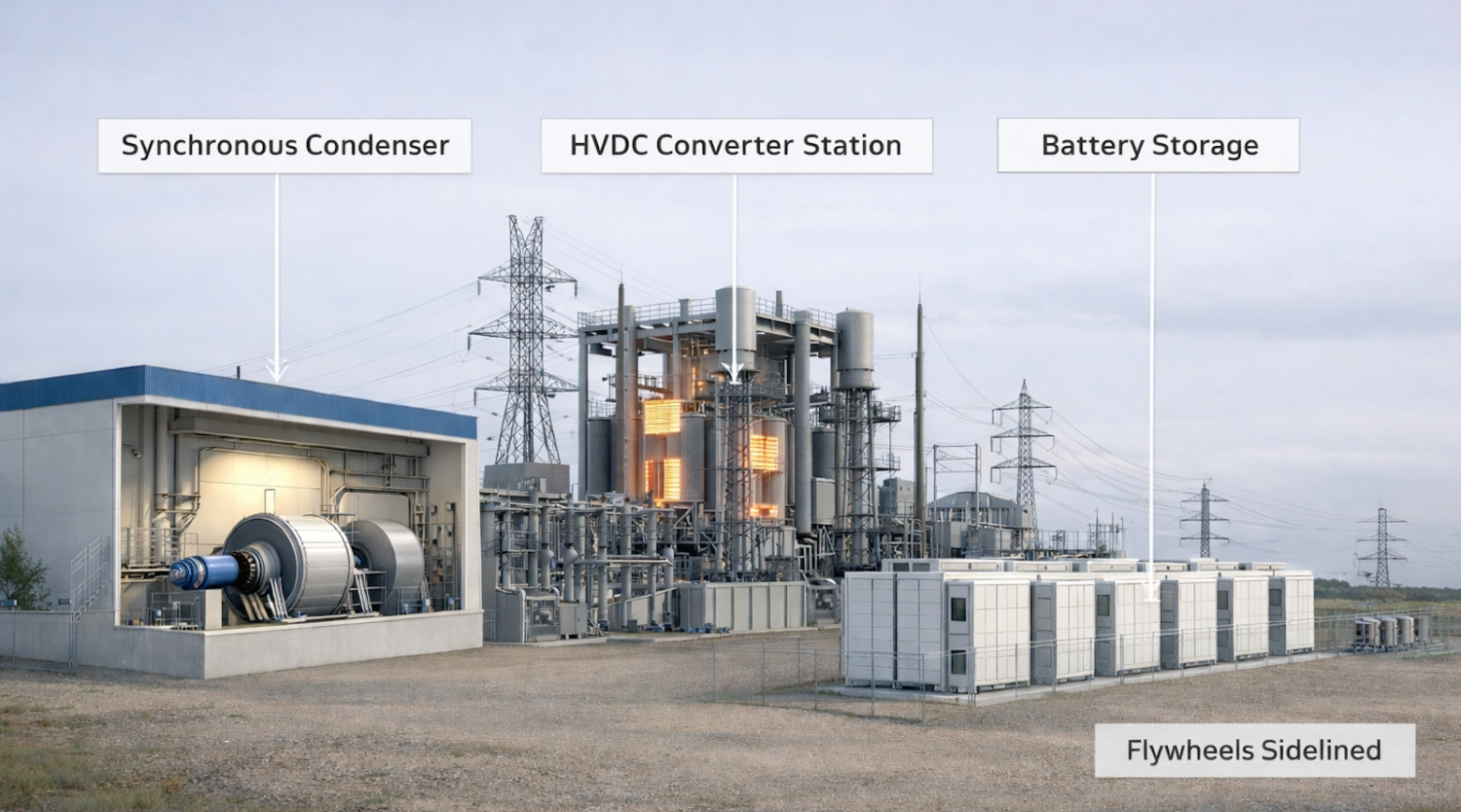

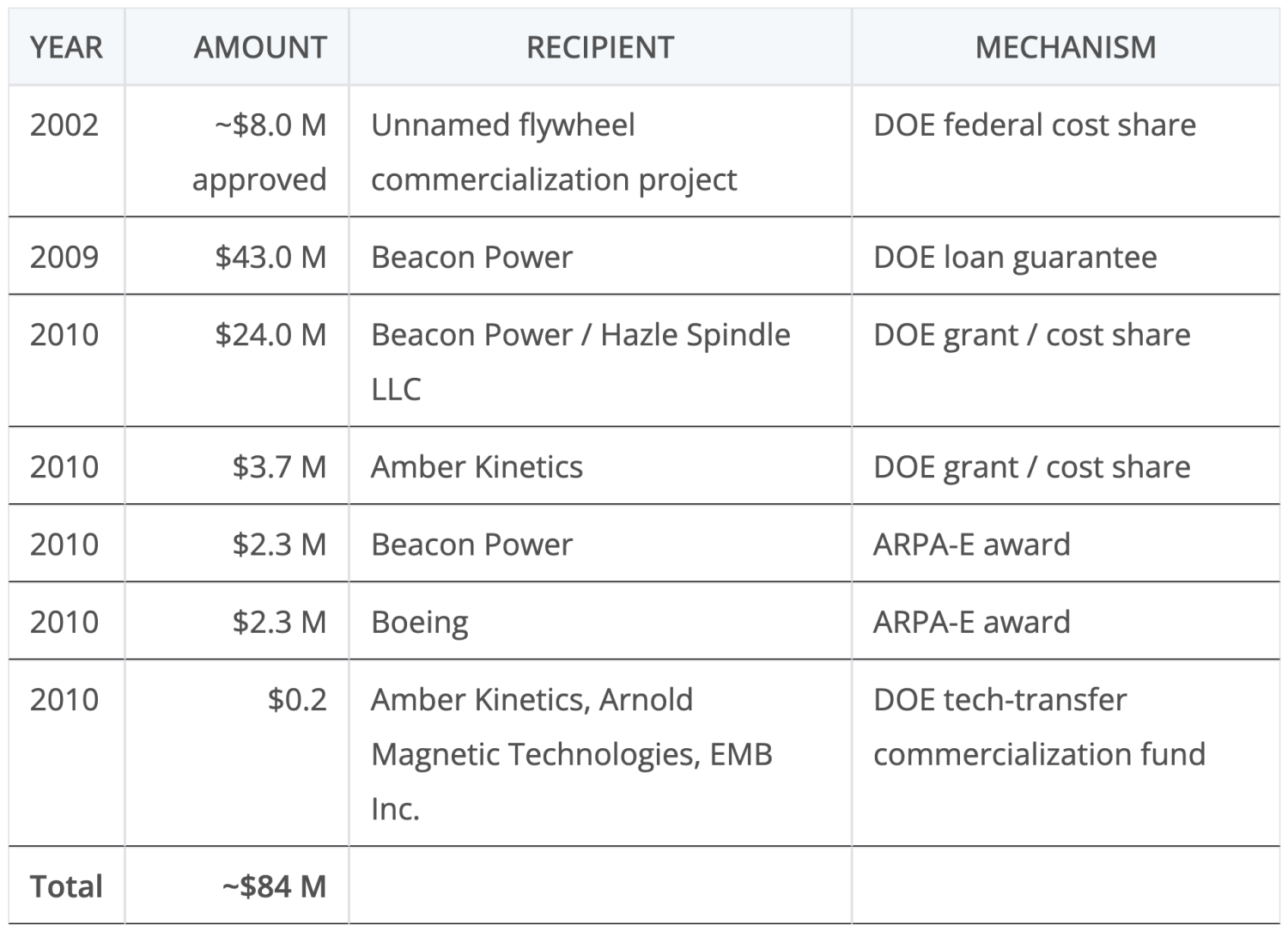

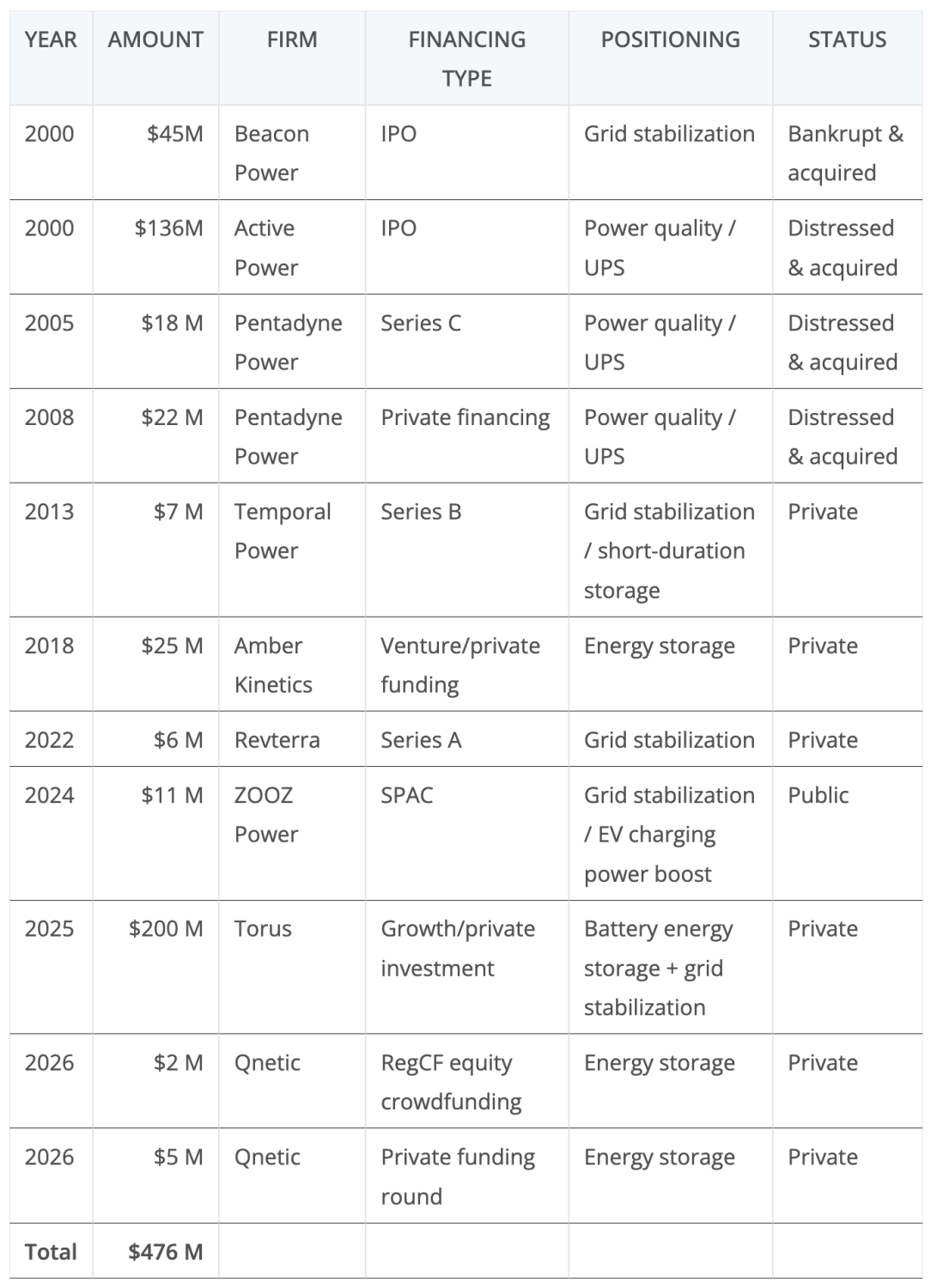

Amber Kinetics crossing my screen today was a reminder that electricity markets are littered with technologies that never quite die. Flywheels are one of those ideas. They are mechanically elegant, grounded in physics everyone understands, and they solve a real problem in principle. Store energy in a spinning mass, pull it back out through a motor generator, and avoid many of the chemical limits of batteries. They respond fast, tolerate heavy cycling, and can last for decades. That sounds attractive in a power system that increasingly values fast control, flexibility, and durability. The surprise is not that flywheels work. The surprise is that anyone is still trying to build a meaningful grid storage business around them in 2026. Table of US DOE flywheel funding for external entities, not the decades of internal research that preceded 2002, by author. That surprise fades a bit once the history is recalled. The US federal energy apparatus was funding flywheel work by the mid-1970s, well before modern battery storage existed as a serious grid category. DOE and its predecessor institutions kept returning to the technology because the appeal was real. Fast response, no combustion, no fuel, long cycle life, and a path to electrical storage that looked less constrained by electrochemistry. The long courtship culminated in the late 2000s and early 2010s when DOE put real money behind commercialization. Beacon received a $43 million loan guarantee for its Stephentown plant. Hazle Spindle received about $24.1 million in DOE support. Amber Kinetics received about $3.7 million for its California demonstration. ARPA-E added $2.25 million to Beacon and about $2.26 million to Boeing for flywheel work. Even after that push, the identifiable direct federal support was only in the tens of millions, not the hundreds of millions or billions that later flowed to lithium-ion, pumped hydro studies, hydrogen, or transmission-scale grid modernization. That federal story matters because it eliminates the lazy argument that flywheels were ignored before they could prove themselves. They were not ignored. DOE supported them for roughly 35 years before the last big commercialization wave, and close to 50 years if the early ERDA period is counted. The money side was not enormous by infrastructure standards, but it was enough to fund prototypes, demonstrations, patents, licensing, and