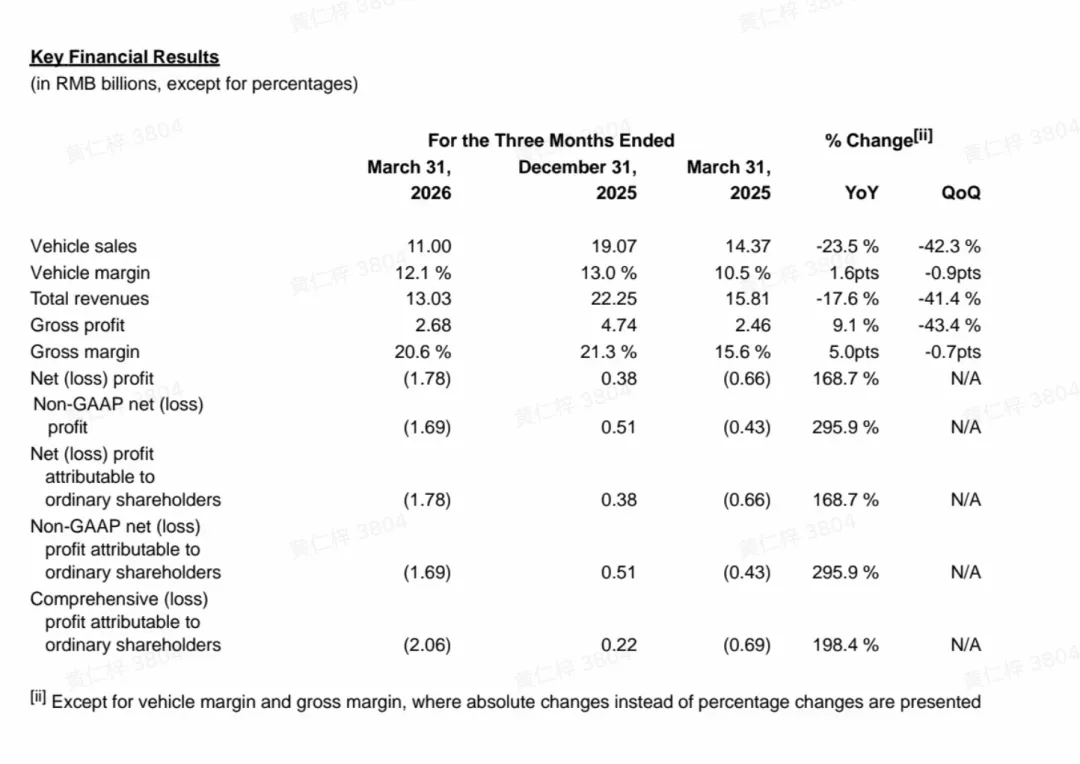

On May 28, Xpeng released its financial results for the first quarter of 2026, and at first glance, the numbers did not look encouraging. The earnings report showed that Xpeng delivered 62,682 vehicles in Q1, down 33.3% year-on-year and 46.1% quarter-on-quarter. Total revenue came in at RMB 13.03 billion ($1.92 billion), down 17.6% year-on-year and 41.4% from the previous quarter. Revenue from vehicle sales reached RMB 11.00 billion ($1.62 billion), down 23.5% year-on-year and 42.3% quarter-on-quarter. Xpeng’s key financila results in Q1 2026 Taken together, those figures make it easy to conclude that Xpeng has once again entered a period of heightened pressure. But that alone does not tell the full story. The first quarter is traditionally a weak season for China’s auto market, and Xpeng also happened to be caught in the middle of a product transition cycle. Older models were losing momentum while new products had yet to fully contribute. In particular, the GX — which was only launched on May 20 — made no contribution to Q1 deliveries. In other words, this quarter looks more like a cyclical trough rather than the start of a long-term decline. Of course, CEO He Xiaopeng himself clearly understands that the weak Q1 delivery performance would trigger doubts about the company. That is why he emphasized three key points during the earnings call: At this stage, Xpeng is prioritizing a balance between sales volume and operational quality, rather than pursuing scale alone — implying that short-term delivery fluctuations are manageable. Over the next six months, Xpeng plans to launch four globally positioned SUV models, and the company is confident it will enter a rapid sales growth phase starting in Q2. Looking ahead, Xpeng expects second-quarter deliveries to rise about 60% quarter-on-quarter, potentially reaching the 100,000-unit mark. The MONA series, currently Xpeng’s sales backbone, will expand overseas in the future — suggesting that the MONA lineup, already validated in China, could become a growth driver across multiple international markets. In short, He Xiaopeng remains highly confident. Xpeng MONA M03 Turning back to the earnings report itself, the most noteworthy metric is actually gross margin. Xpeng’s overall gross margin reached 20.6% in Q1, up 5 percentage points year-on-year and down just 0.7 percentage points quarter-on-quarter. Vehicle gross margin stood at 12.1%, improving 1.6 percentage points year-on-year while slipping 0.9 percentage points sequentially. Despite deliveries nearly halving from the previous quarter, gross margin did not deteriorate significantly, suggesting that Xpeng’s adjustments to cost controls and product mix over the past year are beginning to show up in its financial statements. However, the 20.6% figure should not be interpreted simply as “vehicle gross margin.” In Q1, Xpeng’s services and other revenue reached RMB 2.03 billion ($300 million), up 41.2% year-on-year, with a gross margin of 66.5%. This segment mainly includes technical R&D services, parts and accessories sales, and other businesses that significantly boosted overall margins. Still, Xpeng’s “services and other revenue” segment has long been controversial. The core issue is instability, as such revenue is highly dependent on project timing. For example, the previous quarter benefited from technology service milestone payments and carbon credit revenue, while those contributions declined in Q1, causing services and other revenue to fall 36.1% quarter-on-quarter. Revenue from technology sales to Volkswagen Group is another source of uncertainty. If Volkswagen were to stop purchasing technology from Xpeng, the company could lose revenue worth hundreds of millions or even billions of yuan. While this business can improve profitability, it still cannot be treated as a stable core revenue stream. The