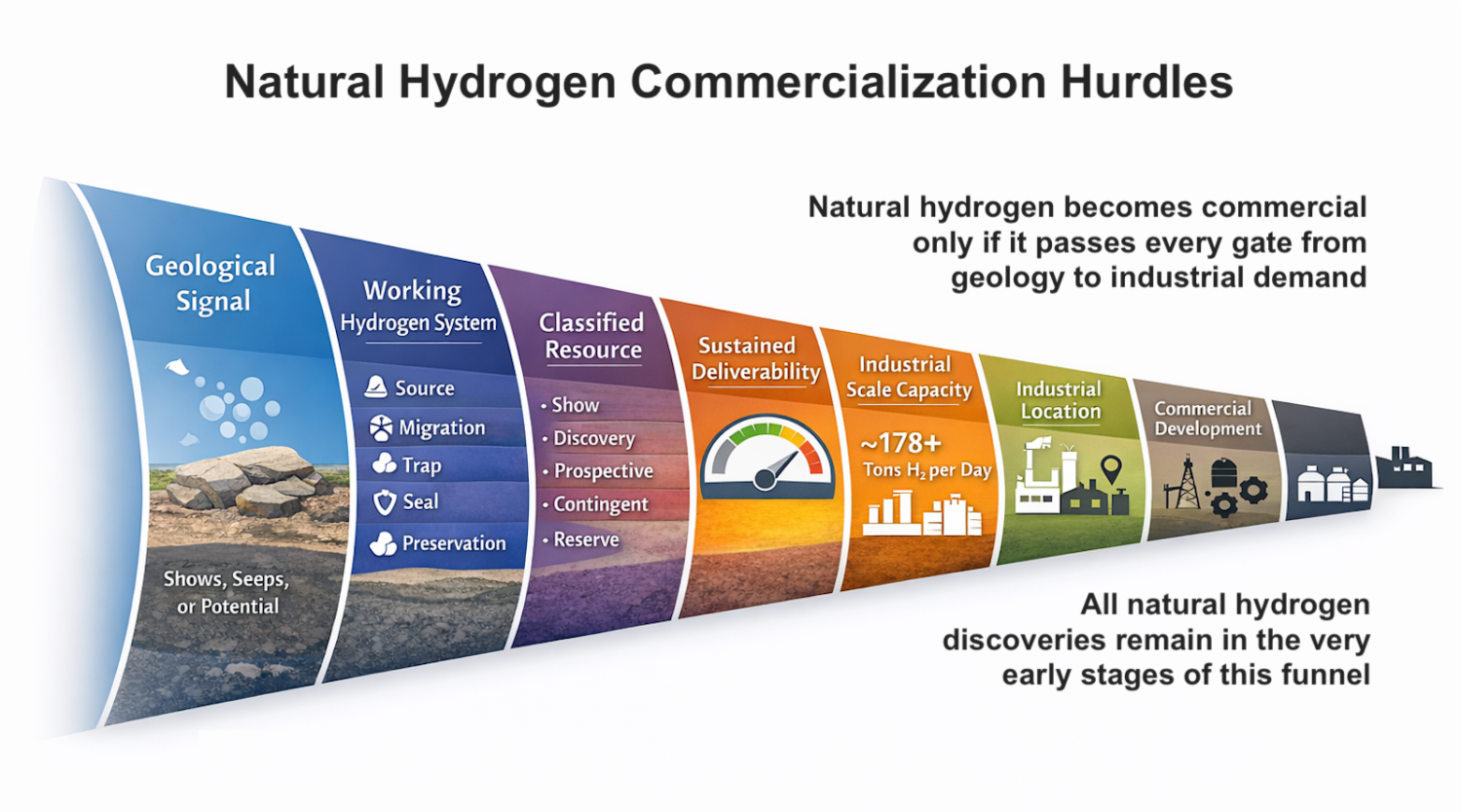

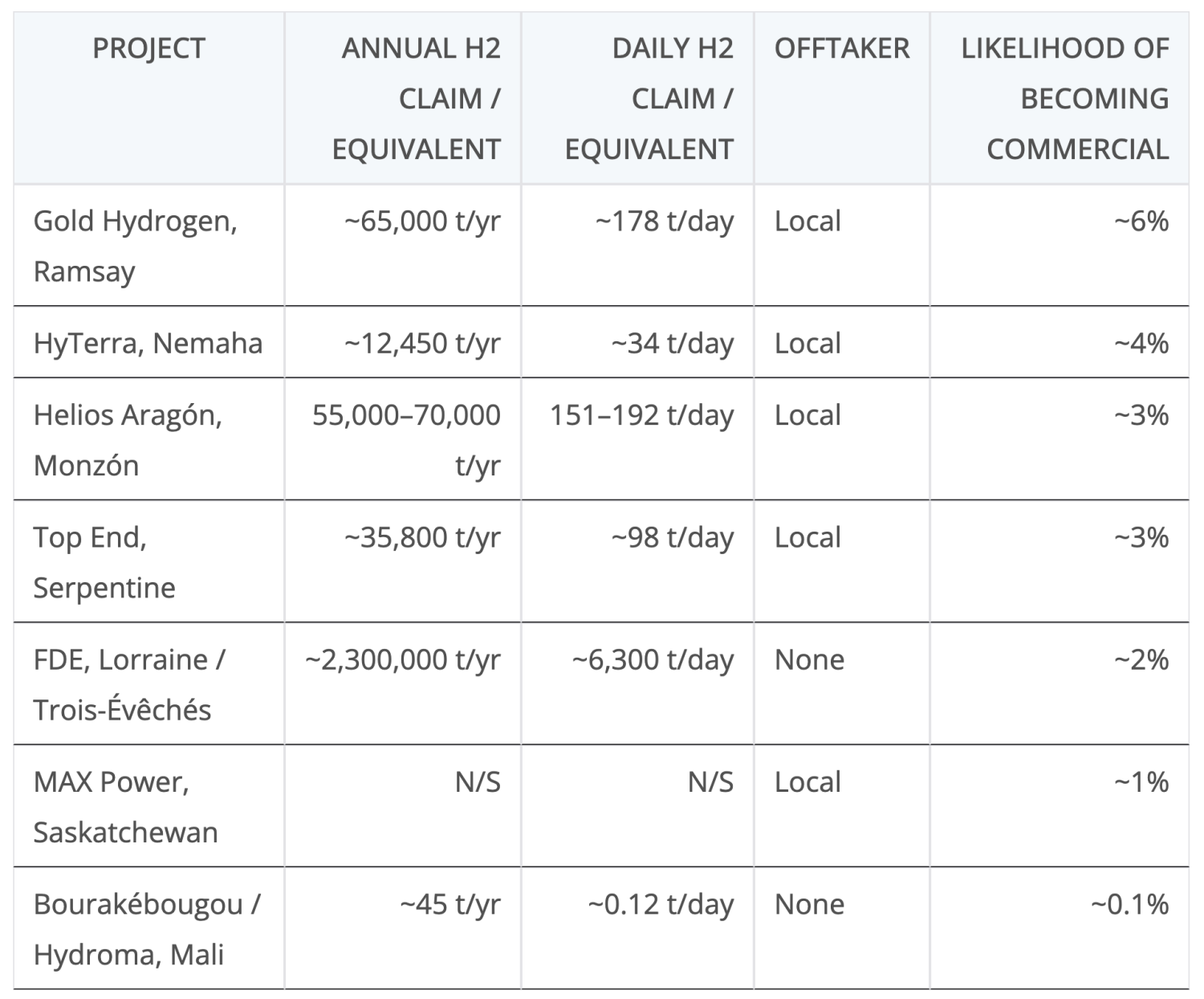

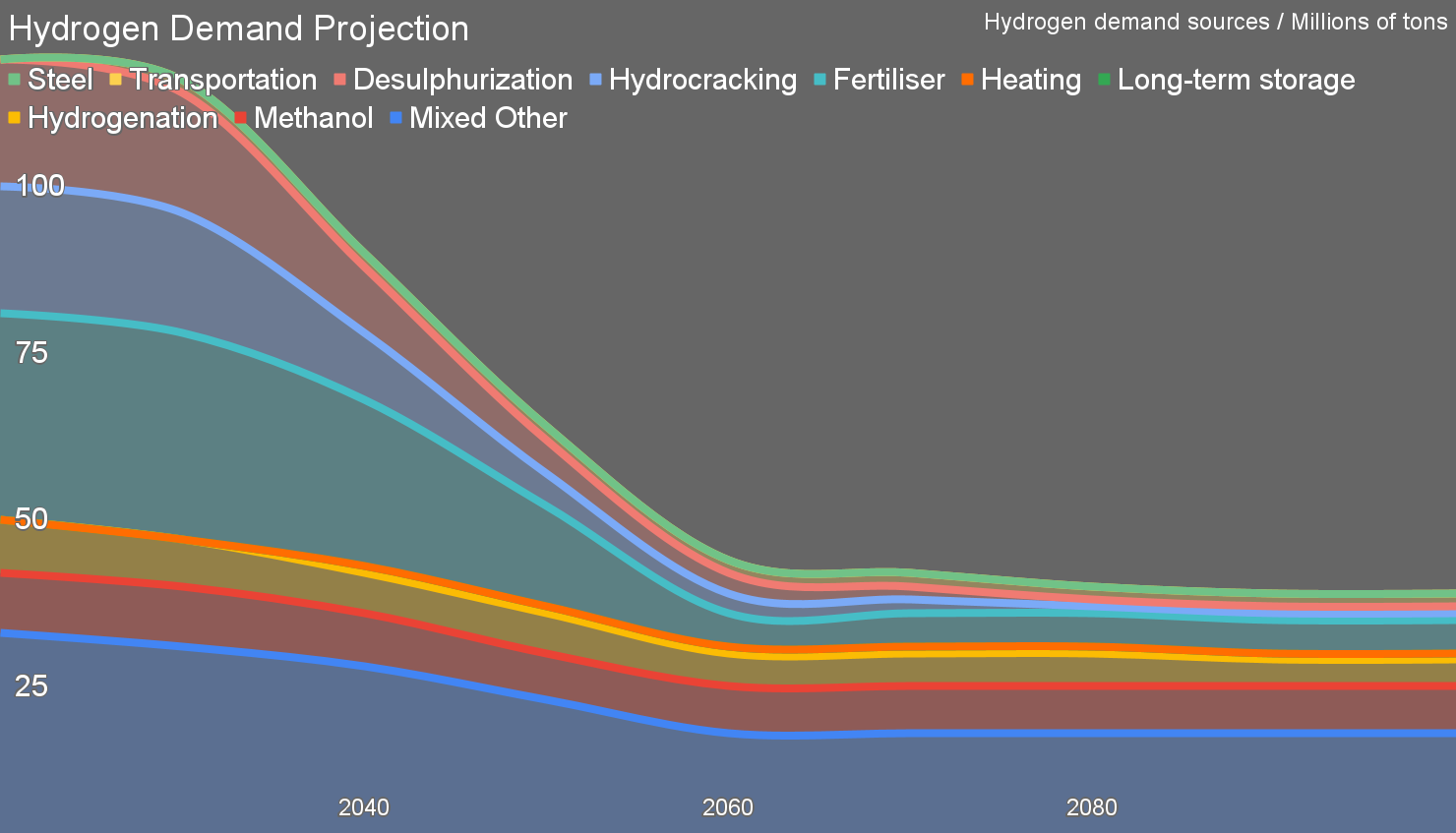

A couple of years ago I wrote that natural hydrogen was interesting as geology, but not as a limitless new clean fuel economy. That remains the right starting point. The state of play in 2026 is not that the miracle arrived late. It is that the sector has moved from speculative headlines toward the first stage of real extractive industry discipline. That is progress. It is also a narrower and more demanding story than the headlines suggested. The question is no longer whether hydrogen exists underground. It does. The question is whether anyone has found enough of it, in the right place, at the right rate, to support a durable industrial business. That is a tougher question, and it is the only one that matters. The first thing worth clarifying is the distinction between hydrogen generation, hydrogen presence, and hydrogen reserves. Geologists have become increasingly confident that natural hydrogen is generated in multiple settings, including serpentinization, radiolysis, iron oxidation, and other crustal processes. But generation is not the same as accumulation. Plenty of hydrocarbons are generated that never become fields. Natural hydrogen has the same problem, amplified by chemistry and physics that are less forgiving than methane. Hydrogen is small, reactive, prone to leakage, and vulnerable to loss through microbial activity and abiotic reactions. A natural hydrogen system has to generate gas, migrate it, trap it, seal it, preserve it, and then deliver it at commercial flow rates. Missing any one of those steps is enough to kill the project. The current public record still lacks widely disclosed reserve figures, and even the benchmark Mali field does not have publicly verified reserve numbers. That makes the right framework familiar rather than exotic. This sector should be judged with the same discipline used in oil and gas. A prospect is not a resource. A resource is not a reserve. A reserve is not just gas in the ground. It is gas that has been found, appraised, shown to be recoverable, tied to a development concept, and linked to a commercial case. Natural hydrogen companies have become better at using the language of prospective resources and appraisal. That is a step up from the early wave of stories that jumped from trace concentrations to trillion-dollar dreams. But the sector is still mostly sitting at the prospect or prospective resource stage, with a few names edging toward what