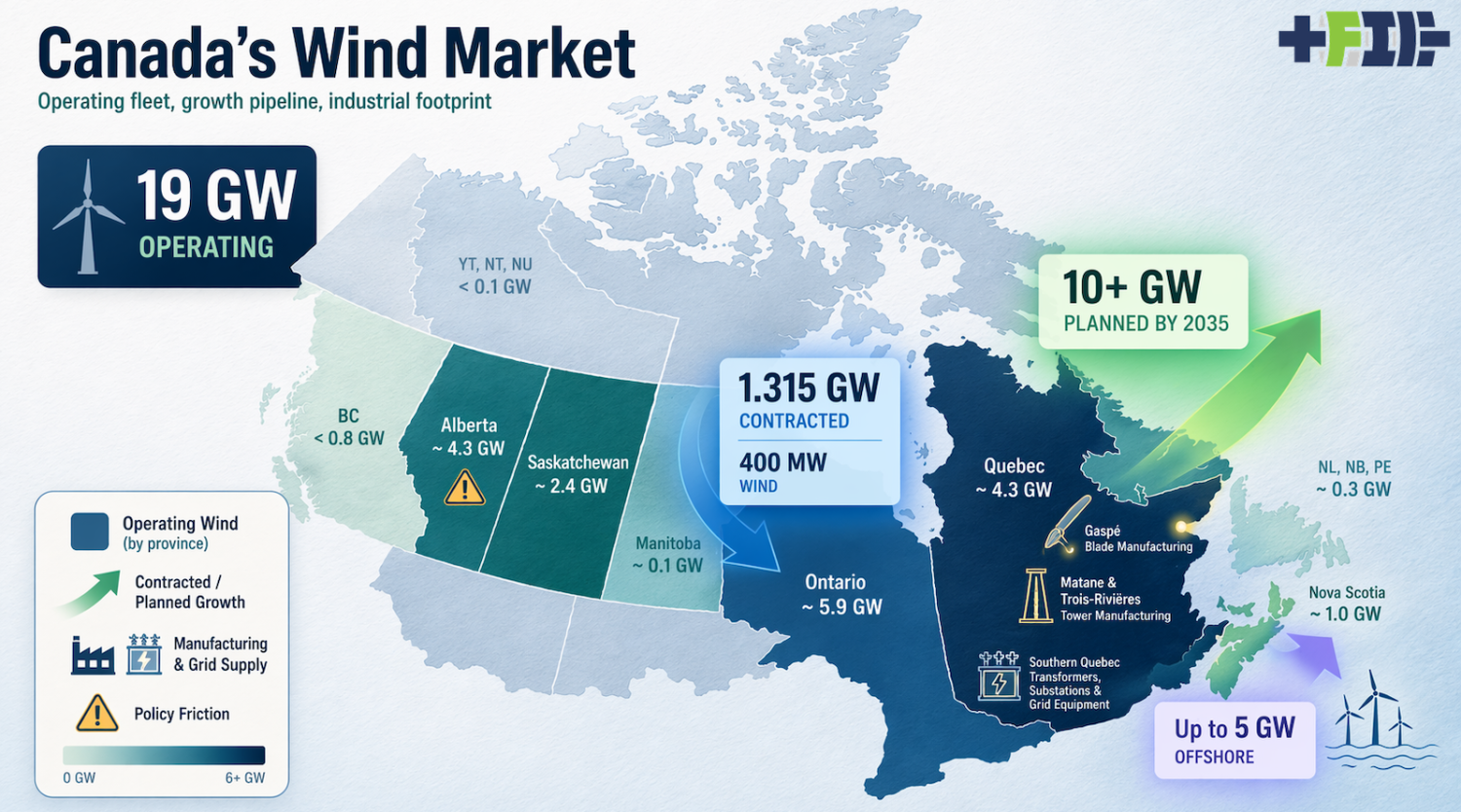

Ontario’s return to renewable procurement is the clearest sign that one of Canada’s largest electricity markets has accepted a reality it spent years resisting. The timing is propitious as I prepare to provide an update to a global audience on North American wind energy through the World Wind Energy Association. Electricity demand is rising as transport, buildings, and industry electrify. Refusing wind and solar in that environment was never a long-term strategy. It was a pause wrapped in politics. The Independent Electricity System Operator’s Long-Term 2 Energy Supply procurement has now broken that pause. On April 9, 2026, the IESO published its final results table for Window 1, with 14 selected projects totaling 1,315 MW of new renewable capacity. Of that, 400 MW is wind, split between two 200 MW projects, Gichigami Wind and Northern Breeze Wind. Annual expected production from the two wind projects alone is roughly 1.25 TWh. In a province where annual electricity demand is about 140 TWh, that is not transformational by itself, but it is real capacity, real energy, and a real market signal after years of drift. According to the IESO and the Canadian Renewable Energy Association, every project in the round also includes at least 50% Indigenous equity participation, which makes this not just a procurement return but a more mature version of one. That return matters because Canada was not starting from zero. According to CanREA’s 2025 annual data release and its By the Numbers summary, Canada ended 2025 with approximately 25 GW of installed wind, solar, and storage capacity, including nearly 19 GW of wind. That puts the country in the top 10 globally for installed wind capacity. Yet the growth rate has not matched the resource base or the country’s decarbonization needs. Only 347 MW of new wind came online in 2025, from three projects in Quebec, Alberta, and New Brunswick. A national fleet of roughly 19 GW that adds only 347 MW in a year is growing at less than 2%. For a country that needs much more electricity in the 2030s than it consumes today, that is a weak build rate. The installed base says Canada already knows how to build wind. The annual addition says it has not been choosing to build enough of it. That gap between capability and action is the core story of Canadian wind. The return also matters because the Ontario Conservatives rode to a majority in 2018 based in large part through populist and inaccurate attacks on wind and solar. One of their first actions upon taking power was to rip up 758 contracts for renewably generated electricity, including one for an almost completed wind farm in Prince Edward County. The same leader and the same party eight years later are finally connecting with the reality of renewably generated electricity. In a country where partisan conservative politics is often dubious of the seriousness of climate change and the large part renewables will play in addressing it, the most powerful Conservative politician in the country endorsing renewables is a strong signal. The geography of the installed base matters because Canada is not one wind market. It is several provincial markets with different histories, rules, and grid structures. Using CanREA’s January 2026 project list, the rough regional split is easy to see. The Prairie provinces of Alberta, Saskatchewan, and Manitoba account for about 6.8 GW of operating wind, or about 36% of the national total. Ontario has about 5.9 GW, close to 31%. Quebec has about 4.3 GW, roughly 23%. Atlantic Canada has about 1.3 GW, close to 7%. British Columbia and the North together are under 0.8 GW, about 4%. In other words, just three zones, the Prairies, Ontario, and Quebec, account for about 17 GW out of Canada’s 19 GW. That concentration is not surprising. Wind development follows resource quality, transmission, procurement, and local politics. But it does mean that when Ontario re-enters the market and Quebec accelerates, Canada’s national trajectory changes quickly. There is no need for all ten provinces to move at once for the country’s wind outlook to improve. Ontario’s importance goes beyond the 400 MW of wind in the latest round. It matters because Ontario was once central to Canada’s renewable energy momentum and then became the most visible example of contract instability and policy retreat. That damaged investment confidence well beyond the province. When a market of Ontario’s size signals that renewables are again part of the long-term plan, the effect is larger than the first auction total. The LT2 Window 1 portfolio of 1,315 MW is expected to produce more than 3 TWh per year in total. If Ontario needs even 20 TWh to 30 TWh of incremental clean electricity over the next decade, which is a plausible range once