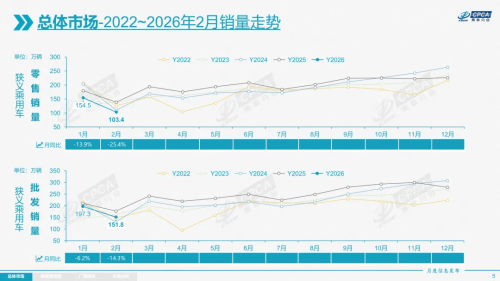

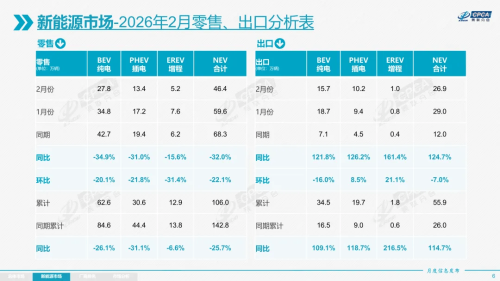

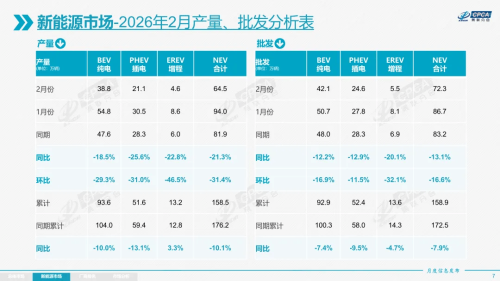

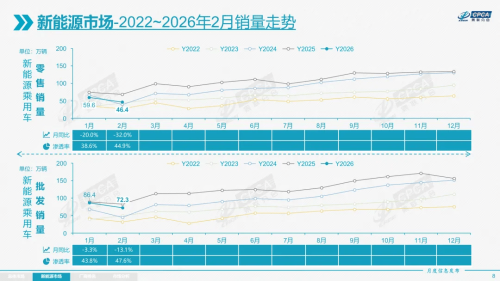

February retail deliveries dropped sharply both YoY and MoM, though export momentum continued. The China Passenger Car Association (CPCA) released its analysis report on the national passenger car market for February 2026. Data shows that due to the combined impact of factors such as the official withdrawal of the new energy vehicle (NEV) purchase tax exemption policy at the end of 2025 and the Spring Festival holiday, the domestic auto market entered a period of deep adjustment in February. The retail sector experienced a significant year-on-year and month-on-month decline, but the export market continued its strong performance, with pronounced structural changes. Overall Market Sales Trend from 2022 to February 2026 Looking at the overall market, national passenger car retail sales in February were 1.034 million units, a year-on-year decrease of 25.4% and a month-on-month decrease of 33.1%. Cumulative retail sales from January to February were 2.578 million units, down 18.9% year-on-year. The report analyzes that the withdrawal of the NEV purchase tax exemption policy at the end of last year led to some consumption demand being pulled forward, which is the main reason for the significant short-term fluctuation in retail at the beginning of the year. Passenger car manufacturer wholesale volume in February was 1.518 million units, down 14.3% year-on-year and 23.0% month-on-month. Production volume was 1.373 million units, down 21.0% year-on-year. Notably, manufacturer wholesale volume in February exceeded production by 150,000 units, while retail volume was 70,000 units lower than domestic wholesale. Overall channel inventory decreased by 220,000 units, which indirectly indicates that automakers are proactively reducing production and destocking to cope with the adjustment in short-term market demand. Analysis of NEV Market Retail and Exports in February In the new energy vehicle sector, the market showed characteristics of a pullback in penetration rate coupled with a continuing trend towards premiumization. Data shows that retail sales of new energy passenger vehicles in February were 464,000 units, a sharp year-on-year decrease of 32.0%. The domestic retail penetration rate for the month was 44.9%, down 4 percentage points from the same period last year. Wholesale volume was 723,000 units, down 13.1% year-on-year, with a wholesale penetration rate of 47.6%. Looking at the specific powertrain structure within February’s NEV wholesale sales, battery electric vehicles (BEVs) decreased by 12.2% year-on-year, plug-in hybrids (PHEVs) decreased by 12.9%, and range-extenders (EREVs) decreased by 20.1% year-on-year. Analysis of NEV Market Production and Wholesale in February Despite the overall decline, structural changes were significant. The proportion of premium NEVs increased, while the share of entry-level consumption decreased. For example, in the BEV market, wholesale sales of B-segment electric vehicles grew by 16% year-on-year, with their share of the BEV segment rising to 35%. In contrast, sales of A00-segment mini electric vehicles plummeted by 61% year-on-year, with their share dropping by 14 percentage points. Sixteen manufacturers exceeded 10,000 units in NEV wholesale sales in February. Among them, BYD (187,782 units), Geely Auto (117,488 units), and Tesla China (58,599 units) ranked in the top three. Enterprise brands surpassing 20,000 units in domestic NEV retail included BYD, Geely, Tesla China, Changan Automobile, Harmony Intelligent Mobility Alliance (HIMA), Li Auto, NIO, and Xiaomi Auto. NEV Market Sales Trend from 2022 to February 2026 Regarding exports, passenger vehicle exports in February reached 555,000 units, a year-on-year increase of 56.0%, with average daily exports hitting a new record high for the period. New energy passenger vehicle exports in February totaled 269,000 units, a surge of 124.7% year-on-year, accounting for 48.5% of total passenger vehicle exports. Among these, NEV exports from domestic brands increased by 110% year-on-year, achieving high growth in regions such as Europe and Southeast Asia. BYD led with 98,706 units, followed by Geely Auto (40,852 units), Chery Auto (28,304 units), Tesla China (20,393 units), and SAIC Passenger Vehicle (14,138 units). February Manufacturer Rankings The report specifically noted that the proportion of CKD (Completely Knocked Down) exports for some domestic brands is relatively high. For instance, CKD exports accounted for 52% of Great Wall Motor’s total exports. Combined with the scale of fuel vehicles produced overseas, it is projected that total overseas sales of Chinese automobiles will exceed 9 million units.