could become contingent resources if appraisal wells and testing go well. That is a real industry beginning to form. It is not a mature extraction sector. Table of natural hydrogen plays, by author. The projects above were assessed using a hybrid extractive-industry framework anchored in conventional oil and gas resource classification and then tightened with an industrial feedstock lens. Each site was screened first for geological credibility, meaning evidence of a working hydrogen system with generation, migration, trapping, sealing, and preservation rather than isolated concentration readings. It was then evaluated for scale using a practical threshold derived from ammonia production, requiring a plausible pathway to at least about 200 tons per day of sustained hydrogen output, which corresponds to a small 1,000 tons per day ammonia plant. The third filter was location and offtake, prioritizing proximity to existing industrial hydrogen demand such as ammonia, refining, or methanol rather than speculative future hydrogen markets. Projects that did not publish annual or daily production assumptions were normalized by spreading best public resource claims over a 15 to 20 year production window to estimate implied throughput. Finally, all claims were discounted where they remained at prospective resource stage without appraisal, deliverability testing, or a defined commercialization pathway, reflecting the gap between geological potential and reserve-class assets. Hydrogen demand projection through 2100 by author, adjusted for decreased demand in Hydrogenation and Mixed Other. In my most recent assessment of hydrogen markets, I put current global demand at roughly 95 million to 100 million tons per year, or closer to 120 million tons when captive and process hydrogen are fully counted, and projected that total demand could decline to under 50 million tons by 2100 as refining shrinks, ammonia stabilizes, and many marginal uses decline due to economic pressure. Against that reality, the roughly 2.47 million to 2.48 million tons per year implied by annualizing all currently cited natural hydrogen discoveries and modeled plays is an absolute best case ceiling from exploration to date. It is not a reserve base, not a production forecast, and not a set of bankable projects. Most of it is still prospective resource, modeled potential, or early discovery language rather than appraised and financeable assets. The vast majority of it, 2.3 million tons or 93%, is from the French site which has perhaps a 2% chance of seeing