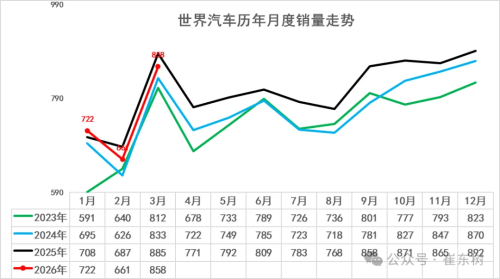

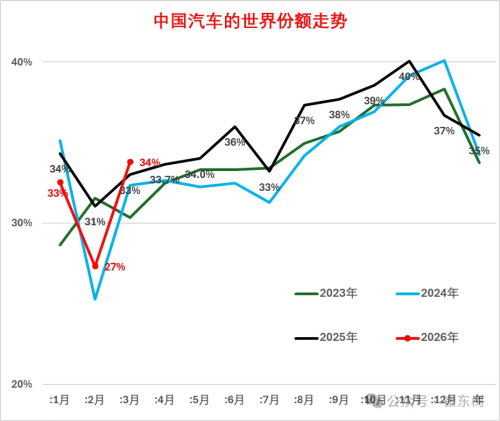

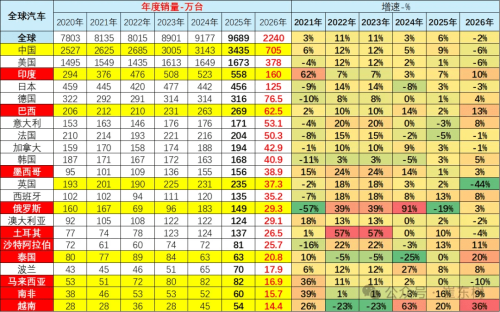

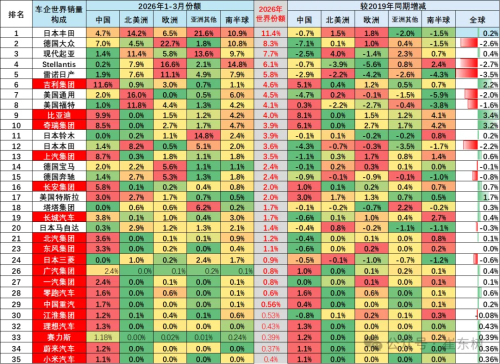

Cui Dongshu, Secretary General of the China Passenger Car Association (CPCA), released a sales analysis report on China’s automobile market for January–March 2026. The report points out that, affected by factors such as slower‑than‑expected growth in the Chinese auto market at the beginning of the year, the global growth momentum has significantly slowed down. From January to March 2026, global car sales reached 22.40 million units, down 2% year‑on‑year. Among them, China’s car sales were 7.05 million units, a year‑on‑year decrease of 6%, which was lower than the earlier forecast for the beginning of the year. World auto monthly sales trend over the years In terms of market share, China accounted for approximately 31.5% of the global market in the first quarter, down 4 percentage points from 35.4% for the full year of 2025. In the short term, the Chinese New Year factor in February was the main disturbance causing the share decline. Looking at specific months, China’s share of the global market was low in January–February but rebounded to 34% in March. As the effects of policy stimulus gradually appear, the Chinese auto market is expected to continue strengthening from the second quarter onward. Trend of China’s global market share Looking at the trend of China’s share in the global automobile market, China’s share of world car sales has increased year by year from 32% in 2020, reaching a historic high of 35.4% in 2025. Entering 2026, although greatly affected by holidays and policies, the market share declined significantly in January–February but showed a recovery trend in March. Trends of major national markets worldwide Looking at individual countries and regions, the performance of major automobile markets is clearly divergent: U.S. sales fell 6%; Germany benefited from the restart of new energy vehicle subsidies, showing a market recovery; emerging markets performed relatively well – India’s auto market grew by 10%, Thailand’s market grew by 20%, and Russia’s market also achieved 3% growth. Trends of major national markets worldwide From the perspective of overall group performance, a trend of “rising East, falling West” is evident – Chinese independent (self‑owned) brands are comprehensively increasing their global market share, while the shares of major international automakers are declining significantly. In the world auto manufacturer ranking for the first quarter of 2026, Geely Group ranked 6th with a global market share of 4.6%; BYD ranked 9th (4%); Chery Group followed closely with 3.9%. Compared with the same period of 2019, the sales of the three groups increased by 2.2%, 3.4% and 3.2% respectively. In contrast, traditional international giants generally face pressure. Among them, the second‑ranked Volkswagen Group, despite holding an 8.3% share, saw a decline of 2.6 percentage points compared with 2019. Stellantis held a 6.1% share, and Renault‑Nissan held a 5.8% share, down 2.7 and 3.5 percentage points respectively year‑on‑year. It is worth noting that Toyota Group performed relatively steadily, with a first‑quarter share of 11.4%, up slightly by 0.2 percentage points from 2019, mainly due to its strong performance in the North American and European markets. South Korea’s Hyundai‑Kia held a 7.7% share, also up 0.4 percentage points from 2019, but its performance in China remained persistently weak.