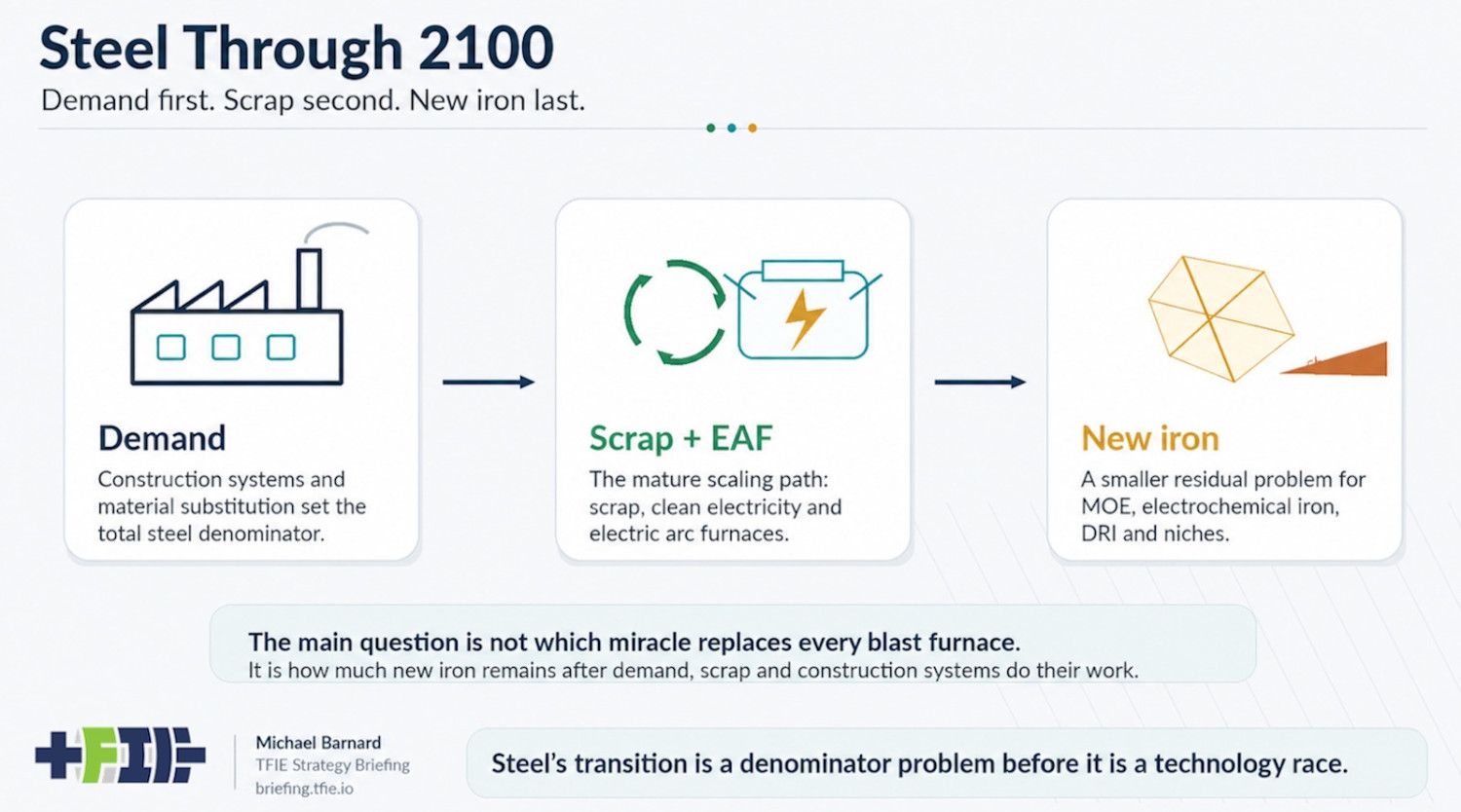

Steel keeps getting framed as a hydrogen problem because hydrogen gives the sector a single shiny lever. Replace coal with hydrogen, keep making new iron, plug it into an electric arc furnace, and declare victory somewhere around the ribbon-cutting ceremony. It is an attractive story for governments, incumbent producers, electrolyzer vendors, consultants, and anyone else who prefers a technology race to a material-flow problem. The trouble is that steel’s transition does not start with hydrogen. It starts with how much steel the world actually needs, how much old steel comes back as scrap, how quickly electric arc furnaces expand, how construction changes, and how much new iron remains after those factors are counted. Hydrogen may have a role in that residual new-iron problem, but treating it as the center of the steel transition gets the order wrong. The scale is not in doubt. The world makes roughly 1.9 billion tons of crude steel a year, much of it still through blast furnaces and basic oxygen furnaces using iron ore, coal, limestone, and some scrap. Steel is in buildings, bridges, vehicles, ships, rails, wind turbines, transformers, ports, warehouses, appliances, factories, and the industrial equipment that makes the rest of the economy possible. It is a serious climate problem, but serious does not mean mysterious. That is the frame of my full TFIE Strategy Briefing transition pathway review, Steel’s 2100 Transition Starts With The Denominator, Not Hydrogen. The paid Briefing version follows the denominator through the century, including demand, scrap, electric arc furnaces, new iron, regional strategy, scorecards, evidence triggers, and the update points that would change the verdict. The public version is simpler: stop asking which hero technology replaces every blast furnace before asking how large the blast-furnace replacement problem actually remains. I have been working through this for several years. In 2023, I wrote that steel is a major climate problem with proven tools and then built a projection showing that steel’s outsized carbon emissions could shrink rapidly as the production mix changed. That earlier work already pointed to electric arc furnaces, scrap, clean electricity, and declining blast furnace use as the central path, but it still gave more room to future demand growth than I now think is warranted. China changed the denominator. Its construction surge from roughly 2000 to 2020 was one of the largest material-demand events in human history, and assuming that the rest of the world will repeat it is a bad starting point. India, Southeast Asia, Africa, and other growth regions will build a great deal, but they are unlikely to reproduce China’s exact mix of steel intensity, cement intensity, urbanization speed, property expansion, infrastructure buildout, and industrial policy. Construction systems matter as well. Steel and cement are coupled through buildings and infrastructure, so lower concrete intensity changes steel demand too. My reassessment of falling cement use and future steel projections pulled cement, mass timber, scrap, and construction practice into the steel pathway. Later work on cross-laminated timber displacement reinforced the same point. Mass timber does not make steel disappear, but it does make some steel demand less inevitable. Scrap is the bigger structural correction. Steel is not a fuel that disappears after use. It is a long-lived material stock that eventually returns from vehicles, buildings, machinery, infrastructure, appliances, pipelines, and industrial systems. The timing is uneven, the quality issues are real, and some products need cleaner metallic inputs than mixed scrap can provide. Still, a lot of future steel demand will be met by steel the world has already made. That makes electric arc furnaces central, not speculative. They are already an industrial steelmaking route, not a lab curiosity, and they dominate production in some markets. They can melt scrap, direct reduced iron, pig iron, or other metallic inputs using electricity, and as grids decarbonize, their emissions fall with them. There are constraints: copper contamination, product mix, regional scrap availability, electricity prices, logistics, and customer qualification all matter. But the route is