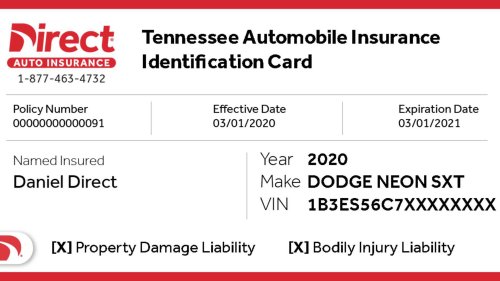

Jump LinksLiability InsuranceFull Coverage InsuranceWhat does liability insurance cover you for?What is not covered by liability insurance?Is it better to have a $500 deductible or $1,000?What are the benefits of liability coverage?Car ownership calls for more skills, responsibilities, and expenses than just meeting the purchase price and ensuring you are a legal, registered driver on the road (with the appropriate permit in your possession). In addition to keeping up to date with the vehicle’s roadworthiness and ensuring it is maintained to schedule, it’s also the expectation under law that you ensure your vehicle is insured. This is true no matter the car you own, be it a six-figure Mercedes-AMG GT63, or a hyper-economical Nissan Versa.Car owners have plenty of choices when it comes to choosing which insurer to go to for securing a quote, but it can be hard to determine how comprehensive your respective insurance plan should be - specifically, judging whether liability vs full coverage is worth paying the premium for. We’ll aim to outline the key difference between liability and full-coverage insurance plans here to help you assess which could prove to be the better purchase.All information has been cited by reputable sources, including insurance agencies and the latest state government laws. Car Insurance Basics: Liability vs. Full Cover Toyota Car insurance is an important item that must be accounted for as part of standard car ownership procedures. As much as you may strive to be a safe and sensible driver on the road, mistakes can still happen; it serves as a form of protection against you and any other road users in the rare cases of an accident. Having insurance coverage of some degree ensures that you, the insured party, are not liable for the full amount of compensation owed to the other parties involved; the insurance provider will cover these expenses (to an extent)."Car insurance is a contractual agreement between a driver and an insurance provider that offers financial protection in case of accidents, theft, or other unexpected vehicle-related incidents... car insurance acts as a critical safeguard, ensuring that unforeseen events don’t lead to overwhelming financial burdens."- GEICONo matter what type of vehicle you intend to own and register to use on the road, whether it be a Toyota Corolla or a Ford F-150, it is a mandatory requirement (per state law) that the vehicle must be insured at any time it is registered and intended to be used on the road. The only state that does not require this is New Hampshire, though you still need to guarantee you can afford repairs in the event of an accident. Depending on what type of insurance company you secure a quote with and the type of vehicle you want it to apply to, certain insurance plans can be created for unique circumstances or types of vehicles, offering a far more reasonable and competitive rate (e.g. classic cars, enthusiast-grade vehicles).Direct Auto Insurance The insurance provider will issue some form of documentation that contains key information about the vehicle, the primary user(s), the date of issue, and the date of expiry for the insurance policy. These can be presented both electronically and physically via a dedicated insurance identification card, which the insurance policyholder will be expected to have on their person at all times. Law enforcement, along with certain automotive businesses (e.g. safety inspection stations), may request the driver to present this documentation to confirm the vehicle is still insured at the present time."Also known as an Insurance Card, this card is issued by your insurer and contains basic information about your insurance policy. Some states require you to keep an insurance ID card in your vehicle."- GEICOMost insurance agencies offer two types of plans for policyholders with automotive needs: limited and full coverage. In this article, we have outlined some of the most significant ways they differ when comparing liability car insurance vs full coverage. Liability Insurance Liability insurance coverage is viewed as the most basic form of automotive insurance, ensuring compensation can be paid for harm or damage caused to other objects or individuals in the event of an accident, no matter how major or minor. In most US states, registered drivers are required to purchase and provide proof of liability coverage as part of owning or purchasing their vehicle, which serves as a minimum amount of insurance to satisfy state regulations."Auto liability coverage pays for damage you cause to others - including physical injuries to people and property damage - and it's required in nearly every (United States) state"- ProgressiveMost liability car insurance plans cover these two specific areas: Bodily Injury Liability: medical expenses for those injured in an accident where the insurance policyholder is at fault Property Damage Liability: compensation that is paid out to cover repairs/replacement to third parties’ respective property that is damaged by the insurance policyholder. Some examples of this include damage to other vehicles or private property. Full Coverage Insurance Full coverage insurance is far more comprehensive compared to liability insurance plans. Comparing full coverage vs liability car insurance, policyholders are entitled to far more benefits on top of what they are get under a liability insurance plan, typically beyond just accident damage or injuries incurred to anyone or anything, and not just the policyholder and their property: More comprehensive damage coverage: damage caused by means other than vehicular accidents (theft, vandalism, natural disasters or declared "acts of god." Compensation