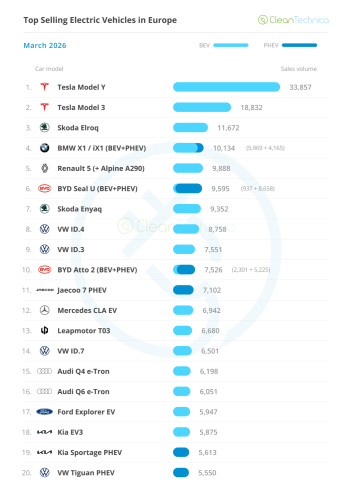

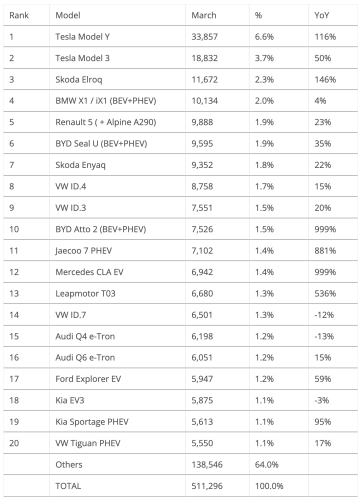

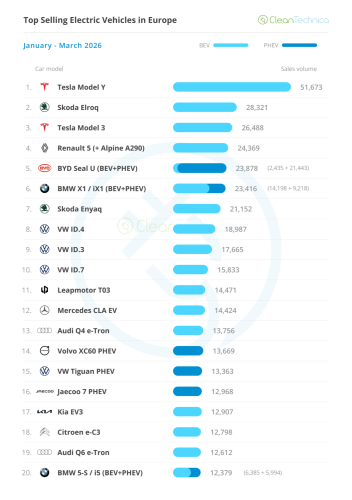

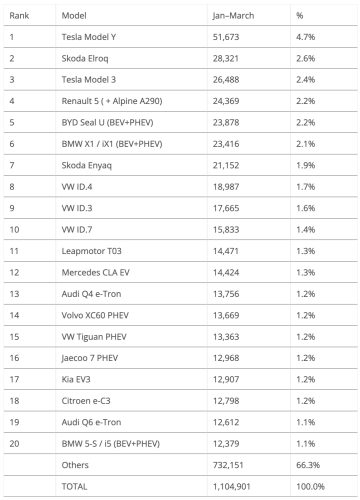

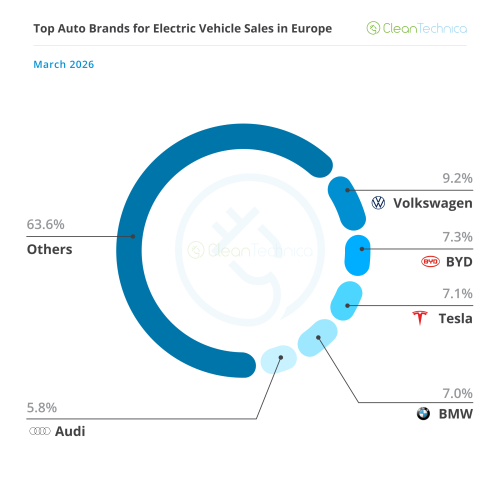

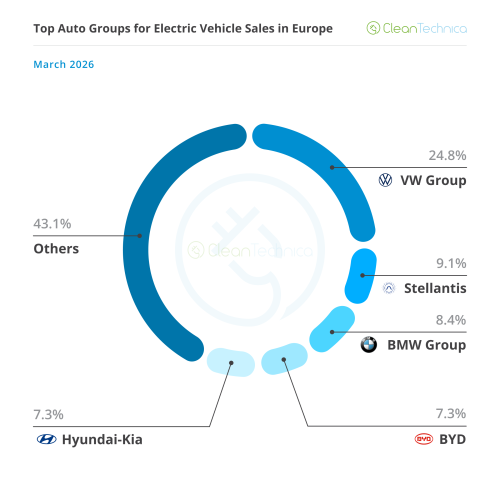

BEVs reach 22% market share! Thanks to a number of factors (new, cheaper and/or better models, record high gas prices, mass arrival of Chinese models, etc.), EVs have risen to record highs in Europe, with over half a million plugin vehicles being registered in Europe in March, 349,000 of them being BEVs. Overall, plugin vehicles were up 39% YoY, while BEVs did even better, jumping 42% YoY. The overall market also had a positive month in March, rising 11% YoY to one million units. That pulled the YTD performance into positive numbers, +4% YoY. Looking at the March powertrain breakdown, one can see that while ICE vehicles are melting (with petrol down 10% YoY, to 22% share, and diesel down 14% YoY, to 6% share), plugless hybrids still managed to grow slightly above the market average (+15%). However, it’s really plugins that are the ones pulling the market upwards — with BEVs surging 42% to 22% share and PHEVs going up 34% to 10% share. Adding the 38% market share of HEVs to the 22% of BEVs and the 10% of PHEVs, this means that a record 70% of all new cars in Europe had some sort of electrification. With both BEVs and PHEVs achieving record results in March, the year-to-date share for BEVs went up to 21% (31% for PHEVs and BEVs combined), a significant 6% share advance over the 25% PEV share registered in the first quarter of 2025. At this pace, we should be close to 100% PEV share by … 2035? 2036? What do you think? Just to give some context, five years ago, in Q1 2021, the PEV share was 15% (7% BEV), less than half of what it is now, and in Q1 2016, the market share for PEVs in Europe was slightly above … 1%. Yep, that’s how far we’ve come. Ten years ago, we were happy to report that March 2016 had a near record month of … 24,000 units. Now, we are at over half a million. (Easter Egg — doing the same exercise for China, while we are now at 45% PEV share, five years ago we were celebrating PEV share climbing to 10%, and ten years ago … it was at 0.8% share. And March 2016 had a now measly 18,000 registrations…. Still, some trends were already settled back then, BYD was the leader, by far — 39% share — and a then young adult BYD Qin was already in China’s top 10, while Tesla was the only foreigner on the table, with the Model S in 8th.) Looking at the best selling models, the big news this month was Tesla placing two models on the podium. Here’s a more detailed analysis of the top 5 EVs this month: #1 Tesla Model Y — Tesla’s midsize crossover is back in the driver’s seat, thanks to 33,857 registrations in March, which is its best result in three years! This represented a 116% jump YoY, mostly thanks to the mass deliveries of the cheaper standard version, allied to the sudden surge in demand that BEVs experienced in March due to the Iran war and the subsequent surge in gas prices. People wanted EVs they could take home the day they went into the store, and Tesla had just that…. With Model Y prices starting at €40,000, and after six years on the market, the crossover still offers an appealing package. Comparing it with the comparable competition and a similar starting price, we have: the base versions of the Toyota BZ4X and VW ID.4 and the BEV version of the BYD Seal U, and all have less range than the base Model Y (in the case of the Toyota, it’s almost 100 km less range). They all also charge slower than the Tesla (with only the Toyota coming close — 150 kW, compared to the 175 kW of the Model Y), and all of them have less interior space than Tesla’s star player. Currently, you buy a Tesla with your wallet/head, not your heart. Which is exactly the kind of buyer that is now searching for EVs, the ones that want to lower their running costs by switching from ICEVs to BEVs. (Also, it’s why they are so popular with Ubers and such.) #2 Tesla Model 3 — Tesla