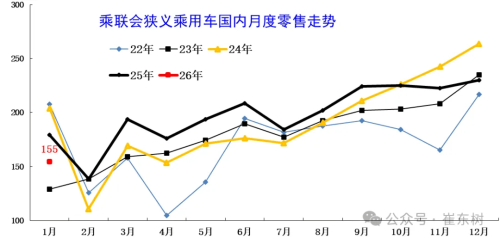

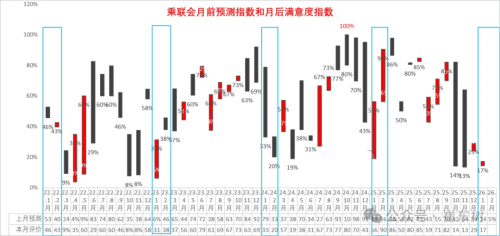

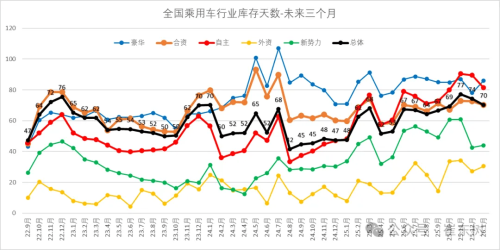

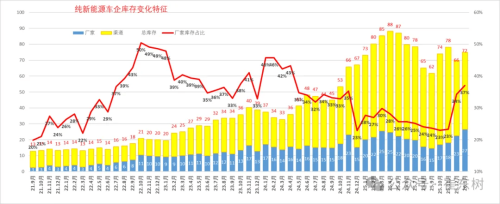

Of the total 3.57 million vehicles in inventory, the manufacturer share stands at a historically high 32%. Secretary-General Cui Dongshu of the China Passenger Car Association (CPCA) Releases Analysis Report on China’s Passenger Car Market Inventory for January 2026. Data shows that at the end of January 2026, the national passenger car industry inventory reached 3.57 million vehicles. Although this represents a decrease of 80,000 vehicles from the previous month, it is a significant increase of 580,000 vehicles compared to January 2025, indicating that inventory pressure is markedly higher than in the same periods of previous years. Looking at the retail market, national passenger car retail sales in January totaled 1.55 million vehicles, a year-on-year decrease of 14% and a month-on-month decrease of 32%. Domestic Passenger Vehicle Monthly Retail Trend Cui Dongshu pointed out that the reasons for the negative growth include the expiration of the vehicle purchase tax exemption policy, the strengthened regulations and reduced subsidies of the new trade-in policy, and, at a deeper level, the fundamental issue of low consumer spending power and willingness. Historical data shows that fluctuations in January retail figures are normal: between 2020 and 2025, January growth rates swung sharply between -38% and +58%. This year’s -14% growth is in the middle range of that historical fluctuation. CPCA Pre-Month Forecast Index & Post-Month Satisfaction Index It is worth noting that the CPCA’s forecasting team’s optimism about the market has been continuously declining since early 2025. In early February 2026, their satisfaction rate with the January market was only 17%, and their optimism for the February market has further dropped to 5%. National Passenger Vehicle Industry Inventory Days In terms of inventory, as of the end of January 2026, the existing inventory supports 70 days of future sales. This is on par with the 65 days in January 2023 and the 70 days in January 2024, but significantly higher than the 48 days in January 2025. The manufacturers’ share of inventory has reached 32%, indicating a high operational level. Inventory Change Characteristics of NEV-Dedicated Manufacturers Regarding the inventory structure, within the total inventory of 3.57 million vehicles, the manufacturers’ share is as high as 32%, a historically high level. This reflects the high production enthusiasm of manufacturers during the earlier period of positive market expectations, while channels’ willingness to stock up has become cautious around the Spring Festival. Specifically, inventory for new energy vehicle (NEV) manufacturers has rebounded from a low of 620,000 vehicles in September 2024 to 720,000 vehicles in January 2026. While this is 160,000 vehicles below the peak, it represents an increase of 60,000 vehicles from the previous month, indicating significant inventory pressure within dealer channels.

![[Gasgoo Express] XPENG responds to breakdown of exclusive Australian distributor partnership; Qingdao drives construction of 57 auto industry projects worth over 100 million yuan](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pbWFnZWNuLmdhc2dvby5j-b20vbW9ibG9nby9OZXdzL1VFZGl0b3Iv-aW1hZ2UvMjAyNTA2MTAvNjM4ODUxNzAw-MTkzODM1OTU2NTQxNDEzNi5qcGc/c06991c2ffe2e05fe81c97062ebd8cf3.jpg?t=20260810&post_id=7167)