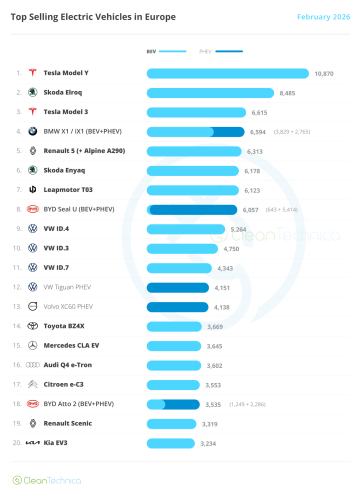

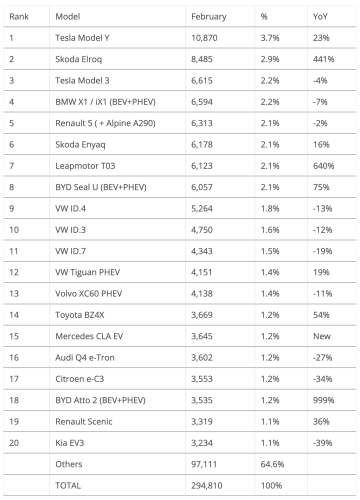

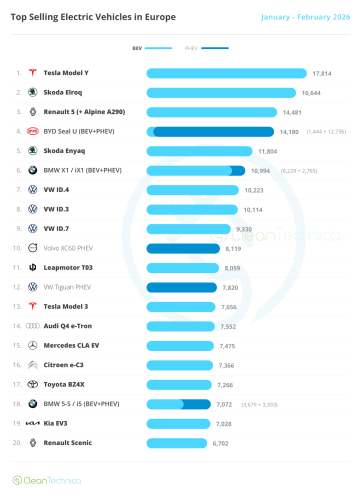

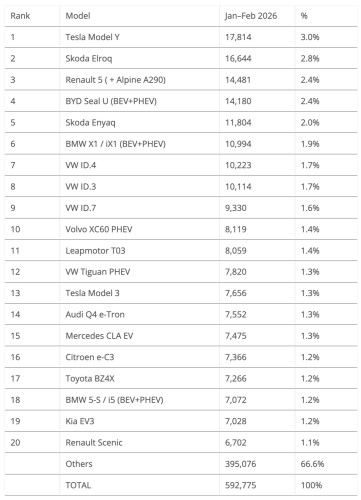

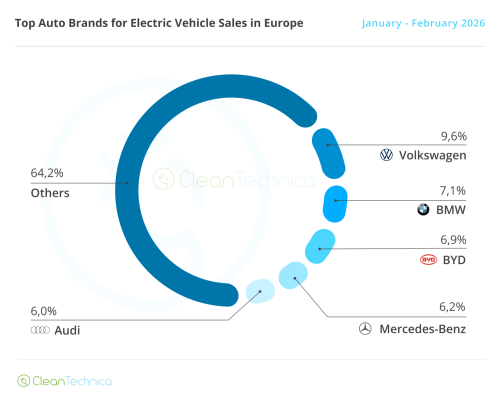

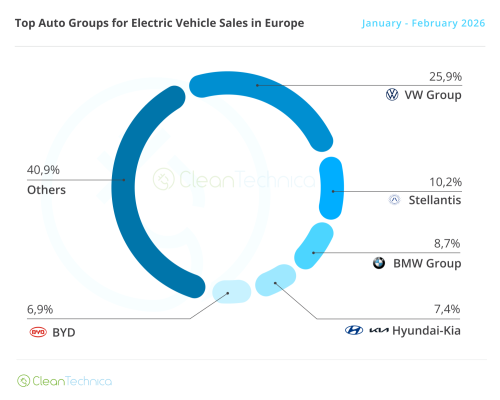

BEVs reach 20% market share! EVs are picking up in Europe, with some 295,000 plugin vehicles being registered in Europe in February, 196,000 of them being BEVs. Overall, plugin vehicles were up 22% YoY. The overall market also had a positive month in February, rising 2% YoY to one million units. Although, the YTD performance is still down 1% YoY. Looking at the February powertrain breakdown, petrol (down 17% YoY, to 23% share) and diesel (down 14% YoY, to 8% share) continued their descent, plugless hybrids still grew above the market average (+10% YoY vs +2%), while plugins continued on the rise — with BEVs up 16% to 20% share and PHEVs surging 33% to 10% share. Adding the 38% market share of HEVs to the 20% of BEVs and the 10% of PHEVs, this means that 68% of all new cars in Europe had some sort of electrification. With these February results, the year-to-date share for BEVs remained at 20% (30% for PHEVs and BEVs combined), mirroring February’s results. Looking at the best selling models, the big news this month was Tesla placing two models on the podium. Here’s a more detailed analysis of the top 5 EVs this month: #1 Tesla Model Y — Tesla’s midsize crossover is back in the driver’s seat, thanks to 10,870 registrations in February. This represented a 23% jump YoY, but the numbers can be deceiving, as twelve months ago the Model Y was going through its facelift. With Model Y prices starting at €40,000, and after six years on the market, the crossover still offers an appealing package. Comparing it with the comparable competition and a similar starting price, we have: the base versions of the Toyota BZ4X and VW ID.4 and the BEV version of the BYD Seal U, and all have less range than the base Model Y (in the case of the Toyota, it’s almost 100 km less range), they charge slower than the Tesla (with only the Toyota coming close — 150 kW, compared to the 175 kW of the Model Y), and all of them have less interior space than Tesla’s star player. Currently, you buy a Tesla with your head, not your heart. (That is why they are so popular with Ubers and such.) #2 Skoda Elroq — The Elroq won another podium presence in February, thanks to 8,485 registrations, which is a 441% increase YoY — in February 2025, the Czech was still starting to ramp up production. Looking ahead, towards the second half of 2026, the problem for the Czech crossover is that around mid-2026, a new, smaller, and more affordable Skoda crossover will land. Called the Epiq, that model should steal lots of sales from the current star player of the Skoda lineup, as it will be simultaneously cheaper and more modern than the Elroq. So, while the first half of 2026 might see the Elroq chase the Model Y, later in the year, we should see it lose pace and see the US crossover gain ground. #3 Tesla Model 3 — Tesla’s previous star player managed to reach the podium after a close race with the #4 BMW iX1/X1 PHEV twins, thanks to 6,615 registrations in February. This still represented a 4% drop in sales, but among the bad news, the silver lining for Tesla’s sedan is the fact that the sales drop is slowing down. So, while