reality. Even taking that number at face value, it amounts to only about 2.5% of today’s core hydrogen market, about 2.1% of the broader 120 million ton figure, and roughly 5% of my long-term demand projection. Put simply, the entire natural hydrogen story so far, in its most optimistic framing, falls well short of replacing even a modest share of realistic future hydrogen demand, never mind becoming a source of new energy. There is one place in the world that still matters more than any other in this discussion, and that is Bourakébougou in Mali. It is the only location producing hydrogen for local benefit, and it is the best-known case of natural hydrogen actually being tapped and used. The field has been drilled multiple times and has demonstrated high hydrogen concentrations. It has provided about 6 kW of local electricity for years, very useful in energy poor Mali prior to the existence of solar panels and batteries, but minuscule by developed world expectations. The numbers are sobering when viewed through an industrial lens. The reported flow rate of the discovery well is about 1,500 cubic meters per day, which translates to roughly 0.13 tons per day, or about 45 tons per year. That is enough to prove existence. It is nowhere near enough to anchor an ammonia complex, a steel plant, or any industrial hydrogen business of scale. The Mali case also helps separate two different narratives that have been blended together too often. One is the reservoir narrative, where hydrogen has accumulated over long periods and can be produced like a gas field. The other is the continuous generation narrative, where hydrogen is being formed rapidly enough in the present to support ongoing offtake without requiring much accumulation. The second story is more attractive because it sounds renewable in the everyday sense. It is also far less demonstrated. Recent analysis of hydrogen flow rates and viability indicates that a system capable of sustaining industrial offtake rates while replenishing itself rapidly is unlikely. Even in optimistic scenarios, it would take centuries to fill a reservoir of the required size, and more realistic cases run into thousands or tens of thousands of years. That does not rule out commercial natural hydrogen. It does rule out many of the claims about self-recharging wells feeding a large energy system. Once that is clear, the next filter is market reality. The right lens is not electricity generation, long-distance transport, or home heating, as has become very clear globally through the collapse of the