated potential for large-scale applications. The company also said its 500 Wh/kg-class 10Ah product became the world’s first lithium-metal battery in this category to enter small-batch production. The company identified lithium-metal anodes as a core technology for accelerating commercialization of higher-energy-density batteries. Ganfeng previously stated that its second-generation semi-solid battery (liquid-solid state battery) uses metallic lithium as the anode material. The company also produces lithium-metal materials that can be used as raw materials for solid-state batteries. The company said both battery routes are aimed at overcoming commercialization barriers and accelerating mass production of high-energy-density cells. Silicon-based route Alongside lithium-metal development, Ganfeng said it is also expanding silicon-based anode products with energy densities of 320–480 Wh/kg. Its 320 Wh/kg cell exceeded 1,000 cycles, while the 480 Wh/kg technology remains under development. The company said the different configurations are intended to meet varying requirements for energy density and cycle life across different applications. Potential applications include premium new energy vehicles, drones, eVTOL aircraft, robotics, and consumer electronics. Expanding solid-state race China’s solid-state battery sector has accelerated in 2026 as battery makers and automakers push toward pilot production and vehicle integration. Earlier this month, a Chinese startup, Pure Lithium, announced plans to expand its 500 MWh production capacity after a cut test continued to operate. Separately, CATL and BYD received awards for next-generation battery development at China’s inaugural Golden Lithium Awards event. Ganfeng is also connected to several Chinese automakers pursuing solid-state programs. The company has previously supplied and cooperated with Dongfeng and Changan. Dongfeng has already begun extreme-cold testing of 350 Wh/kg solid-state battery vehicles, while Changan plans to trial installing 400 Wh/kg solid-state batteries in 2026. Market backdrop According to China EV DataTracker, China’s EV battery installations reached 108.9 GWh in April 2026, up 25.8% year-on-year. LFP batteries accounted for 80.8 GWh, representing 74.2% of the market, while ternary NMC batteries accounted for 27.9 GWh, with a 25.6% share. The figures illustrate that conventional lithium-ion chemistries still dominate the market even as companies increase investment into solid-state technologies. EV battery sales volume in China. Credit: China EV DataTracker