full grid-connected projects. By 2024, though, DOE’s long-duration storage strategy assessed 10 technologies and mechanical storage in that exercise meant compressed air and pumped hydro, not flywheels. As a note, I think they are off base with compressed air storage just as they were with flywheels, and the market is bearing that out. DOE went out of its way to say that the report should not be read as formal prioritization or de-prioritization, but the portfolio choice still says a lot. When DOE looked at what might matter for 10+ hour storage and future grid scale economics, flywheels were no longer on the short list. The best case for flywheels on the grid was always Beacon Power, not Amber. Beacon’s Stephentown and Hazle Spindle plants were real utility-scale projects, each at 20 MW and 5 MWh, built around 200 flywheels rated at 100 kW and 25 kWh apiece. Those numbers are the clue. The plants were not bulk storage. They were not evening peak shifters. They were not solar soak-and-discharge assets. They were frequency-regulation plants designed to absorb and inject power very quickly to follow ISO signals. DOE’s own project material said the system could respond nearly instantaneously and much faster than traditional generators. That was the niche. In the early 2010s, when pay-for-performance regulation markets briefly rewarded speed and precision, flywheels had a plausible commercial opening. Even there, the story was narrower and messier than the sales pitch. Stephentown cost about $69 million. Hazle came in at about $53 million, which DOE described as a 38% cost reduction from the first plant. That still meant Hazle cost around $10,600 per kWh of stored energy, because 5 MWh is only 5,000 kWh. That number is not a typo. It looks absurd because frequency-regulation plants are really power-and-control assets with a sliver of energy behind them. Beacon’s business was not storing a lot of electricity cheaply. It was selling fast correction services into a market window. When that window narrowed and the company’s finances broke, Beacon filed for Chapter 11 in 2011. Rockland Capital picked up the assets in 2012, completed Hazle using the already awarded DOE support and additional equity, and eventually sold the flywheel plants to Convergent. The hardware worked. The business did not. Amber Kinetics is the contemporary version of a different ambition. Instead of selling seconds or minutes of response, Amber has spent years pitching four-hour flywheel