cheap green hydrogen hype bubble. The right lens is industrial feedstocks, especially ammonia, and to a lesser extent refining, methanol, and selected chemical uses. Ammonia remains one of the largest and most durable hydrogen markets in the world. Ammonia consumption has represented a large share of global hydrogen demand for years. The chemistry is straightforward. Ammonia is about 17.8% hydrogen by mass. Every 1 ton of ammonia requires about 0.178 tons of hydrogen. A plant producing 1,000 tons of ammonia per day needs roughly 178 tons of hydrogen per day. A 2,000 tons per day plant needs about 356 tons of hydrogen per day. Modern scaled plans producing 3,000 tons of ammonia daily, requiring 534 tons. That’s with a perfectly efficient ammonia synthesis process, so reality requires more. These numbers matter because they shrink many natural hydrogen headlines down to a scale that looks much less transformative. That industrial lens also changes how projects should be ranked. A natural hydrogen accumulation in the wrong place is not especially valuable. Hydrogen is expensive to move compared with natural gas, liquids, or electrons. The logistics and losses do not disappear because the hydrogen is geologic instead of electrolytic. A field close to existing ammonia, methanol, or refining demand has a real advantage. A larger field in a remote area may still struggle to justify development unless it is large enough to support dedicated downstream conversion, and large enough to do that for decades. This is where the hype around white hydrogen often lost the plot. The sector was treated as if any large geologic number could be poured into a future hydrogen economy. In practice, the real question is whether the field is near a durable hydrogen sink that already exists, or can be justified without a stack of speculative downstream assumptions. Spain’s Helios Aragón project is a good illustration of both the progress and the limits of the current moment. The project materials state a most likely recoverable volume of 1.1 million tons of hydrogen and plateau production between 55,000 tons and 70,000 tons per year starting near the end of the decade. That annual figure converts to about 151 tons to 192 tons per day. On first glance that sounds serious, and it is one of the few projects talking in something like field-development language. But when run against ammonia math, it becomes less compelling. The low end of the plateau is below the hydrogen required for even a 1,000 tons per day ammonia plant. The high end just reaches