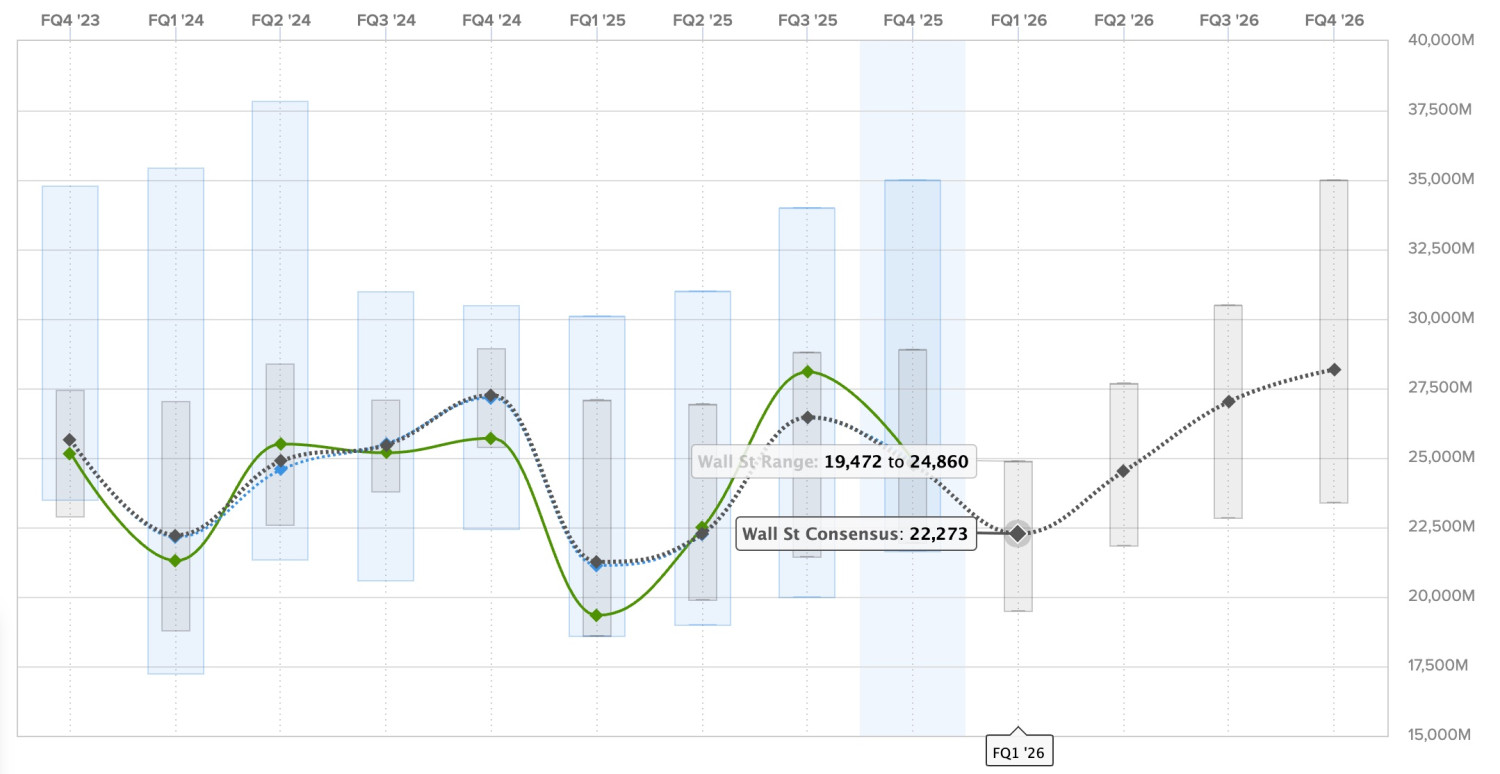

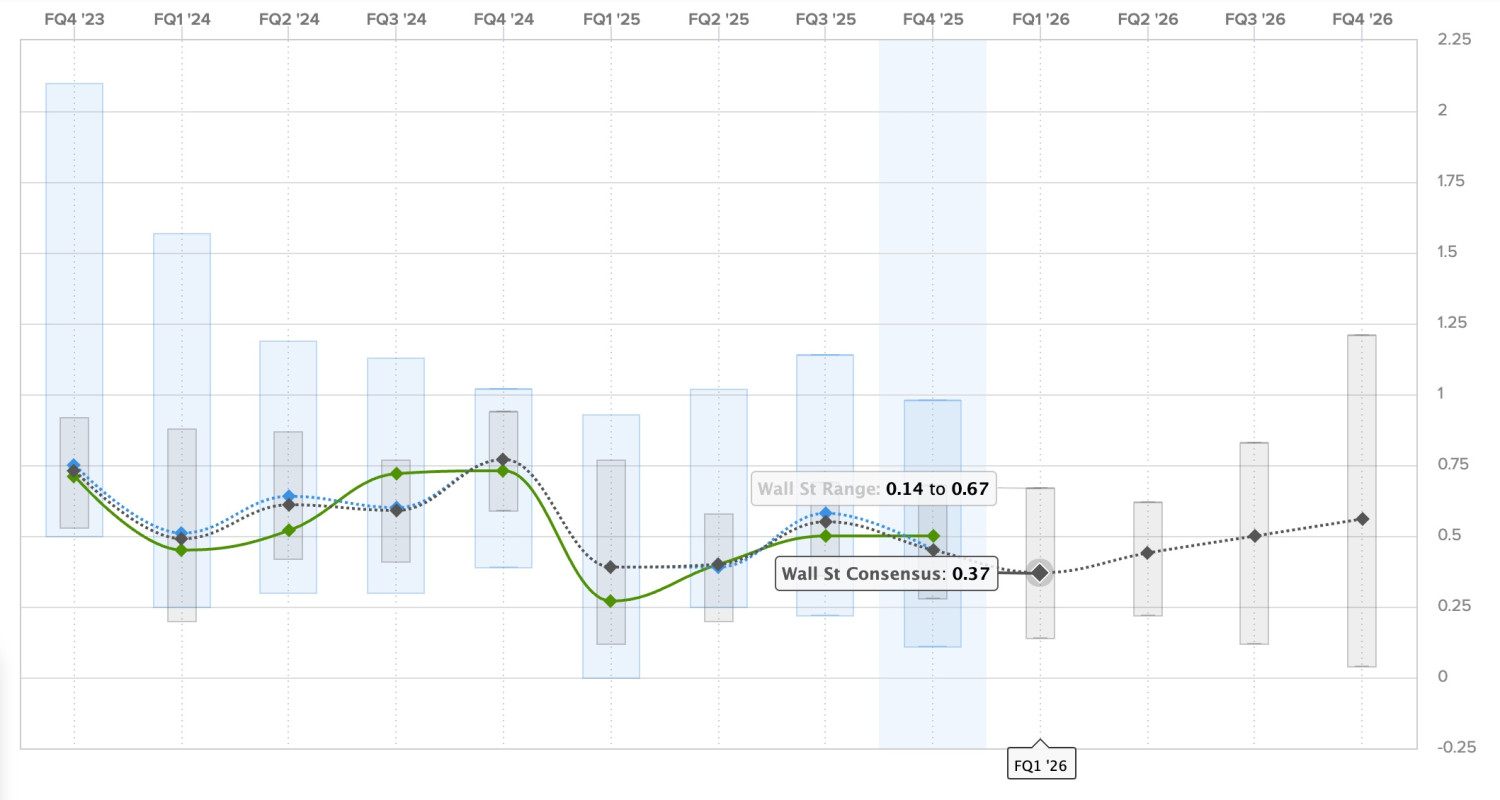

Tesla (TSLA) will release its first-quarter 2026 financial results tomorrow (April 22) after the market close, with a conference call to follow. Despite leadership continuing to push the narrative that Tesla is now an “AI and robotics company,” the automotive business still drives the vast majority of Tesla’s financial performance. Let’s look at what Wall Street and retail investors are expecting. Tesla Q1 2026 deliveries and energy deployment We already know the delivery and production numbers for the quarter: ProductionDeliveriesSubject to operating lease accountingModel 3/Y394,611341,8931%Other Models13,77516,1302%Total408,386358,0231% Tesla delivered 358,023 vehicles, missing the 365,645 consensus by roughly 7,600 units. While that’s a 6.3% year-over-year increase from Q1 2025’s 336,681 deliveries, that comparison is misleading since Q1 2025 was artificially depressed by Model Y production shutdowns across all four factories for the “Juniper” refresh. Advertisement - scroll for more content The most concerning figure is the gap between production and deliveries. Tesla produced over 50,000 more vehicles than it sold — nearly all of it in the Model 3/Y category. That kind of inventory buildup points to a demand problem, not a logistics issue. On the energy side, Tesla deployed just 8.8 GWh of energy storage — a 38% drop from Q4 2025’s record 14.2 GWh and far below the analyst consensus of roughly 12-14 GWh. Energy storage had been the one consistent growth story in Tesla’s business over the last two years, so this sequential decline is significant. Tesla Q1 2026 revenue Wall Street consensus on Estimize puts Q1 2026 revenue at approximately $22.3 billion, up roughly 14% from $19.34 billion in Q1 2025. Meanwhile, Tesla has started releasing its own company-compiled analyst consensus, which is lower at $21.4 billion. Again, the year-over-year growth looks good on paper, but it’s largely a function of comparing against Tesla’s worst quarter in years. On a sequential basis, revenue is expected to decline from Q4 2025’s $24.9 billion. The energy segment should continue to be a bright spot in terms of revenue growth, though the 38% sequential decline in deployments will likely moderate expectations going forward. Tesla Q1 2026 