electrification and data center growth are included, then this round covers only about 10% to 15% of that rough need. That is exactly why the procurement matters. It is not the solution. It is the reopening of the channel through which solutions can actually flow. Ontario has moved from pretending wind was optional to contracting it again because system math has forced the issue. According to the IESO, more LT2 procurement windows are still ahead. If Ontario is the clearest sign that Canada is moving again, Quebec is the clearest sign of where scale may come from. Hydro-Québec’s Action Plan 2035 is explicit. The province plans to add more than 10,000 MW of new wind by 2035, backed by over $30 billion in public and private investment and major transmission expansion. In practical terms, that means Quebec intends to more than triple its current wind base over about a decade. If the province starts from around 4.3 GW of wind and adds another 10 GW, it ends up above 14 GW. That would make Quebec by itself comparable to a major European wind market. The logic is sound. Hydropower gives Quebec a huge dispatchable balancing asset, so wind does not have to carry firming on its own. Hydro can absorb variability, preserve reservoirs when wind is strong, and generate when wind is weak. In many jurisdictions, integrating large amounts of wind means a parallel fight over batteries, gas peakers, or interconnection. In Quebec, a lot of the balancing plant is already there in the form of dams and reservoirs. That makes Quebec one of the structurally advantaged places in the world to scale wind. Quebec’s story changes the way the rest of Canada should think about wind. For years, hydro-rich provinces were often discussed as though they had less need for variable renewables because they already had low-carbon electricity. That framing missed the next phase of electrification. A hydro system that served legacy loads comfortably may not have enough spare energy for electric vehicles, heat pumps, industrial conversion, and export opportunities all at once. Hydro-Québec’s own plan is an admission that even one of the world’s great hydro systems needs a large new buildout of wind and other resources. The numbers make that plain. Hydro-Québec says it needs 60 TWh of additional clean generation by 2035. If new wind contributes a capacity factor around 35%, then 10 GW of wind would generate about 30.7 TWh per year. That is roughly half the identified need. Wind is not peripheral in that plan. It is central. For the Canadian wind industry, Quebec is no longer an interesting regional market. It is one of the country’s core growth engines. Atlantic Canada is still small in operating wind capacity, but it is gaining strategic weight. Part of that is the old onshore story, where Nova Scotia, New Brunswick, and Prince Edward Island have built useful if modest wind fleets. Part of it is the new offshore story, where Nova Scotia plans to offer licences for up to 5 GW of offshore wind in its first call for bids in 2026 and up to another 10 GW in later rounds. Part of it is also a broader change in Canadian energy geography. For a long time, Atlantic electricity strategy was often discussed in north-south terms, with exports to New England and the United States as the default logic. What is becoming more interesting now is the east-west and domestic picture. More interprovincial electricity movement, more discussion of energy security inside Canada, and more serious thinking about Atlantic resources serving Canadian rather than only foreign demand all improve the long-term case for wind in the region. Even if only a portion of the offshore ambition materializes, 5 GW is not a boutique target. At a 45% offshore capacity factor, 5 GW would produce about 19.7 TWh per year. That is a meaningful block of electricity in a region whose combined provincial loads are not especially large. That does not mean Atlantic Canada is already a major wind center. It means the region is moving from peripheral to strategic. The difference matters. Small markets can remain small for decades if they lack transmission, stable procurement, and an anchor purpose for new generation. Atlantic Canada is slowly acquiring all three. Nova Scotia’s offshore roadmap provides one anchor. The broader conversation around domestic clean electricity flows provides another. If Canada becomes more serious about east-west transmission and reducing dependence on imported fuels for reliability margins, then the Maritimes become more relevant to the national system. Wind in Atlantic Canada will still face the familiar issues of ports, grid reinforcement, supply chains, and local benefits. But unlike a decade ago, the region is now being discussed in terms that imply growth rather than maintenance. That is a meaningful