that neighborhood. The project is framed around supplying local industry and regional demand. What it does not show publicly is a named anchor offtaker with a long-term feedstock requirement. This may be one of the more advanced public natural hydrogen stories. It is not yet a reserve-backed ammonia story. Australia’s Gold Hydrogen is a different kind of case. It has one of the clearer public prospective resource claims, with a mean prospective resource of about 1.3 million tons of hydrogen. Drilling has shown high hydrogen concentrations. The company argues that natural hydrogen offers a cost advantage because it does not need to be manufactured. The challenge is that resource and cost claims still sit upstream of the key hurdles. The figure is prospective, not a reserve. The reservoir has not been fully appraised. The company has discussed supplying local ammonia plants, which is the correct commercial direction. But to turn 1.3 million tons into a viable ammonia business, the project still needs to prove reservoir integrity, sustained deliverability, and long-term commercial contracts. Spread over 20 years, that resource would average about 65,000 tons per year, or about 178 tons per day. That is at the threshold of a modest ammonia plant and not much beyond it. Kansas has become interesting because of its industrial context. HyTerra and Top End are both exploring there, and the region has a high concentration of ammonia production. HyTerra reports hydrogen concentrations up to about 96% in a discovery well and points to the surrounding industrial base as potential offtake. That is a strong location advantage. But its prospective resource is relatively modest and the company is still working to demonstrate reservoir deliverability. Top End reports a mean prospective resource equivalent to about 716,000 tons of hydrogen. Spread over 20 years, that becomes roughly 35,800 tons per year, or about 98 tons per day. That is below the scale needed for a meaningful ammonia anchor. Location helps these projects. It does not eliminate the need for sustained industrial flow rates. France’s Lorraine basin highlights the gap between scientific potential and commercial reality. The widely cited estimate of 46 million tons at depth is based on modeling and represents potential, not a reserve. In fact, it doesn’t even meet the bar to be considered a resource. The current work in the basin is focused on confirming hydrogen presence across multiple intervals and building a geological understanding of the system. Initial certification