storage. Its commercial M32 unit is rated at 8 kW and 32 kWh. On paper that sounds like a graduation into mainstream storage. In practice it highlights the scale problem. Thirty-two kWh is 0.032 MWh. A single modern 4-hour battery container sits in the 4 to 6 MWh range, with the frontier already pushing beyond that. One 3.9 MWh Megapack-class enclosure holds about 122 Amber M32 units worth of energy. A 5 MWh container is roughly 156 Amber units. A 100 MWh battery project would need about 3,125 M32-equivalent units to match it on stored energy. That is before talking about balance of plant, controls, foundations, maintenance, and site integration. Amber’s four-hour claim matters technically. Commercially, the module size is a confession. Table of private money that’s visible in flywheel firms, by author. The financing trail says much the same thing. Flywheels attracted real private capital, but the pattern was not durable confidence in a growing category. Beacon raised $44.6 million in its 2000 IPO. Active Power raised $136 million, but that was a UPS and power-quality story more than a grid-storage one. Pentadyne raised $18 million in a Series C and another $22 million later, again around UPS applications. Temporal Power raised C$10 million in 2013 for short-duration grid balancing. Revterra raised $6 million in 2022 for a grid-stabilizing kinetic battery. Amber sits in the murky middle with public databases showing $25 million or $47 million depending on the source, which is itself revealing for a 17-year-old company. The largest recent number in the flywheel neighborhood is Torus at $200 million in 2025, but Torus is not a pure flywheel company. It is a battery heavy, flywheels on the side story. Qnetic raised $2.1 million through crowdfunding and then $5 million more in 2026 for longer-duration flywheel systems. ZOOZ reached public markets by SPAC, not a traditional IPO, and its minimum net proceeds at closing were about $10.9 million. None of that looks like a sector on the edge of scale. It looks like a sector surviving on niches, hybrids, and investor patience. The fate of the better-known firms is even more instructive. Beacon ended in bankruptcy before its assets were rescued. Pentadyne was effectively liquidated through an assignment process rather than a formal Chapter 11. Active Power was acquired in a distressed sale before the remaining corporate shell later went through bankruptcy. The history is not one of repeated triumphs obscured by bad luck. It