podium positions are no longer on the horizon, it looks like a top 10 (top 5?) spot is doable this year, which is no mean feat for a nine-year-old model wearing a body type (sedan) not popular in Europe. #4 BMW iX1/X1 PHEV — The German twins are in cruise control, winning a top 5 position in February thanks to 6,594 registrations. Benefitting from favorable lease rates to help things along, the BMW crossovers saw their sales drop by 7% in February. Still, help is on the way, with a deep refresh coming this year, promising to transform them into baby Neue Klasse. Expect the iX1 in particular to upgrade its specs, making it far more interesting than the current version. #5 Renault 5 (inc. Alpine A290) — Renault’s star player delivered 6,313 sales in February, with the iconic hatchback dropping its sales slightly, by 2%. Looking at its 2026 performance, with production already ramped up and demand now at cruising speed, now is the time for the French twins to show their true value. Will they replicate the success of their Renault Zoe predecessor? No matter how attractive the 5 is, the truth is that in 2026, its space on the market will be squeezed not only by external competition (VW ID.Polo, Cupra Raval, etc.), but also by internal competition, with the equally cute new Twingo stealing sales from below and the appealing 4 crossover doing the same from above. And let’s not forget the Nissan Micra, which is basically a Renault 5 in a Kenzo suit…. Outside the top 5, the biggest highlights come from Asia, with two new Chinese EVs on the table and Toyota’s BZ4X benefitting from the recent refresh, jumping 54% in sales and landing in 14th with 3,669 units. Is Toyota finally playing ball in the EV space? But more surprising was the Leapmotor T03, which surged into 7th thanks to 6,123 units, a new record for the small EV. Much thanks is due to the shocking result in Italy, with the Chinese EV collecting 4,778 units in that market alone, allowing it to be 4th overall, ahead of best sellers like the Citroen C3, Toyota Yaris, and Renault Clio. It even outsold the Fiat 500 & 600 … together! In ITALY!!!! So, when Stellantis says that EVs are not ready for prime time … this kind of result says something different. It’s Stellantis EVs that are not ready for prime time. I mean, city cars is Fiat’s strong point, and even that is being taken away by a Chinese company in its domestic market. Sooner or later, the multinational OEM will need to take painful measures, and the longer it takes making them, the more painful these measures will be. Finally, the PHEV version of the BYD Atto 2 (BYD Yuan Up in euro-spec) landed with a bang, with over 2,000 deliveries right in in its debut month. Added to the BEV units, that allowed it to break its sales record and join the top 20. With it, BYD is exploring a segment that currently is basically up for grabs (PHEV small crossovers) due to the lack of competitors. Will it be another success story for the Shenzhen make? Outside the top 20, the highlight goes to the fact that the BYD Dolphin Surf (euro-spec Seagull) ended the month at #21, just 13 units from the #20 Kia EV3. If BYD’s smallest EV had joined the table, it would mean that BYD would have placed three representatives in the top 20, something that only Volkswagen managed to do. Yep, Volkswagen’s biggest nightmare in Europe from now on isn’t