shift in national context. Alberta sits at the other end of the policy spectrum. It remains one of the country’s strongest wind resource areas and a major part of the installed base. It also remains the clearest example of how politics can convert a natural advantage into development friction. Alberta’s moratorium on renewable approvals in 2023 was the bluntest expression of that. Since then, the province has continued to raise the burden on new projects through land-use restrictions, reclamation requirements, and greater uncertainty around permitting. The Alberta government’s land conservation and reclamation guidelines for renewable energy operations add new expectations around security and end-of-life obligations. There is nothing wrong with requiring real reclamation planning. Fossil fuel industries should have faced tougher and earlier cleanup rules themselves. The problem is selective friction. Alberta is imposing tighter scrutiny on renewables in a province that has long tolerated much larger and more durable land and emissions liabilities elsewhere in the energy system. The signal to investors is not that Alberta is careful. It is that Alberta is unpredictable. And yet Alberta remains important, because the resource does not disappear when the policy becomes hostile. The Canada Energy Regulator’s provincial renewables snapshot still identifies large projects in the pipeline, including the 300 MW Bull Trail Wind Project planned by 2029. That is the contradiction at the center of Alberta’s wind sector. The province has the wind regime, the land, and an electricity market structure that should have made it one of Canada’s strongest ongoing clean power growth regions. Instead it has become a case study in how to slow a market that was working. A 300 MW wind farm with a 35% capacity factor produces about 0.92 TWh per year. Ten such projects would produce around 9.2 TWh annually, enough to materially change Alberta’s generation mix. The province’s problem has never been physics. It has been political willingness to accept the answer that physics keeps giving. The Prairie provinces beyond Alberta still matter because they are the working core of Canadian wind. Saskatchewan has expanded from a small base and has more room to grow if procurement continues. Manitoba has less wind than its resource quality might imply, in part because hydro has occupied the low-carbon narrative space there much as it did in Quebec. Across the Prairies, the case for wind is strengthened by industrial load, mining potential, agricultural demand for distributed and community generation, and the large, open geographies that make multi-hundred-megawatt projects possible. If the Prairie region’s roughly 6.8 GW of operating wind grows by only 3% per year, that adds about 200 MW annually. If it grows by 8% per year, closer to what a country in buildout mode might target, that becomes more than 540 MW annually. Over ten years, the difference compounds into several gigawatts. In other words, Canada’s national wind future does not depend on whether one marquee province announces a single big project. It depends on whether the Prairie engine keeps turning and whether Ontario and Quebec stop working against it. British Columbia and the North remain small in operating wind, but they should not be ignored. British Columbia has leaned on hydro for decades, which limited urgency around wind procurement much as in Quebec, but BC Hydro’s recent calls for power and the province’s growing electrification agenda suggest that wind will have a larger place than it has had historically. CanREA’s market outlook argues that British Columbia’s combined wind and solar base could rise materially over the next decade. The reason that matters for wind is that hydro-heavy provinces often look self-sufficient until new demand arrives all at once. When that happens, wind becomes attractive because it can be deployed faster than large hydro, faster than new nuclear, and at lower system cost than overbuilding one resource type alone. The current small base in BC is not proof that wind lacks value there. It is proof that previous system conditions delayed the need for it. As those conditions change, the economics change too. One of the healthiest structural changes in Canadian wind is the increasing role of Indigenous ownership and partnership. According to CanREA, there are now 118 Indigenous-owned wind, solar, and storage projects in operation across Canada. That number is across technologies, but the underlying point applies directly to wind. Projects with meaningful Indigenous equity and governance are becoming less exceptional and more normal. Ontario’s LT2 Window 1 round made this visible, with every selected project including at least 50% Indigenous equity participation. This is not