is one of repeated failure to establish a large and durable commercial category. That does not mean the engineering was bad. It means the market problem was narrower than the companies hoped, and the alternatives kept getting better. That last point is the heart of the problem. Flywheels did not lose to one rival. They lost to a swarm of rivals, each better suited to a specific service. For mainstream energy shifting, lithium-ion batteries won on cost, scale, and packaging. NREL’s recent work shows 4-hour utility battery system costs in a range centered far below the effective cost basis of historic flywheel projects, while market evidence keeps pointing to rapid deployment at tens of GWh per year in the United States alone. For long-duration mechanical storage, pumped hydro and compressed air remained the main DOE reference points. For inertia, system strength, fault current, and voltage support, synchronous condensers and repurposed spinning machines from retired thermal or hydro plants remain more natural fits. For cross-border balancing and fast active power support, modern HVDC and inverter-based resources are now expected to respond without intentional delay, often in the sub-second range. Flywheels were once able to claim speed as a category advantage. In 2026 that is no longer much of an advantage because batteries, advanced inverters, and HVDC controls are already fast enough for the services that matter. This is why comparisons to synchronous condensers and Dinorwig matter. A synchronous condenser is a large grid-connected rotating machine that is kept spinning to provide inertia, voltage support, reactive power, and fault current to stabilize the grid. A high-speed flywheel also stores energy in rotation, but it is a much smaller, faster device built mainly for short-duration power injection and absorption, not for the broad system-strength and protection services that synchronous condensers provide. A synchronous condenser is not an energy storage plant, but it is often the right answer for stability services that venture-backed flywheel firms tried to wrap into the term grid balancing. Basically, flywheels tried to provide similar services by replacing mass with speed. It provides inertia, short-circuit strength, and voltage control in a form grid operators understand well. It’s old tech, not disruptive tech and doesn’t have a disruptive tech price tag expectations. The first award when the United Kingdom’s inertia market came on line was a synchronous