earnings Analysts expect non-GAAP earnings of $0.37 per share, up from $0.27 in Q1 2025 — a 33% year-over-year increase. The company-compiled consensus is significantly lower, $0.33. Automotive gross margin will be the most scrutinized metric. Margins have been under pressure from increased competition and aggressive pricing, and if the figure drops below 17%, the profitability narrative deteriorates further. For context, Tesla has beaten and missed estimates in equal measure in three of the past four quarters, with an average negative earnings surprise of 7.66%. Most upvoted Tesla shareholder questions for Q1 2026 As of this morning, Tesla shareholders have submitted 872 questions on the Say.com platform. Here are the most upvoted: 1. When will we have the Optimus v3 reveal? When will Optimus production start since we ended the Model Xand S production earlier than midyear? What’s the expected Optimus production rate exiting this year? What are the initial targeted skills? Shareholders are asking when Optimus v3 will be revealed and when production will begin, especially since Tesla ended Model S and X production earlier than expected. Tesla has been showing off Optimus at events for years, but it remains heavily reliant on teleoperation rather than autonomous function. Production timelines have been repeatedly pushed back. I expect Musk to move the goal post as per usual. 2. What milestones are you targeting for unsupervised FSD and Robotaxi expansion beyond Austin this year, and how will that drive recurring revenue? Investors want specific milestones for unsupervised FSD expansion beyond Austin and how it will drive recurring revenue. This has been the top question at nearly every Tesla earnings call for the past two years. Musk has been wrong about self-driving timelines for a decade, and I expect him to continue being wrong and moving the goal post. He will keep describing Tesla’s small pilot program in Austin, now sort of also in Dallas and Houston, as a real deployment and expansion of robotaxi. 2.B When you do expect FSD Unsupervised to reach customer cars? This is virtually the same question but more specifically about unsupervised in customer vehicles. At this point, it’s funny to me that people still believe this will happen on the current hardware. 