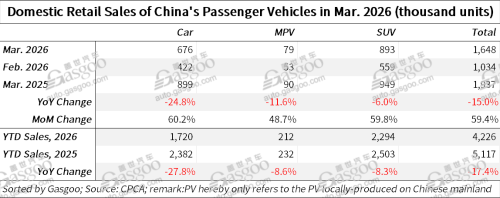

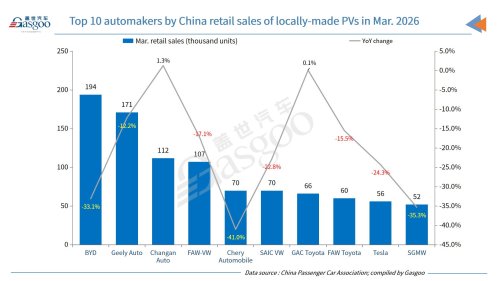

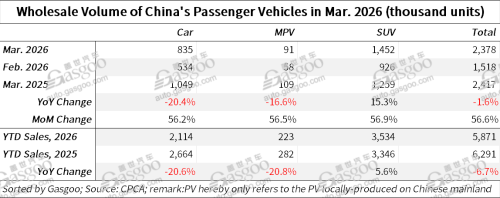

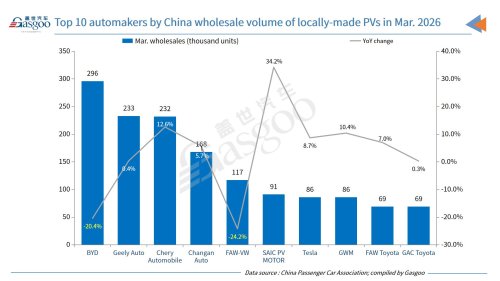

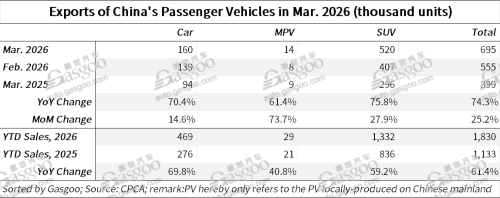

Gasgoo Munich- China's passenger vehicle (PV) market showed a mixed performance in March 2026, with retail sales reaching 1.648 million units, down 15% year-on-year but rebounding 59.4% from February, according to data from the China Passenger Car Association (CPCA).For the first quarter, the country's cumulative PV retail sales totaled 4.226 million units, representing a 17.4% decline compared with the same period last year.For clarity, the PVs mentioned here are all locally produced on the Chinese Mainland.The CPCA noted that overall market performance in the first quarter slightly exceeded expectations, despite the year-on-year decline. Seasonal and policy-related factors continue to distort demand patterns, with sales in recent years typically skewed toward the second half. In 2026, the late timing of the Chinese New Year, combined with ongoing adjustments to fiscal and tax policies, contributed to weaker retail activity early in the year, followed by a gradual recovery.China's self-owned brands recorded retail sales of 1.02 million units in March, down 16% year-on-year but up 61% month-on-month, capturing a 61.8% market share—0.8 percentage points lower than a year earlier. While performance in the new energy vehicle and export segments remained relatively stable, leading legacy automakers undergoing transformation, such as Geely and Changan, continued to expand their market presence.Mainstream joint-venture brands posted retail sales of 410,000 units in March, marking a 13% year-on-year decline and a 54% increase from the previous month. German brands accounted for 16% of the market, down 0.7 percentage points year-on-year, while Japanese brands improved their share to 13.3%, up 1 percentage point. U.S. brands held a 6.9% share, edging up 0.1 percentage points over a year earlier, while South Korean brands remained broadly stable.Luxury vehicle retail sales reached 210,000 units in March, down 15% year-on-year but rising 62% from February. As pricing strategies normalized, the segment's retail share edged up to 12.9%, suggesting early signs of stabilization in the Luxury market.PV wholesale volumes reached 2.378 million units in March, down 1.6% year-on-year but up 56.6% month-on-month. Driven by a sharp surge in exports, wholesale growth outpaced retail by 13.4 percentage points.Chinese automakers sold 1.611 million units by wholesale, up 2% year-on-year and 50% from February. Joint-venture brands recorded 490,000 units, down 10% year-on-year but surging 75% month-on-month, while Luxury vehicle brands record a wholesale volume of 270,000 units, down 3% year-on-year and up 69% month-on-month.The competitive landscape among major automakers continued to evolve, with companies including Geely, Chery, Changan, SAIC MOTOR Passenger Vehicle, Tesla, FAW Toyota, GAC Toyota, Dongfeng Nissan, Dongfeng Motor, Leapmotor, and SAIC-GM all reporting year-on-year wholesale growth.Five automakers recorded monthly wholesale volumes exceeding 100,000 units, up from three in February and in line with the same period last year, accounting for 44% of total market share. Manufacturers with monthly volumes between 50,000 and 100,000 units held a 31% share, while those in the 10,000–50,000 range accounted for 21%.A total of 19 PV models recorded wholesale volumes exceeding 20,000 units in March, up sharply from eight models in February. Leading the list were BYD Song with 66,989 units and Tesla Model Y with 55,856 units, followed by Geely Xingyuan at 40,613 