managed to make a #1 plus #2 win, placing the previous star player Model 3 in 2nd thanks to 18,832 registrations in March, a 50% increase YoY and its best score since June 2024. Benefiting from the same tail winds that its Model Y had (mass delivery of the standard version, surge in EV demand), the 10-year-old sedan could be on the verge of a second spring, now that price-conscious buyers are in the market and its prices, starting around 35,000 EUR, place it, a midsize sedan, in competition with models one segment below, compact hatchbacks. So, while the heart of the midsize car market is probably lost for the Model 3, a new segment of buyers, somewhere between the C and D segments, could give it a second wind. Turns out, Tesla’s sedan could even recover its podium position in 2026 … which is no mean feat for a 10-year-old model wearing a body type (sedan) not popular in Europe. #3 Skoda Elroq — The Elroq won another podium presence in March, thanks to 11,672 registrations, which is a 146% increase YoY (in March 2025, the Czech was still ramping up production). Looking ahead, towards the second half of 2026, the problem for the Czech crossover is that around mid-2026, a new, smaller, and more affordable Skoda crossover will land. Called the Epiq, that model should steal lots of sales from the current star player of the Skoda lineup, as it will be simultaneously cheaper and more modern than the Elroq. So, while the first half of 2026 might see the Elroq run with the Teslas, later in the year, we should see it lose pace and see other models gain ground. #4 BMW iX1/X1 PHEV — The German twins are in cruise control, winning another top 5 position in March thanks to 10,134 registrations, a 4% increase YoY. Benefitting from favorable lease rates to help things along, the BMW crossovers are still the brand’s bread and butter models. Still, help is on the way — with the much hyped iX3 landing this month, the crossover twins can now rest a little. And with a deep refresh coming later this year, promising to transform them into baby Neue Klasse, expect both, but the iX1 in particular, to upgrade their specs, making them far more interesting than the current versions and allowing the Bavarian brand to make its compact models a perfect escort for the iX3 superstar. #5 Renault 5 (inc. Alpine A290) — Renault’s star player delivered 9,888 sales in March, with the iconic hatchback increasing its sales year-on-year by 23%. Looking at its 2026 performance, with production already ramped up and demand now at cruising speed, now is the time for the French twins to show their true value. Will they replicate the success of their Renault Zoe predecessor? No matter how attractive the 5 is, the truth is that in 2026, its space on the market will be squeezed not only by external competition (VW ID.Polo, Cupra Raval, etc.), but also by internal competition, with the equally cute new Twingo stealing sales from below and the appealing 4 crossover doing the same from above. And let’s not forget the Nissan Micra, which is basically a Renault 5 in a Kenzo suit…. Outside the top 5, in a record month, there were a number of models with record scores. The highlights came from China, with two very different EVs hitting best ever results, although through different paths. The #11 Jaecoo 7 PHEV scored a record result in March, 7,102 units, a result heavily based in the UK — the British bought around two thirds of all Jaecoo 7 EVs sold in Europe last month. Maybe it’s the Range Rover Evoque looks for half the price strategy, but one thing is certain — Brits love it. Another surprise was the Leapmotor T03, which was 13th thanks to 6,680 units, it’s second record score in a row! This is much thanks to the shocking results in Italy, with the Chinese EV collecting 5,022 units in that market alone, allowing it to be 3rd overall, only behind the Fiat Panda and Jeep Avenger. So, when Stellantis says that EVs are not ready for prime time … this kind of result says something different. It’s Stellantis EVs that are not ready for prime time. City car lover