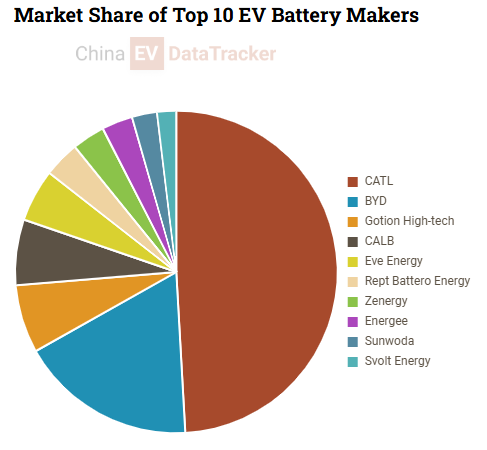

Chinese researchers advance solid-state battery prototypes to achieve higher energy density and faster charging. Image enhanced by CNC. Understand China EV’s Market Real-time notifications when critical EV data is released All important data in one place 2,000,000+ data points Become a member China says it faces the risk of being overtaken in the global solid-state battery race despite holding one of the world’s largest research pipelines and patent portfolios in the sector, according to XHN. A new Chinese industry and policy analysis describes all-solid-state batteries as a strategic technology entering a critical phase of industrialisation, while warning that the United States, Europe, Japan, and South Korea are accelerating policy support, industrial coordination, and patent deployment. China accounts for approximately 35% of the global solid-state battery patent market, making it the largest in this segment. Chinese electrolyte-related patents represent about 39% of worldwide filings, the highest share among all countries. However, Japan remains the largest source of technology, accounting for around 37% of global patent filings, compared with roughly 30% from China. Research output reaches global peak China’s annual publication volume of solid-state battery research papers increased from 21 in 2015 to 562 in 2023, ranking first globally. Key institutions, including the Chinese Academy of Sciences, the Institute of Metal Research under the Chinese Academy of Sciences, and Tsinghua University, were cited for advances in solid-solid interface engineering, a core technical bottleneck in commercialisation. Global solid-state battery-related patents reached 16,429 as of November 2025, covering 6,321 unique patent families. China and Japan lead total patent applications with 3,341 and 3,225, respectively, followed by the United States with 2,355 and South Korea with 1,544. Corporate patent concentration remains uneven Despite China’s large-scale activity, the report notes a gap in top-tier patent concentration. Among the world’s top 30 institutions in solid-state battery and electrolyte patents, Japanese companies account for 17 positions, Chinese firms for 7, South Korean firms for 5, and European companies for 1. The top 10 institutions are entirely Japanese or South Korean. Toyota is identified as the largest corporate patent holder in the sector, accounting for approximately 40% of global solid-state battery patents. Chinese companies, including CATL, BYD, and SVOLT, are among the leading recent patent applicants, with Chinese entities filing more than 500 applications in 2023 alone. CATL, Ganfeng and Gotion advance pilot production The report states that the industry is moving from pilot-scale development toward limited small-batch production, with early manufacturing expected around 2027 and broader commercialisation targeted for 2030. Recent corporate disclosures and research breakthroughs highlight the accelerating pace of development activity. Chinese researchers recently unveiled a 451.5 Wh/kg solid-state battery prototype with claimed three-minute charging capability. Separately, Changan-backed Ganfeng Lithium reported a solid-state battery achieving 1,100 cycles with 400 Wh/kg energy density, while targeting 500 Wh/kg for future production applications. CATL has also disclosed patent activity on fluorine-containing lithium compounds and sulfide electrolyte systems to improve fast-charging performance and thermal stability. Gotion High-tech has completed design work for a 2 GWh all-solid-state battery production line, while a 0.2 GWh pilot line is already in operation with vehicle testing underway. Market share of top 10 EV battery Makers by battery installations in China. Credit: China EV DataTracker Expanding applications beyond electric vehicles While electric vehicles remain the largest application area, the report states that solid-state battery development is increasingly extending into humanoid robots, electric vertical take-off and landing aircraft, consumer electronics, and energy storage systems. These applications are described as emerging demand areas for high-energy-density battery systems, though no deployment timeline was provided. China’s EV battery market remains highly concentrated among a small number of major suppliers. CATL led installations with 29.06 GWh and a 47.2% market share in the latest available period, followed by BYD with 10.49 GWh and a 17.1% share. Gotion High-tech ranked third with 4.05 GWh and a 6.6% share, according to China EV DataTracker. Technical pathways and structural challenges remain Solid-state battery development continues across three main electrolyte routes: sulfide, oxide, and polymer systems. The report states that no single dominant technical pathway has emerged, with each route presenting trade-offs in conductivity, stability, cost, and manufacturability. Key unresolved challenges include lithium dendrite formation, ion transport mechanisms, solid-solid interface engineering, and battery failure mechanisms. The report also highlights gaps in overseas patent deployment, noting that Chinese companies file fewer international patent applications than their Japanese and South Korean peers, which maintain broader patent coverage across the United States, Europe, Southeast Asia, and India. China’s first national solid-state battery standard, titled “Terms and Classification,” is currently open for public consultation. The draft proposes classification into liquid, hybrid solid-liquid, and solid-state categories.