units and Chery Tansuo 06 at 36,583 units. Other high-volume models included BYD Seagull (30,636 units), Tesla Model 3 (29,814 units), Nissan Sylphy (27,514 units), Chery Tiggo 7 (26,895 units), and BYD Dolphin (25,770 units), alongside several popular SUVs and sedans such as Geely Boyue, Li i6, Changan EADO, Changan CS75, Yuan UP, Toyota RAV4, etc.New energy vehicles accounted for the majority of these top-selling models, highlighting their dominant position in the market.PV exports, including fully built units and CKD kits, surged to 695,000 units in March, up 74.3% year-on-year and 25.2% from February. New energy vehicles accounted for 50.2% of total exports, an increase of 14 percentage points compared with a year earlier.Chinese brands dominated overseas shipments with 606,000 units, up 76% year-on-year, while joint-venture and Luxury brands exported 88,000 units, rising 65% from a year earlier.PV production reached 2.364 million units in March, down 4.9% year-on-year but jumping 72.2% month-on-month.Luxury vehicle output increased 1% year-on-year and 73% month-on-month, while joint-venture production declined 8% year-on-year but surged 91% from February. Chinese brands saw output fall 5% year-on-year, though production rose 67% compared with the previous month.China's new energy passenger vehicle (NEPV) production reached 1.123 million units in March, slipping 3.8% year-on-year but jumping 74.3% from February.Over the first quarter, total NEPV output stood at 2.708 million units, down 7.6% compared with the same period last year, reflecting a slower start to the year despite the sharp monthly rebound.Retail sales of NEPVs totaled 848,000 units in March, down 14.4% year-on-year but surging 82.6% month-on-month.For the January–March period, cumulative NEPV retail volume reached 1.908 million units, marking a 21.1% decline from a year earlier, underscoring the continued pressure on consumer demand in early 2026.Despite softer sales, electrification continued to deepen. NEVs accounted for 51.5% of total PV retail sales in March, up 0.3 percentage points year-on-year and 7 percentage points higher than in February.Penetration rates varied significantly by segment. Chinese brands saw NEVs make up 73.5% of their retail sales, while the figure stood at 33.9% for luxury brands and just 6.2% for mainstream joint-venture automakers.By brand grouping, Chinese players captured 66.6% of NEPV retail sales, down 5 percentage points from a year earlier. Mainstream joint-venture brands held a modest 3.4% share, up 0.8 percentage points. Chinese NEV startups accounted for 21.5%, gaining 4.4 percentage points year-on-year, driven by companies such as Leapmotor, Li Auto, and NIO. Tesla's share came in at 6.6%, down 0.9 percentage points.Wholesale volume of NEPVs reached 1.144 million units in March, rising 1.1% year-on-year and 58.3% from the previous month.In the first quarter, NEPV wholesale volumes totaled 2.733 million units, down 4.3% year-on-year, again highlighting the uneven demand recovery.At the wholesale level, NEVs accounted for 48.1% of total PV wholesales in March, an increase of 1.3 percentage points from a year earlier.Among manufacturers, NEV penetration reached 61.7% for Chinese brands, 43.3% for luxury brands, and only 6.4% for joint-venture automakers, reflecting a widening electrification gap across the market.NEPV exports continued to surge, reaching 349,000 units in March—up 139.9% year-on-year and 29.6% from February.For the first quarter, NEPV exports totaled 908,000 units, representing a 123.7% increase compared with the same period last year, reinforcing the growing role of overseas markets in sustaining China's NEV growth momentum.