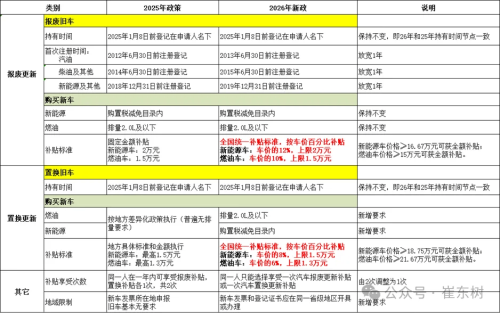

In 2026, China’s auto market shifts from price competition to value-driven rivalry. As the adjustment of the preferential new energy vehicle purchase tax policy officially takes effect in 2026, combined with the guidance of policies like the “trade-in” program for consumption upgrades, the direction of competition in China’s auto market is shifting. Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA), analyzed that the proportional subsidies for replacement and renewal in 2026 encourage consumers to purchase more premium vehicles. Most consumers need to buy a model priced around 200,000 RMB to receive the full subsidy, leading them to further upgrade their choices, thereby driving consumption upgrades and an increase in purchase prices. This assertion is already reflected by clear signals in the market. Data from the CPCA shows that from January to December 2025, the number of models with price reductions in the industry was 177, a decrease of 42 compared to 2024. This number is expected to further decrease in 2026, indicating a contraction in market strategies that rely solely on price stimulation. Meanwhile, consumer surveys show that over 30% of consumers have set their budget for their next car above 300,000 RMB. These two sets of data point to a common trend: the market is becoming desensitized to mere “price cuts” but increasingly sensitive to “real value.” In Cui Dongshu’s view, the core characteristic of the 2026 auto market can be simply summarized as: the diminishing effectiveness of the “price war” and the rise of the “value war” as the main channel. The key to competition for automakers will be who can provide more upscale configurations and experiences. Policy Comparison: 2025 vs. 2026 Entering 2025, despite fluctuations in the average price during the year, the single-month average price in December rebounded to 184,000 RMB, showing the stability of the consumption base. The recently released “Deloitte Global Automotive Consumer Study” indicates that over 63% of consumers are targeting their next car budget at 300,000 RMB or above. Looking at market data and the performance of specific models, the decline in sales and popularity of some traditional luxury brands and new energy vehicle (NEV) startups is not due to a decrease in market demand for “premium” features itself, but rather because consumers are no longer willing to pay for invisible “brand premiums.” AITO M7 This is reflected in the data: in 2024, models in the 200,000-300,000 RMB price range held an 18% share in the domestic retail market, which increased to 19% by 2025. In terms of models, vehicles like the Xiaomi SU7/YU7 and the AITO M7, which have different positioning but both emphasize high value perception, have received positive market feedback. Furthermore, referring to the sales structure data from December 2025, the distribution of powertrain types is relatively uneven across different market price segments. Among these, pure electric vehicles perform strongest in the sub-50,000 RMB market, while range-extended electric vehicles show their strongest distribution in the premium market. Hybrid vehicles hold a slightly higher share in the 200,000-400,000 RMB segment and perform relatively strongly in the 100,000-200,000 RMB market. Benz CLA As market trends change, traditional luxury brands are also quickly adjusting their configuration strategies, focusing more on the genuine needs of users. For example, Mercedes-Benz has made features like seat heating and ventilation standard on some models; Audi and Volkswagen have added new intelligent features to already-sold vehicles via OTA updates, both receiving positive market feedback. GAC Toyota bZ7 Other joint-venture brands are no exception. In the core 200,000-RMB upgrade market, while actively offering advanced configurations like high-end intelligent driving and digital cockpits, they also emphasize overall vehicle tuning and quality control. For instance, the upcoming GAC Toyota bZ7 is equipped with Momenta R6 advanced driving assistance and dual-chamber air suspension. On the side of NEV startups, there is also a shift towards focusing on the development of core features for high-frequency use, optimizing space and riding experience, and beginning to build more extensive service networks.