only a social licence issue. It is a finance and durability issue. A project with local and Indigenous ownership has a different political footing from one imposed from outside. If a 200 MW wind project has 50% Indigenous equity, then half of the cash flow, tax base, and strategic leverage sits with partners who are tied to place for the full life of the asset. In practice, that can improve approvals, project resilience, and long-term legitimacy. Canada is not alone in learning that lesson, but it is making it more central to the market’s structure. Canada is not a full-spectrum wind turbine manufacturing country in the way Denmark, Germany, Spain, or China are, and a lot of the highest-value turbine content, especially nacelles, drivetrains, generators, and OEM platform integration, still comes from outside Canada, often from the United States or Europe. But it is not accurate to say Canadian wind projects are simply imported either. Canada retains real domestic industrial capacity in some of the bulkiest turbine components and in a meaningful share of the electrical and civil systems around the turbine. In Quebec, Marmen fabricates wind towers, and LM Wind Power’s Gaspé facility remains a significant blade plant. Beyond the turbine itself, Canadian content is often stronger in the ancillary power-management and grid-integration stack than people assume. Wind farms need transformers, collector substations, switchgear, protection and control systems, reactive power compensation, grid automation, transmission interconnection, foundations, roads, cranes, and ongoing field service. Those pieces are not minor. On many projects, the balance-of-plant and grid-connection package can represent a large share of total capital cost even if the turbine package remains the single biggest line item. Canada has domestic capability in major parts of that stack, including large power transformer manufacturing and expansion in Quebec by Hitachi Energy, plus a broader Canadian footprint in grid services, automation, maintenance, and substation work through firms such as Hitachi Energy and GE Vernova. So the clean formulation is that Canada mostly imports the brains and muscle of the turbine platform itself, but it contributes materially in towers, blades, electrical balance of plant, substations, transformers, controls, construction, and long-term operations. Canada is not just buying finished wind farms from abroad. It is assembling them with a mixed supply chain in which the turbine core is often imported, while a meaningful share of the surrounding industrial and grid infrastructure is Canadian. The real constraint on Canadian wind is no longer proving that turbines work in cold weather, on remote grids, or alongside hydro. That work is done. The real constraint is coordination. Procurement continuity matters. Transmission matters. Interprovincial interties matter. A grid can absorb a fair amount of wind if planners know more wind is coming and build around it. It struggles when governments lurch between enthusiasm and retreat. Hydro-Québec’s plan points in one direction, with more than 10 GW of wind and 5,000 km of transmission by 2035. Ontario’s LT2 procurement points in the same direction, though on a smaller scale. Alberta points the other way, increasing friction in a resource-rich market. That split is why Canada can look well positioned in theory while underperforming in annual additions. The country does not have a wind resource problem. It does not have a basic technology problem. It has a planning consistency problem. From an international perspective, that leaves Canada in an interesting but unresolved position. It ranks ninth globally in installed wind capacity, which means it is not a marginal player. It has roughly 19 GW of wind, which means it has real industrial, operational, and policy experience. It has provinces with top-tier wind resources, provinces with hydro systems that can firm wind output, and provinces with growing electricity demand that will force new procurement. But in 2025 it added only 347 MW of new wind. If Canada had instead added 1.5 GW in 2025, still not an aggressive number for a country of its size and resource base, it would have grown its wind fleet by about 8% instead of under 2%. That is the difference between a market in active expansion and a market idling below potential. Ontario’s return matters because it suggests the idling phase may be ending. Quebec’s plan matters because it puts scale behind that change. Atlantic Canada matters because it broadens the map of future growth. Alberta matters because it shows how much policy can still slow things down. Canada’s wind story in 2026 is not that the country has discovered wind. It is that parts of the country have started deciding, again, to keep building it.