against insured motorists, property damage, or collisions: in the event the policyholder is involved in accidents where they are not at fault, but the other parties are found not to have a valid insurance, the insurance provider will still provide compensation for any injuries or damage to the policyholder and/or their vehicle. Medical expenses coverage: unlike liability vs full coverage insurance, policies that fall under the latter will cover, or provide reimbursement for, any medical bills filed under the policyholder (and any passengers riding in the vehicle) in the event of an accident. Rental car reimbursement: full coverage plans may include some allowance to cover a rental car for the policyholder to use, in the event their registered vehicle is damaged/stolen and is temporarily out of service while it is repaired, or the time it takes for a replacement vehicle to arrive. While the premium for full coverage is higher than that for liability coverage, the peace of mind its more comprehensive benefits offer policyholders is viewed as justification for the higher price. The Advantages Of Full Coverage Insurance vs Liability Image: Ulrick Trappschuh / PexelsThe key advantages of going for full coverage vs liability insurance plans is that policyholders have peace of mind that both themselves and other parties will not have to pay for any expenses to settle damage or injuries they experience. Under most insurers, this will ensure that the vehicle’s registered owner does not need to pay out of their own pocket for any damages or injuries of any party involved, including non-vehicular objects like property (though some plans may dictate whether public and/or private property is covered, unless additional protection has been paid for).Despite this, it’s worth knowing that full coverage may not cover every expense the registered owner may encounter or attempt to file for reimbursement. General wear/tear of components and roadside assistance, for instance, may only be covered or provided if the policyholder pays for these extras separately. Use of the vehicle for ride-sharing or courier duties (i.e. Uber/Lyft), or in an environment outside a public road, may also void any benefits under a full coverage plan.Compared to liability vs full coverage, opting for the more comprehensive plan fulfills more than what is considered by most state governments as the bare minimum when it comes to protection against other motorists if an accident were to occur under the driver’s watch. Does Liability Insurance Offer Enough Benefits? Advocates for Highway and Auto Safety The main difference between liability and full coverage insurance is indeed the price the policyholder will have to pay (aside from other factors like any applicable no-claims bonuses, driving record, and type of vehicle the policy covers), but comprehensive benefits aside, some car owners may find liability insurance provides enough to satisfy their requirements. This is especially true if the car is of a certain age or value that is not worth paying an excess premium to insure, if any potential repairs to the vehicle are not too expensive, or if the registered owner intends to only use the vehicle for a certain number of days in the year, among other potential reasons.However, it’s important to highlight that under a liability insurance plan vs full coverage, the policyholder will be expected to cover any and all costs related to repairing their personal vehicle involved in the accident."Liability coverage covers others when you are at fault in an accident. Liability coverage is an important minimum for auto insurance. If you only choose liability insurance, your damages are not covered. "- AAA (American Automobile Association)Other limitations of liability-only insurance plans can also include: Not providing compensation in the event of "hit-and-run" accidents, or if the insured vehicle was being driven by anyone other than the registered driver(s). Not providing compensation if the vehicle is stolen or damaged by natural disasters, vandalism. Not providing coverage if the insured vehicle has been used for any means other than private, general use (e.g. ride-sharing, track days, off-roading). Ultimately, car owners are highly advised to exercise due diligence to shop around as much as possible between insurance companies to figure out which plan, along with their respective terms/benefits, policyholders are entitled to best meet their needs, budget, and expectations. FAQs What does liability insurance cover you for? Most liability car insurance policies will typically cover any damage and associated legal expenses incurred to parties other than yourself, such as, but not limited to, damage caused to other vehicles, property, and/or pedestrians. What is not covered by liability insurance? Typically, liability insurance plans do not cover damage inflicted on your own vehicle or any injuries you report. The general rule is that liability-only insurance does not cover any of your personal damage/costs, whether you are identified to be the driver at fault or not. Is it better to have a $500 deductible or $1,000? Judging whether having a $500 deductible versus a $1,000 deductible is dependent on the given circumstances and budget unique to the policyholder at any given time. What are the benefits of liability coverage? Under liability insurance coverage, aside from covering the basic requirements of vehicle insurance, the primary benefit is that the insurance policyholder does not need to pay for any expenses caused to third parties if they are at fault in an accident. Liability coverage will cover bodily injuries and property damage, as well as vehicle damage experienced by anyone other than the policyholder.