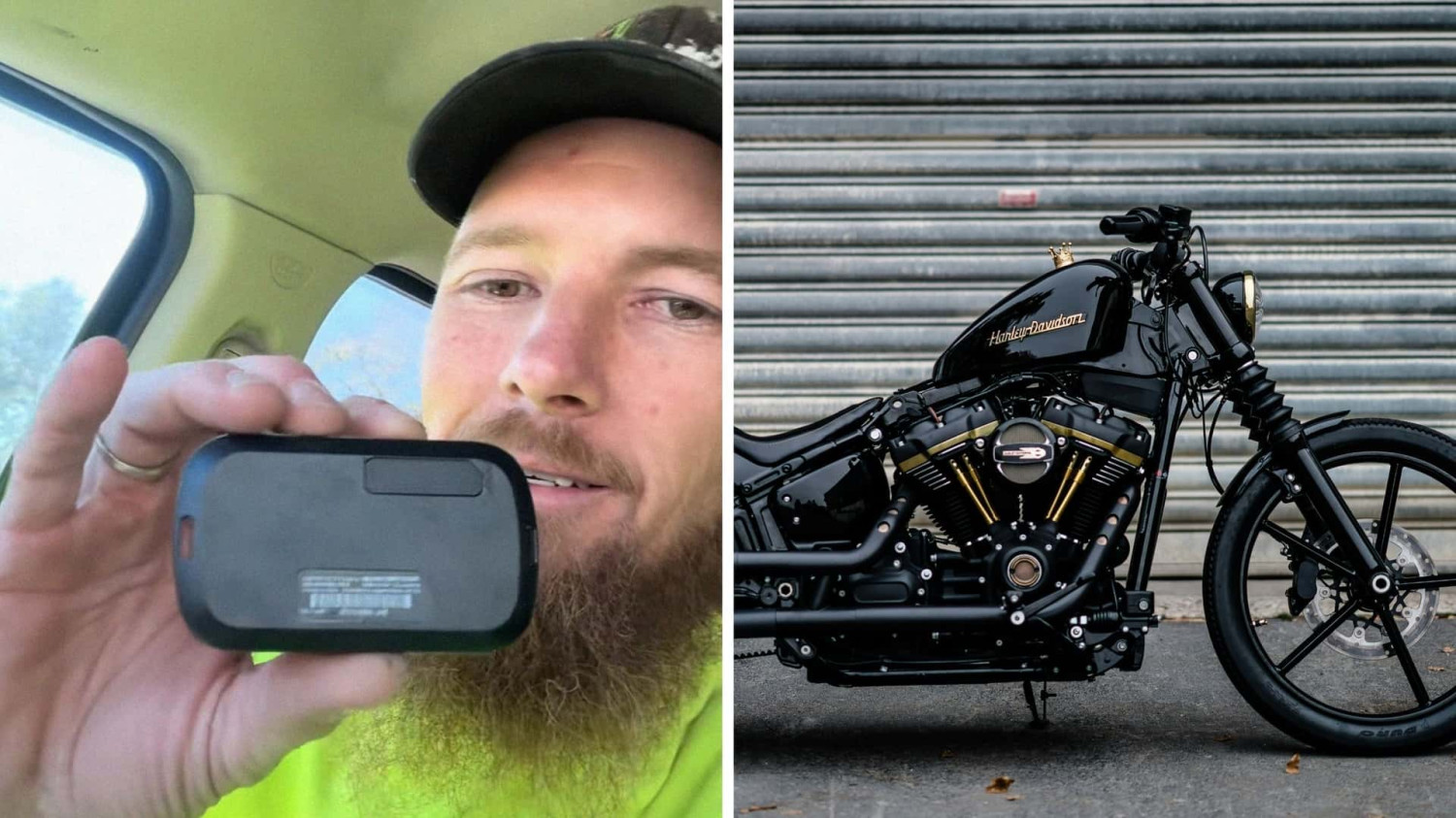

Anyone who's recently purchased a motorcycle likely has had a hidden spy riding along with them. That's what we learned from a man who recently bought a Harley-Davidson. He’s warning other motorcycle owners about the possible presence of hidden tracking devices on their vehicles. Florida TikTokker HighLife (@highlife0580) appears satisfied with himself in a video showing the tracking device he said was secured behind the right saddlebag of his motorcycle. After removing the device, which was about the size of a computer mouse, he tossed it out the window of his truck to avoid further monitoring. "So when you find it, this is what you do with it," he says in the clip that has more than 38,000 views, before throwing the device on the road. "Get rid of that [expletive]!" Understandably, the clip played on the anxieties of modern motorists that their highly wired vehicles might be watching them wherever they go. The tracker was almost certainly installed by the lender, rather than Harley-Davidson. Tracking devices like the one seen in the clip are commonly used by lenders and dealerships to protect financed vehicles. In some cases, they’re marketed as theft recovery devices, while in others, they're tied to loan terms that allow lenders to locate or even repossess a vehicle more easily if payments stop. Commenters who’ve seen these devices before said they're typically disclosed in the financing paperwork, even if most buyers don't realize what they've agreed to in the moment. That context didn't calm tempers in the video's comments section, which escalated into a heated debate among riders, dealership employees, and finance veterans sharing wildly different experiences and viewpoints. One commenter, who identified as a Harley-Davidson dealership employee, claimed that trackers are typically installed only when lenders don't trust a buyer's creditworthiness. Others pushed back, saying they had excellent credit scores and still found similar devices on their bikes. "They make you sign an acknowledgment waiver saying they are going to place a GPS on your bike," one wrote, adding that his older, lower-credit-score purchase had one while his newer bike did not. Another person warned bluntly: "Don’t remove it if you’re financing. Usually, in the contract, if you remove it before you pay it off, they can repo it immediately." Are Auto Loan Companies Watching You? The 20-second clip glosses over any details about what the device actually does once installed. Most lender GPS units aren't