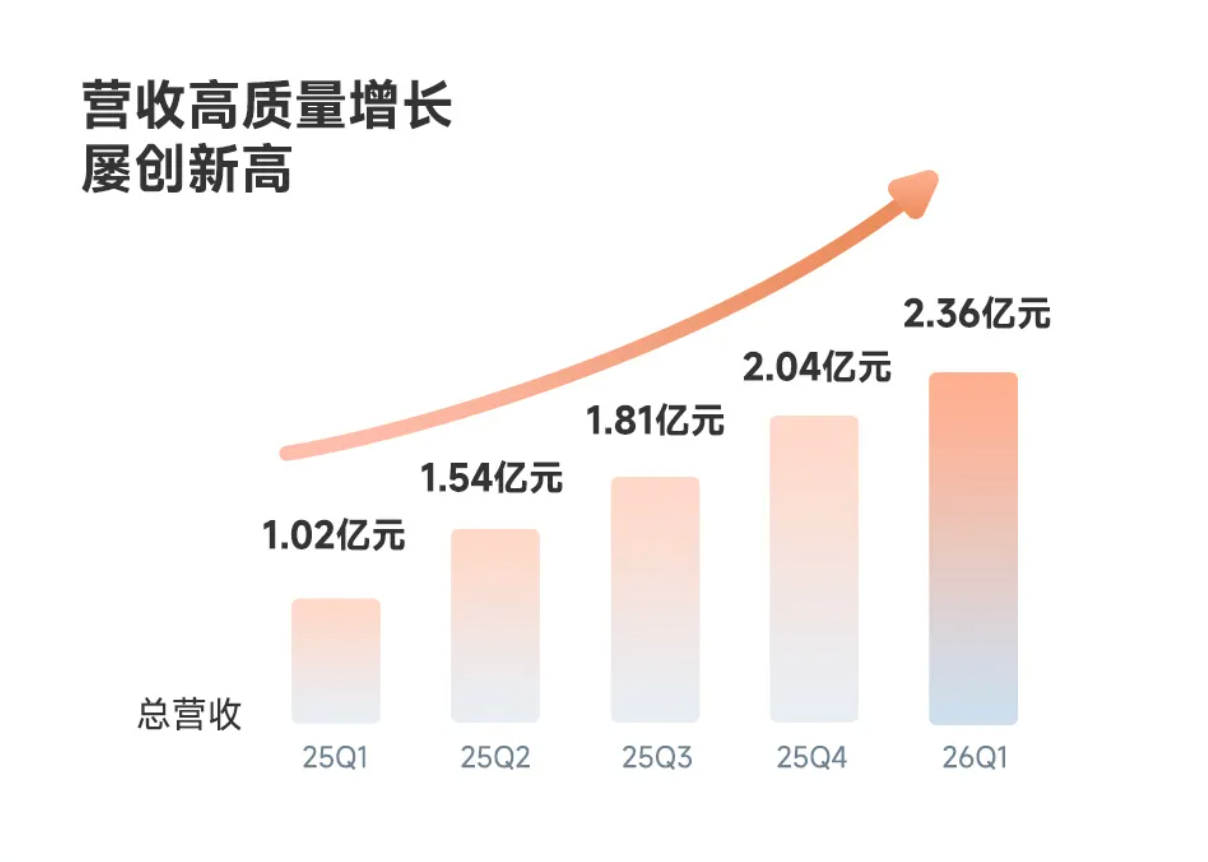

Gasgoo Munich-The race for autonomous driving in 2026 has finally hit a critical commercial turning point. It's no longer just about accumulating test miles or securing funding; real revenue growth has become the new yardstick for measuring a player's value.On May 26, Pony.ai released its scorecard for the first quarter of 2026. The standout figure: quarterly revenue from its Robotaxi business hit 59.12 million yuan, a staggering surge of 395.4% year-on-year. That single number alone eclipses more than half of the entire 2025 revenue for the unit. Consequently, Pony.ai raised its full-year Robotaxi revenue target from "triple 2025 levels" to "more than 3.5 times," while bumping its fleet size goal from 3,000 to over 3,500 vehicles.On the earnings call, Pony.ai executives explained that the raised expectations are driven by strong commercial momentum in the first quarter. The company observed that across all Tier-1 Chinese cities, revenue, paid orders, and user bases continue to expand. Notably, operations in Guangzhou and Shenzhen have turned profitable on a per-vehicle basis, offering a replicable success model. Furthermore, a "joint fleet" model has attracted a slew of domestic and international partners, promising to boost capital efficiency and accelerate deployment.This sends a clear signal: leading autonomous driving companies are crossing the threshold from "cash-burning experiments" into a new phase of "scale expansion."Shifting Revenue Mix: Fares Surge 456.5%, Robotaxi Breaks the 'Spring Festival Slump'A closer look at Pony.ai's Q1 revenue structure reveals a pivotal shift. While smart solutions still account for the lion's share of revenue, the core engine driving this high growth is no longer B-side technology licensing—it's tangible payments from C-side passengers.The report shows total revenue of 236 million yuan for the first quarter, up 145% year-on-year. Of this, the Robotaxi business—often dismissed as a "future story"—contributed 59.12 million yuan, growing nearly fourfold. More crucially, fare income paid directly by passengers soared 456.5%, becoming the primary growth driver. This means ordinary users are voting with their feet and truly opening their wallets for driverless services.Image source: Pony.ai (same below)Pony.ai CEO Peng Jun emphasized on the call that even though Robotaxi pricing remains higher than entry-level ride-hailing, user demand is robust. Service stability and repurchase rates continue to improve, particularly during peak hours and in complex urban scenarios.Industry wisdom has long held that the first quarter, encompassing the Lunar New Year, is a travel lull where Robotaxi volume and revenue usually take a hit. Pony.ai's data suggests that while this pattern hasn't been entirely shattered, its impact has been significantly blunted. The report reveals that paid orders maintained month-on-month growth even around the holidays. That momentum has spilled into the second quarter: weekly average paid orders in May were up 119% compared to January, while daily paid orders during the May Day holiday exploded by 544% year-on-year.This resilience stems from expansion on two fronts:First is the rapid scaling of the fleet. As of May 24, Pony.ai's Robotaxi fleet surpassed 1,700 vehicles. Newly added Toyota bZ4X Robotaxis have begun fully driverless testing and will be deployed in several Tier-1 cities within the year. More importantly, Pony.ai made a bold pledge at the 2026 Beijing Auto Show: by 2027, it will cap the cost of a complete vehicle—including the car, battery, and kit—at under 230,000 yuan. If achieved, this price point would shatter the cost bottleneck for commercialization.Pony.ai CFO Wang Haojun stated that the decline in BOM costs relies on three levers: enhanced purchasing power from fleet expansion, system simplification and optimization based on real-world data from seventh-generation vehicles, and strengthened supply chain management. The company expects to hit this cost target by mid-2027.Second is a strategic breakout in operational geography. Domestically, services have entered downtown Guangzhou for the first time, covering landmarks like Canton Tower and the Pazhou Complex. Internationally, Pony.ai launched Europe's first commercial Robotaxi service in Zagreb, Croatia, and initiated driverless testing in Dubai. Currently, its operations span nine countries, with public passenger services open in five.Peng Jun noted that overseas expansion is central to the company's vision of "making autonomous driving within reach." Pony.ai has already launched commercial Robotaxi services in Croatia, Qatar, Singapore, and South Korea. Moving forward, it plans to work closely with regulators and partners to expand its footprint to over 20 cities globally by year-end.Diversified Revenue Streams: Robotruck and Smart Solutions Advance in TandemWhile Robotaxi grabs the spotlight, Pony.ai's other two business lines—Robotruck (autonomous trucks) and smart solutions—are also finding their rhythm. Together, they form a more complete commercialization loop.Take the Robotruck business first. Revenue reached 70.33 million yuan in Q1, up 31% year-on-year. While that growth lags Robotaxi, the strategic upgrade is key. In April, Pony.ai announced a full-scene freight layout covering "trunk line logistics + city delivery": the fourth-generation pure electric heavy truck enters mass production in the second half of the year, and the first fully automotive-grade, fully redundant light truck has already debuted.Peng Jun explained that the L4 light truck fills the crucial "city delivery" gap in the logistics map. It shares the same software stack and operational infrastructure (such as remote assistance and ground networks) as the Robotaxi, cutting operating costs by half and simultaneously reducing daily overhead for Robotaxi services. The company has co-developed this model with CATL and established partnerships with leading logistics firms, aiming to launch scaled operations early next year.The commercial logic is straightforward: rapidly replicate the algorithms and operational experience honed by Robotaxi into freight scenarios. Internal calculations show that per-kilometer costs for unmanned urban delivery could drop by 40% to 50% compared to manual driving. This is a B-side market that is more cost-sensitive yet more willing to pay. Once scaled, the cash flow potential is significant.Then there is the smart solutions business. Revenue hit 107 million yuan in Q1, surging 246.5% year-on-year, making it the largest contributor to total revenue. The core product is the autonomous driving domain controller, with Q1 shipments growing more than sixfold from last year. Where is the demand coming from? Low-speed delivery vehicles, unmanned sweepers, logistics trucks, and even humanoid robots.The potential here lies in not building cars, but selling "brains." As various robots and specialized vehicles move toward automation, demand for standardized, automotive-grade domain controllers is set to explode. Pony.ai is modularizing and exporting its autonomous tech, positioning itself as a light-asset "seller of shovels."Underpinning all this is a continuously improving financial model. In the first quarter, despite revenue doubling, operating losses remained flat year-on-year and narrowed by 21% quarter-on-quarter. As of the end of March, Pony.ai held nearly 10 billion yuan in cash and investments. In an industry where capital is generally scarce, ample funding and narrowing losses provide the confidence needed to keep expanding.