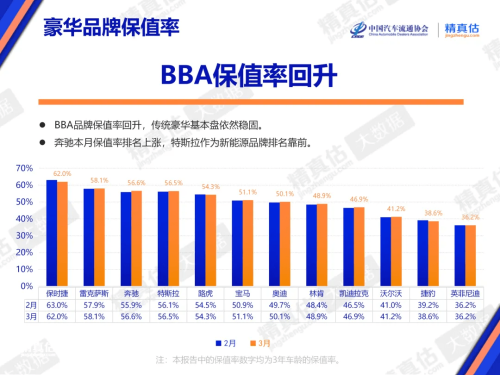

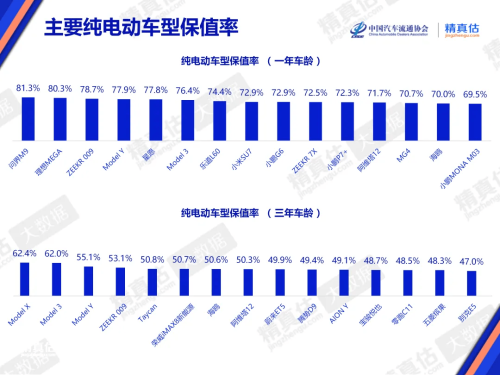

The China Automobile Dealers Association released the “China Automobile Value Retention Rate Report for March 2026”. The report indicates that following the post-Spring Festival market recovery and the full implementation of the detailed “trade-in” policy, the supply of used car sources has rebounded significantly, and the value retention rates of vehicles across all segments have generally improved. In terms of brand landscape, traditional luxury brands (BBA) and Japanese joint-venture brands have demonstrated strong risk resistance, while among Chinese independent brands, GAC Trumpchi and TANK continue to lead by leveraging their differentiated positioning. Trend in Online Vehicle Source Volume Looking at specific market supply and demand data, the online vehicle source volume reached 719,202 units in March 2026, a month-on-month increase of 27.8% from 562,614 units in February, essentially recovering to the level seen before the Spring Festival (896,433 units in December 2025). The report shows that this growth is mainly attributable to three factors: first, the full resumption of work by used car dealers after the holiday, normalizing the supply side; second, the complete rollout of local “trade-in” policy details, stimulating the release of replacement demand; and third, a significant increase in spring car usage demand, driving strong consumer enthusiasm. As the price system in the new car market stabilizes, dealer business confidence is gradually recovering, and market circulation efficiency has improved markedly. Value Retention Rates by Vehicle Segment Regarding specific market segments, the report shows that value retention rates generally rebounded across all vehicle segments in March, with the SUV sub-segment performing better overall than sedans, reflecting strong consumer demand for vehicle space practicality, multi-functionality, and off-road capability. According to the “three-year vehicle age value retention rate” ranking, mid-to-large SUVs led the market with a retention rate of 56.4%, followed by MPV models (56.2%) and mid-to-large cars (52.0%). In contrast, the retention rates for compact cars and mid-size cars were both below 50%. It is worth noting that compact cars, as the mainstay of traditional fuel vehicles, while being the most directly impacted by new energy sedans, have demonstrated strong trading activity and price recovery speed during the overall market rebound, thanks to their huge market stock and relatively low absolute price threshold. Luxury Brand Value Retention Rates Looking at specific brands, Porsche topped the list with a value retention rate of 62.0%, followed by Lexus (58.1%) and Mercedes-Benz (56.6%), with all three BBA brands seeing an increase in their retention rates. Of particular note, Tesla ranked fourth with a retention rate of 56.5%, making it the only new energy brand to enter the top tier of luxury brand value retention. In comparison, brands such as Land Rover (54.3%), BMW (51.1%), and Audi (50.1%), while remaining steady, face continuous pressure from new energy brands. In the mainstream joint-venture brand segment, Japanese brands continued to occupy the top positions in value retention. Honda (57.6%), Toyota (57.2%), and Mazda (54.9%) took the top three spots, while Volkswagen (51.9%) held a steady middle position. Value Retention Rates of Major Pure Electric Vehicle Models Among new energy independent brands, value retention rates showed mixed performance. Li Auto (51.8%), BYD (48.0%), and NIO (46.7%) all saw their retention rates improve in March. Data shows that among the main pure electric vehicle rankings in March 2026, the top three models for one-year value retention were AITO M9, Li MEGA, and ZEEKR 009. In this month’s plug-in hybrid vehicle ranking for one-year vehicle age, AITO M9, TANK 400 New Energy, and TANK 500 New Energy ranked in the top three, with Chinese independent brands continuing to show strong momentum.