3. How will hardware 3 cars reach unsupervised FSD? Speaking of hardware. It won’t. The answer is that it won’t. Musk said it more than a year ago at this point. Nothing changed other than him not wanting to address it. 4. Elon has posted on X about a new vehicle better than a minivan. What are the details around that? Or is it just the Model Y L? As we reported when Elon posted that, we unfortunately expect he was referring to the robovan. Hopefully not. 5. When do you expect Optimus to move from factory testing to external sales, and what revenue potential do you see from it long-term? Why even ask that? He has already said a dozen times that he expects it to be the “biggest product ever” and to bring in trillions of dollars per year. They want to hear it again? Electrek’s Take Wall Street expects Tesla to report year-over-year growth for the first time in several quarters — 13% on revenue, 33% on EPS. But nearly all of that “growth” is measured against Q1 2025, which was Tesla’s worst quarter in years due to the self-inflicted Model Y production shutdown. It’s a flattering comparison that masks the underlying trends. The data we already have is not encouraging. Deliveries missed expectations. Tesla built 50,000 more cars than it sold. Energy storage dropped 38% sequentially. Europe remains in terrible. And revenue from regulatory credits is plunging. We expect Musk will spend a significant portion of the earnings call talking about robotaxis in Dallas and Houston, and Optimus robots. These are the same talking points we’ve heard for years. What investors should focus on is whether the core automotive business can stabilize, whether energy storage rebounds in Q2, and whether Tesla has a credible plan for headwinds. Tesla investors operate as if Tesla is not facing intense competition in self-driving and humanoid robots, even as its core business is rapidly deteriorating. These earnings calls are often used by Musk to try to maintain this narrative. Stay up to date with the latest content by subscribing to Electrek on Google News. You’re reading Electrek— experts who break news about Tesla, electric vehicles, and green energy, day after day. Be sure to check out our homepage for all the latest news, and follow Electrek on Twitter, Facebook, and LinkedIn to stay in the loop. Don’t know where to start? Check out our YouTube channel for the latest reviews.