constantly "spying" in the cinematic sense, but they do transmit location data and, depending on the system, may store a limited history of the vehicle's location. Those data patterns are enough to make repossession or recovery significantly easier and far cheaper than old-school skip tracing. That data typically resides with the lender's tracking service provider, rather than with the manufacturer. Some financing agreements also allow them to share that information with law enforcement if a vehicle is reported stolen, a detail some commenters noted was included in their own loan documents. In some cases, more advanced versions of these systems can support remote immobilization, although that feature isn't always enabled and isn't universal across motorcycles. In practice, lenders typically reserve remote immobilization for extreme cases, as disabling a bike remotely raises safety and liability concerns. It's also worth noting that these devices aren't unique to motorcycles and are already widespread in subprime auto loans, at buy-here pay-here dealerships, rental fleets, and commercial vehicles, where tracking has become an assumed part of financing costs. Reading the Lending Paperwork Discovering a tracker like this may cause unease, but the simple truth is there's nothing illegal going on, especially since the use of such devices is disclosed in financing contracts. In most states, lenders may require tracking or recovery devices on financed vehicles, provided the buyer agrees in writing. That agreement is often buried in dense loan paperwork, which helps explain why so many riders are surprised to discover the device later. Anyone looking to avoid this kind of external monitoring can pay in full for their vehicle, eliminating any ongoing recovery obligations for the lender or dealership. Otherwise, it depends on the lender's and dealership's requirements, though some finance companies may waive the requirement for certain creditworthy borrowers. But some won't negotiate on this at all. In the broader context, this underscores the importance of paperwork literacy in any vehicle purchase. If you're financing, look for language about tracking, recovery devices, data sharing, or immobilization. Find out where the device is installed, who controls the data, and what happens if it's damaged or removed. Motor1 reached out to HighLife via direct message and commenting on the clip. We’ll update this if he responds. We want your opinion! What would you like to see on Motor1.com? Take our 3 minute survey. - The Motor1.com Team