Tesla, but BYD. Looking at the 2026 ranking, there were significant changes in the top positions. The Tesla Model Y returned to the top of the table, and shouldn’t leave it soon. VW’s ID.4 surpassed its stablemates and climbed to 7th, but it was the second half of the table that witnessed the most surprising turnarounds: The Leapmotor T03 and the Tesla Model 3 joined the table, at #11 and #13, respectively; VW’s Tiguan PHEV jumped five positions, into 12th, allowing the German make to have four representatives in the top 12; Toyota saw its BZ4X climb one spot, to #17, making it the 5th D-segment BEV on the table and highlighting a few things: Tesla’s black-hole effect isn’t as effective as in the past, company cars continue to have an outsized importance on BEV sales, and finally, BEVs are winning over company car fleets, with PHEVs losing share in that particular corner of the market. As for the plugin auto brand ranking, the leader, Volkswagen, remained firm (9.6%), holding a comfortable 2.5% share lead over sliding #2 BMW, which lost 0.2% share in February and is now at 7.1%. (It must be all those clients on the iX3 waiting list….) Third placed BYD saw its share rise by 0.1% in February, from 6.8% to 6.9%, and is now just 0.2% share behind the runner-up BMW, so March might bring BYD climbing into the #2 position! Then the Shenzhen make would only need to focus on going after Volkswagen to take the best seller title … in Europe! Below the podium, Mercedes (6.2%) profited from a drop from rival Audi (6% in February, down from 6.4% in the previous month) to climb one position into 4th. With the three-pointed-star brand having an avalanche of new models set to start this year (GLB, GLC, VLE, VLS, C-Class…), expect this to improve its sales performance significantly. Maybe it won’t be enough to remove BMW from the podium, but it likely will place it above Audi at the end of the year. As for Audi, even keeping the 5th spot would be a tall order, considering the steady rise of #6 Skoda (5.8% in February, up 0.1% compared to January) and the fact that the Czech maker will introduce two brand new BEVs in 2026, the small Epiq and the large Peaq. Both will surely increase the total volume of sales from the brand. Arranging things by automotive group, Volkswagen Group is firmly in the lead, despite losing 0.5% share in February. It is now at 25.9% share, a market share that is comparable to BYD’s in China and Tesla’s in the USA. This is an important metric for the German conglomerate if it wants to stay relevant in a fully electrified global automotive market. If you can’t win at home…. #2 Stellantis and #3 BMW Group were both down 0.2% in February, but both remained comfortable in their podium positions in February. Hyundai–Kia (7.4%) remained in 4th, while #5 BYD (6.9%) is now closer to the Korean OEM. Still, with #6 Geely (6.7%) dangerously close, the Shenzhen OEM will also need to keep a close eye on the rearview mirror, as its arch rival has the potential to surpass it a few months from now.

![Gasgoo, Xpeng, [Gasgoo News] XPENG GX officially announced; China's NEV insurance premiums up 34.8% YoY in 2025](https://cdn.topcarnews.net/media/id/aHR0cHM6Ly9pbWFnZWNuLmdhc2dvby5j-b20vbW9ibG9nby9OZXdzL1VFZGl0b3Iv-aW1hZ2UvMjAyNTA2MTAvNjM4ODUxNzAw-MTkzODM1OTU2NTQxNDEzNi5qcGc/c06991c2ffe2e05fe81c97062ebd8cf3.jpg?t=20260808&post_id=12479)