loss side of the earnings report is much more straightforward. Xpeng posted a net loss of RMB 1.78 billion ($260 million) in Q1, compared with a net loss of RMB 660 million ($100 million) a year earlier, meaning losses widened by RMB 1.12 billion ($165 million) year-on-year. In Q4 2025, Xpeng had actually posted a net profit of RMB 380 million ($56 million), implying a sequential swing of RMB 2.16 billion ($320 million). The picture looks similar under the non-GAAP metric. Q1 non-GAAP net loss reached RMB 1.69 billion ($250 million), versus a loss of RMB 430 million ($63 million) in the same period last year, while Q4 2025 had delivered a non-GAAP net profit of RMB 510 million ($75 million). In other words, this was not simply another “loss-making quarter.” It marked Xpeng’s return to losses immediately after briefly achieving profitability in Q4. The renewed expansion in losses reflects two dynamics: weaker deliveries reduced gross profit scale, while R&D spending continued to rise. Xpeng’s R&D expenses reached RMB 2.91 billion ($430 million) in Q1, up 46.8% year-on-year and 1.1% quarter-on-quarter. During the earnings call, He Xiaopeng repeatedly referenced Robotaxi, humanoid robots, and physical AI. Xpeng’s nest-gen humanoid robot IRON These initiatives may support a more ambitious long-term narrative, but in the short term, they remain major cost centers. Xpeng still needs to prove that such investments can eventually translate into meaningful revenue rather than remaining concepts showcased at launch events. According to He Xiaopeng, the second half of the year will see further moves in these emerging businesses, including preparations for mass production of humanoid robots and pilot Robotaxi operations. However, globally speaking, these sectors remain more “vision” than mature business models, and Xpeng itself is still an early explorer. Betting on new businesses does not eliminate uncertainty. Taking both the financial fundamentals and He Xiaopeng’s comments into account, the most appropriate way to read this earnings report is not that “Xpeng has suddenly deteriorated,” but rather that “the company is shifting gears.” Going forward, the weight of the “car business” in interpreting Xpeng’s story may gradually decline. As repeatedly highlighted during the earnings call, humanoid robots, VLA 2.0, Robotaxi initiatives, and overseas expansion will increasingly become key indicators by which the market assesses Xpeng’s value. In the near term, however, the market’s focus is straightforward: after the GX launch, can Xpeng successfully bridge into its next product cycle? He Xiaopeng stressed that the GX is an extremely important product. It is expected to deliver higher gross margins and higher ASPs (average selling prices) for the company, while also serving as a core testing platform for L4 autonomous driving and Robotaxi technologies. In that sense, the GX represents not only Xpeng’s present, but also its future. As for that future itself, vehicles will still remain part of the story — but the narrative is becoming far more diversified. That includes overseas market expansion, with management forecasting overseas deliveries could double this year and international markets contributing significantly more revenue and profit over the next five years, as well as commercialization opportunities in Robotaxi, which He Xiaopeng believes may only meaningfully emerge after 2028. During the earnings call, He Xiaopeng also specifically addressed the company’s rebranding — changing its name from “Xpeng Motors” to “Xpeng Group” — describing it as the real beginning of Xpeng’s commitment to physical AI. Ultimately, this somewhat “bittersweet” Q1 earnings report may end up playing a pivotal role in Xpeng’s corporate history. Whether it marks the start of decline or the turning point of a transformation will only become clear over a longer time horizon.