condenser from ABB. The Dinorwig pumped hydro facility in Wales is another category altogether. It can deliver 1,728 MW and do so in seconds, with roughly 5 hours of duration. Hazle’s 20 MW and 5 MWh flywheel plant is not even playing the same sport. Dinorwig has about 86 times the power and around 1,700 times the stored energy. Once the comparison is framed honestly, it becomes hard to argue that flywheels were ever general grid-balancing platforms. They were specialist regulation devices operating in a narrow market niche. One of the more practical answers to the stability services once wrapped into the flywheel pitch is repurposing existing thermal generation units as electrically powered inertia machines, synchronous condensers. Instead of burning fuel and exporting net electricity, the retired plant’s generator is kept spinning with a small electrical input, allowing it to provide real physical inertia, voltage support, reactive power, and short-circuit strength to the grid. That matters because inverter-based resources and batteries can imitate some grid services, but they still do not fully replace the protection-quality fault current and synchronous inertia that large rotating machines provide. Where the generator, shaft train, foundations, switchyard, and grid connection already exist, conversion can be cheaper and faster than building new synchronous condensers from scratch, especially for coal and gas sites that are already well located in the transmission system. It is not free money, because clutches, drives, cooling systems, controls, and refurbishment still cost real capital, and old machinery may have limited remaining life. But as a way to preserve useful grid services from retiring thermal assets, it is often a far more grounded proposition than trying to sell ultra-high speed flywheels as a broad grid-balancing solution. There is another constraint that got less attention in the early enthusiasm and more in later DOE material. Safety for flywheels is a mechanical problem. DOE’s 2024 safety strategy states that flywheels are not generally attractive for large-scale grid support services requiring many kWh or MWh because of cost, safety, and space requirements. The most prominent safety issue is rotor failure while rotating. In a large steel rotor, a crack can propagate and release large pieces at high speed, which means containment engineering matters a lot. This is not thermal runaway. It is not a battery fire story. It is a very fast moving steel