is still targeted for the future. Even if the basin holds large volumes, the path from modeled potential to a producing field that can supply industrial feedstock remains long. It represents 93% of claimed natural hydrogen resources, it’s nowhere near offtakers, and it doesn’t meet the bar for being a resource. Canada’s MAX Power sits in a region with strong industrial hydrogen demand and has reported discovery-level hydrogen concentrations and evidence of gas movement. The location is favorable because of nearby refining and fertilizer demand. But the project has not yet published a resource estimate that allows comparison with other plays, and it has not demonstrated sustained production capability. It remains at an early stage. A useful way to summarize the sector is that geology, volume, and location each eliminate most projects. Bourakébougou passes geology and fails scale. Helios may pass geology and partly pass scale, but lacks a demonstrated anchor customer. Gold may have enough prospective scale to matter, but still must prove the reservoir and the commercial case. HyTerra has a strong location but limited demonstrated scale. Top End has some scale and location, but limited maturity. Lorraine has a large modeled potential but early-stage commercial development. MAX has location but little public scale. Many projects remain stories that have not yet been converted into industrial propositions. The core argument from a couple of years ago still stands. Hydrogen should be judged by lifecycle carbon intensity and commercial logic, not by labels. The most durable hydrogen demand remains in industrial feedstocks. Distribution remains a constraint. Natural hydrogen has moved from curiosity toward early-stage extractive industry, but it has not yet reached the point where it can support large-scale industrial transformation, and there is little likelihood that it will. Money invested to date is far more likely to be lost than to turn into anything bankable. The fair question is what would change that conclusion. A publicly documented contingent resource would matter. A reserve statement would matter more. Sustained industrial flow rates would be critical. A project demonstrating 200 tons per day or more of hydrogen near an ammonia or methanol offtaker would change the conversation. A development plan that does not depend on speculative hydrogen energy demand would be equally important. Until those conditions are met, natural hydrogen remains an interesting geological opportunity with unlikely commercial outcomes.