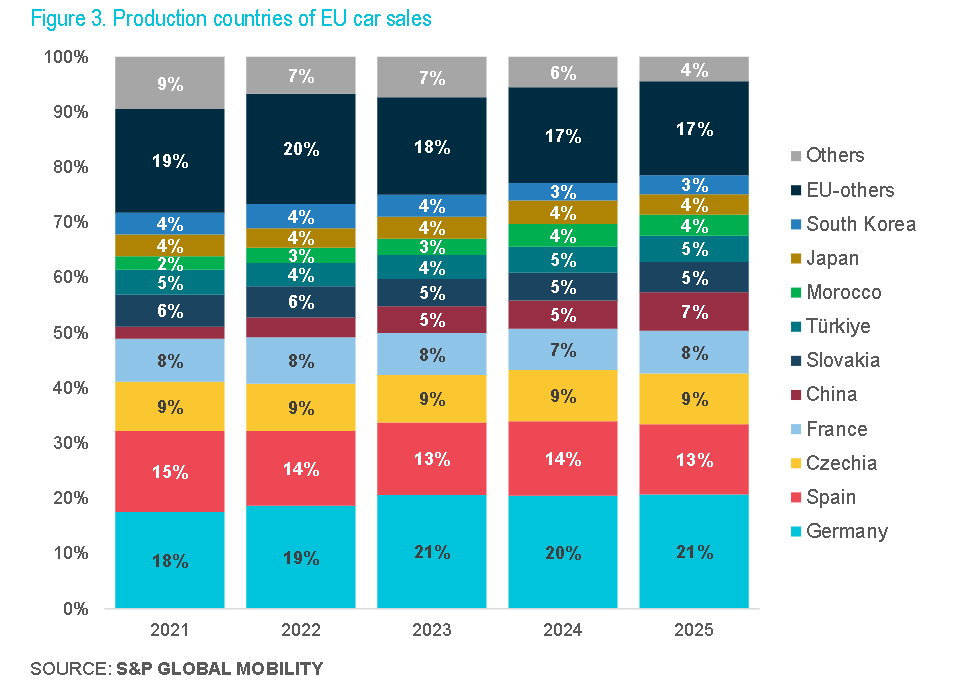

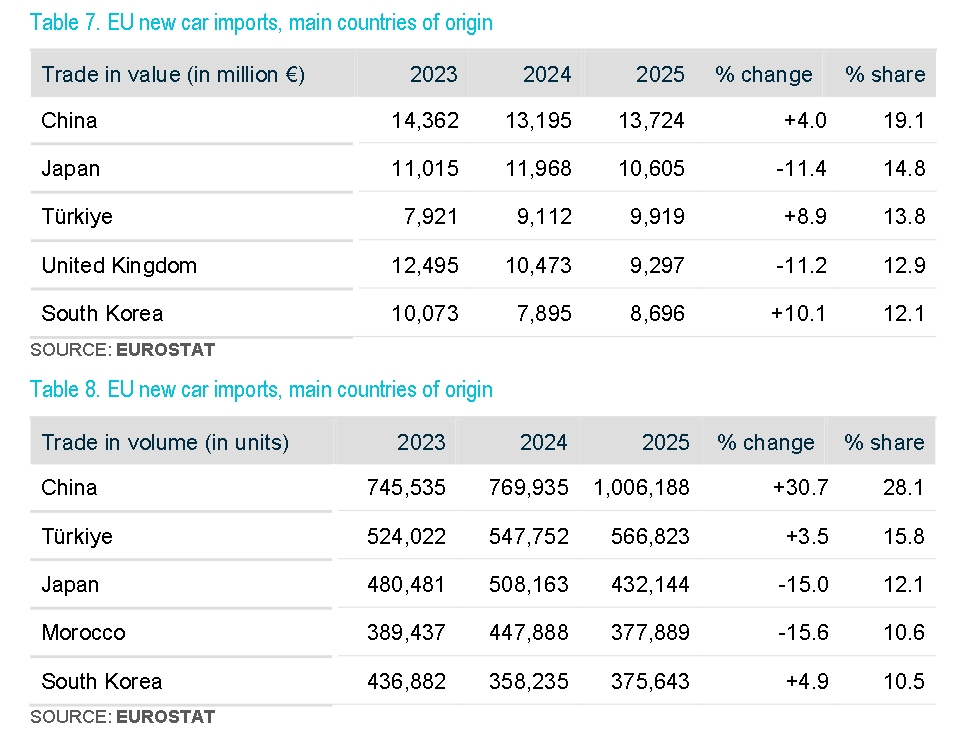

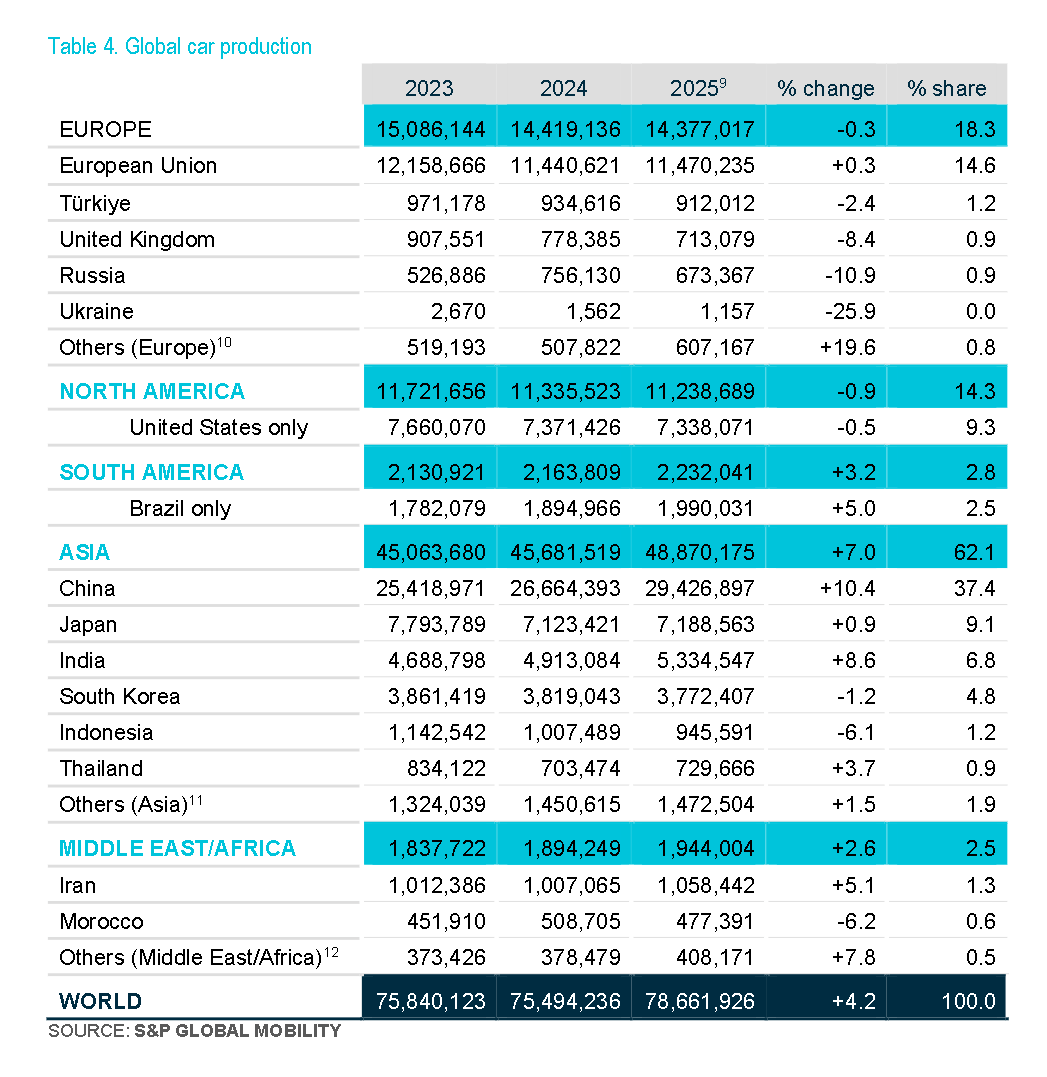

The European Automobile Manufacturers’ Association recently released its “2025 Global and EU Automotive Industry Economic and Market Report.“ Data shows that global automobile production reached 78.7 million units in 2025, a year-on-year increase of 4.2%. Among this, the Asian market contributed 62.1% of total production, while the European Union accounted for 14.6%. In terms of new vehicle registrations, global registrations reached 77.6 million units in 2025, up 3.5% compared to 2024. Registrations in the Asian market accounted for nearly half of the global total, with a growth rate of 4.8%. Specifically, the Chinese market grew 5.5% to 24.2 million units, supported by government scrappage subsidies and NEV purchase tax policies. Meanwhile, registrations in India, South Korea, and Japan all showed upward trends, increasing by 5%, 4%, and 3.2% respectively. Production countries of EU car sales In the EU automotive import market, China continued to be the largest source of car imports to the EU in 2025, with an import value of €13.7 billion, accounting for 19.1% of total EU import value. By volume, imports from China surged 30.7% year-on-year, surpassing the 1 million unit mark and representing 28.1% of total EU import volume. In stark contrast, the value of Chinese imports grew by only 4%. Behind these figures lies a market strategy of “volume for price” adopted by Chinese brands, rapidly seizing EU market share with cost-competitive