Italy is switching to EVs … just not from the usual players. I mean, city cars are Fiat’s strong point, and even in its domestic market, these are being taken away by a Chinese company. If that isn’t an alarm bell…. But not all records came from China, as Mercedes’ new baby, the CLA EV, achieved a new record result in March, 6,942 registrations, no doubt thanks to the new station wagon body and cheaper versions. In 2026, the German make is pulling out all the stops to be in a better position in 2027 than it was in 2025. And for that, in March, not only is Mercedes pushing the CLA to new heights, but it has also landed not one but two(!) new models in that same month (and I thought only BYD and Geely could pull that trick…). The GLB EV seven-seater and the GLC EV midsizer both just landed. Sure, the GLB has landed with some real volume (1,074 units) compared to the GLC (385 units), but the truth is that the GLB has much less competition to deal with, making it a star player for the brand. The GLC, meanwhile, has a certain BMW iX3 in its crosshairs … but more on this later. Elsewhere, the Skoda Enyaq was 7th, with 9,352 registrations, its best result in 17 months, with the Czech automaker milking all it can from its current flagship EV. Meanwhile, BYD once again placed the BYD Atto 2 (euro-spec Yuan Up) on the table, with it rising to 10th in March thanks to the new PHEV version representing two thirds of the Atto 2’s sales. Looking specifically at PHEVs, one can see the difference that tariffs make. In the BEV top 5, four models are made in Europe and there’s only one Made-in-China EV, the Tesla Model 3. In the PHEV top 5, it is a much more balanced picture — #1 & #2 are Chinese (BYD Seal U PHEV and Jaecoo 7 PHEV), #3 is Korean (Kia Sportage PHEV), and only the #4 VW Tiguan PHEV and #5 Volvo XC60 PHEV are made in Europe. Outside the top 20, the biggest highlight goes to the official landing of the much awaited BMW iX3. With Tesla-like efficiency, top-grade specs (800 km/500 mi WLTP range, 400 kW charging rate, etc.), and a new, attractive design, the German midsizer represents a new generation of BMWs, and more broadly the best EV globally that is ready to take on the world’s best, including ICE, models. With the upcoming Volvo EX60 and (if we are benevolent) the Mercedes GLC EV, these models represent Europe’s most competitive premium BEVs on the market, with long waiting lists to prove it. And with close to 5,000 units (4,858, to be exact), in its debut month, one can say that the iX3 landed with a bang, so a top 20 position should be possible in a couple of months, if not already by April. Top 10? Could very well be possible, once the production ramp-up is sorted…. But there is more to mention besides the new Beemer. Despite beating its record score, with 5,421 registrations, the Citroen e-C3 wasn’t able to reach the table, making it another month without any Stellantis model in the top 20. Are those alarm bells ringing?!? Toyota also landed its C-HR+, a new BEV unrelated to the hybrid C-HR but with the same philosophy and market position. The Japan-made EV landed with a quite solid 2,323 registrations, thus presenting good arguments for a top 20 position. Concerning the Volkswagen Group galaxy, the Spanish brand Cupra had a great month, with the Born hatchback scoring 4,603 registrations, its best score since December 2023. Meanwhile, its crossover counterpart, the Tavascan, hit a record 4,520 registrations. Regarding the namesake brand, while the ID.x models are in wait and see positions, as we wait for their deep refreshes, players on the bench were able to shine — the ID.Buzz scored a record high 2,954 registrations, and the VW Golf PHEV had a record month thanks to 5,027 registrations, its highest score in its 12-year career! As for BYD, besides the Seal U and Atto 2, already in the top 20, two other players are showing top 20 potential, and none of them are the Seagull Dolphin Surf — the Seal 6 is benefiting from its station wagon body to win popularity in Europe (a record 4,937 registrations), while