mature, commercial, and scalable in a way many new-iron technologies are not yet. This is where a lot of green-steel narratives start to wobble. A pilot is not a market. A grant is not a transition. A hydrogen direct reduced iron announcement is not a durable steelmaking strategy. A carbon capture retrofit on a blast furnace is not automatically decarbonization. Real progress is visible in blast furnace retirements, electric arc furnace capacity running at high utilization, better scrap collection and sorting, clean electricity being used for actual production, and buyers specifying lower-carbon steel because the material has to meet real procurement requirements. Hydrogen direct reduced iron works technically. Iron ore can be reduced with hydrogen instead of carbon monoxide from coal or fossil gas, and the resulting iron can be melted in an electric arc furnace. With clean hydrogen and clean electricity, emissions can be low. That part is straightforward industrial chemistry. The hard part is the comparator. Hydrogen DRI is not competing only with an unabated blast furnace. That is the easy comparison and, unsurprisingly, hydrogen does better. The real comparison is lower steel demand, more scrap, electric arc furnaces, clean electricity, better scrap processing, material substitution, regional green iron trade, and possibly direct electrochemical iron routes. Hydrogen also has to carry its own fuel chain: production, conditioning, storage, transport, delivery, reliability, and cost before a steel plant ever sees a molecule. That is why my later conclusion was that hydrogen will not win the zero-carbon steel race. Not because hydrogen cannot reduce iron. It can. The problem is that once demand is moderated and scrap rises, hydrogen DRI becomes one candidate for a smaller residual new-iron problem, not the center of the steel transition. Australia is a useful example of the distinction. The country has iron ore, ports, industrial capability, and excellent renewable resources, so moving up the value chain toward green iron or hot briquetted iron is physically coherent. Exporting hydrogen as a national destiny is much less so. Turning ore into higher-value metallic inputs near clean power is at least aligned with the material system. Shipping molecules around the world in the hope that they become the universal answer is mostly a rerun of hydrogen-export wishful thinking. The policy and investment test should be simple. Support what changes production: embodied-carbon standards, public procurement, clean electricity, grid capacity, scrap quality, industrial permitting, and retirement of high-emitting assets. Then ask every green-steel project what it actually beats, what steel-demand denominator it assumes, what happens if scrap rises faster, and what happens if the promised hydrogen never arrives at the promised price. Steel is not easy, but it is less mysterious than many heavy-industry narratives imply. The world already has a mature circular route in scrap and electric arc furnaces, clean electricity keeps expanding, construction systems can reduce material intensity in some segments, and the existing stock of steel will return over time. It also has a large legacy blast furnace fleet, a lot of coal, a lot of incumbency, and many strategies that confuse announced activity with changed production. If the world assumes endless growth in primary steel demand, every low-carbon pathway has to replace an enormous blast furnace system ton for ton. If demand moderates, scrap rises, electric arc furnaces expand, and construction intensity falls, the new-iron problem becomes smaller, sharper, and more regional. Hydrogen may earn a place in that narrower problem, but it has to earn it against the real alternatives, not against a convenient cartoon of coal steel forever. The full transition pathway review is available at TFIE Strategy Briefing: Steel’s 2100 Transition Starts With The Denominator, Not Hydrogen. It goes deeper on demand, scrap, electric arc furnaces, construction systems, regional strategy, new-iron routes, update triggers, and the evidence that would change the verdict. For more reality-based analysis of industrial decarbonization, hydrogen claims, material demand, infrastructure strategy, and climate-tech denominators, subscribe to TFIE Strategy Briefing.