models. EU new car imports, main countries of origin By comparison, Japan’s automotive exports to the EU fell 15.0%, the UK dropped 11.2%, and Morocco plunged 15.6%. Among the top five import sources to the EU, China leads by a wide margin with over 28% share, followed by Turkey (15.8%) and Japan (12.1%), though their growth rates lag far behind China’s. By trade value, China still ranks first, with Japan and Turkey taking second and third place at €14.8 billion and €9.9 billion respectively, though Japan’s export value declined 11.4% year-on-year. Global car production Among new cars sold in Europe, Germany remains the top source of vehicles sold in the EU with a 21% share, followed by Spain (13%), the Czech Republic (9%), and France (8%). Notably, vehicles produced in China now account for 7% of the total, surpassing Turkey (5%) and Morocco (4%) to become the largest source of vehicles from outside the EU. This trend is closely linked to the accelerated European expansion of Chinese brands such as BYD, SAIC, and Great Wall Motors. Despite ongoing disputes over EU tariffs on Chinese electric vehicles, Chinese brands are seeking breakthroughs through localized production and hybrid technology routes. The 7% share may be just the beginning.

![[Gasgoo News] XPENG GX officially announced; China's NEV insurance premiums up 34.8% YoY in 2025](https://cdn.topcarnews.net/thumb/id/aHR0cHM6Ly9pbWFnZWNuLmdhc2dvby5j-b20vbW9ibG9nby9OZXdzL1VFZGl0b3Iv-aW1hZ2UvMjAyNTA2MTAvNjM4ODUxNzAw-MTkzODM1OTU2NTQxNDEzNi5qcGc/c06991c2ffe2e05fe81c97062ebd8cf3.jpg?t=20260722&post_id=12479)