the Sealion 7 also hit a record score (4,232 registrations), providing a more premium alternative for those who find the Seal U a bit too utilitarian. That is one of BYD’s strengths — the lineup is so vast that it can adapt to whatever a specific market requires. Looking at the 2026 ranking, the major change in the top positions was the ten-position jump of the Tesla Model 3, into the 3rd spot. The midsizer’s strong result in March helped it to join the podium, but with the three models below being fewer than 3,000 units behind, Tesla’s sedan will have a tough time keeping the bronze medal. The French twins in particular will make the Texan’s life hard. As for the remaining changes, one has to go down to the bottom half of the table to see them, with the Mercedes CLA EV jumping three positions, to #12; the Audi Q4 e-tron benefiting from the Volvo XC60 PHEV’s slow month to climb to #13; and the Ingolstadt make also celebrating the return of the Q6 e-tron to the table, at #19. The Jaecoo 7 PHEV celebrated its record March by joining the 2026 table at #16, while the Kia EV3 was up two positions to #17. As for the plugin auto brand ranking, the leader, Volkswagen, remained in the lead (9.2%), holding a comfortable advance over new runner-up BYD (7.3%, up 0.4%). BYD climbed one position in March thanks to volume deliveries in the usual places (UK, Italy, Spain, Germany…), as well as in other not so usual markets, like Azerbaijan and Albania. So … will BYD be able to go after Volkswagen in Europe? Place your bets. But the biggest change happened below BYD. Tesla (7.1% share, up from 5.3% in February) came out of nowhere and jumped into the 3rd position, displacing previous runner-up BMW (7%, down 0.1%) into the 4th position. But with the iX3 now starting its career, expect the German make to recover some ground in the coming months. The race for the 3rd spot will be quite interesting! Bring on the popcorn, because this will be fun! As for #5 Audi (5.8%, down 0.2%), keeping the 5th spot will be a tall order, not only because #6 Mercedes is just 20 units behind and the three-pointed-star brand has a LOT of fresh metal coming in this year (GLB, GLC, VLE, VLS, C-Class…), but also because #7 Skoda (5.5%) will introduce two brand new BEVs in 2026, the small Epiq and the large Peaq. Both will surely increase the total volume of sales from the brand. Expect the Czech make to increase its market share. On the other hand, Audi has … not much, actually. Besides a couple of refreshes, later in the year there will be a new A2 e-tron and … that’s it. All while the Q6 e-tron should suffer from the competition of the three new Musketeers — BMW iX3, Volvo EX60, and Mercedes GLC EV. Arranging things by automotive group, Volkswagen Group is firmly in the lead, despite losing 0.9% share in March. It is now at 24.8% share, a market share that is comparable to BYD’s in China and Tesla’s in the USA. This is an important metric for the German conglomerate if it wants to stay relevant in a fully electrified global automotive market. If you can’t win at home…. #2 Stellantis and #3 BMW Group were both down, but the prospects are quite different — while the multinational OEM’s drop was significant (down 1.1% share to 9.1%) and has no end in sight, the German OEM’s drop was manageable (8.4% now vs 8.7% in February), and with the new iX3 surely adding significant volume to the tally in the near future, BMW should recover some ground, while at same time surpassing Stellantis maybe as soon as May. Rising BYD (7.3%, up 0.4%) has surpassed the Korean Hyundai–Kia duo (7.3%, down 0.1%), now pushed to 4th place. While fewer than 1,000 units separate these two, their current market dynamics say that the Chinese OEM will surely leave the Koreans behind. Outside the top 5, Tesla (7.1%) jumped into the 6th position, replacing a struggling Geely (6.5%, down from 6.7% in February), which is suffering from poor results from its Volvo brand. Still, with the Swedes now focussing on landing the EX60 as soon as possible, expect Geely to rebound soon.