story. Amber’s response is to stress that its M32 is 98% steel by weight, cannot burn, and is designed around rotor integrity and containment. That may all be true. It also reinforces the point that the scaling problem for flywheels is not only economics. It is economics tangled with physics and containment. If there is still a real niche for flywheels, it is much smaller and more specific than the grid-storage narrative suggests. While Sandia’s flywheel safety and applications material points to transit regenerative braking as one of the clearer remaining opportunities, the reality of trains is much more focused on batteries. Flywheels remain scattered demonstrations and pilots, not scaled solutions. Rotary UPS is one of the few niches where flywheels are not just plausible but clearly deployed. The fit is straightforward. These sites usually need seconds to a few minutes of ride-through, not hours of storage, and they need it with high reliability, repeated cycling capability, and fast response to brief grid disturbances. In that role, a spinning machine can be a better fit than oversized chemical storage, especially where operators care more about power quality, uptime, and maintenance predictability than about shifting large amounts of energy. Piller, for example, says a major global bank has operated eight flywheel-backed UNIBLOCK units totaling 17.2 MVA since 2012 and is doubling that system to 34.4 MVA, while Active Power points to Parkland Hospital’s deployment of 10 CleanSource UPS systems totaling 29 flywheels to support critical operations. It is a real market. It is just a critical-power market, not the basis for a large grid-storage sector. That is why the surviving firms do not inspire much confidence. Amber is still private after being founded in 2009, with module sizes that are tiny by modern storage standards and a public funding record that looks modest for a hardware company trying to create a new infrastructure category. Further, the publicly stated installed based and 2 GWh returned electricity, even at the $1,500/kWh price Amber acknowledged years ago would only amount to $1.65 million to $2.75 million in lifetime revenue. It’s been living on investor money, grants and loans, not sales. Its chairman, Luis Virata, is a prominent deal broker in Indonesia, but Amber is clearly not his focus. Nor is it the focus of US Secretary of Commerce Howard Lutnick, who disclosed between $1 and $5 million in investment in Amber through a family trust in 2025. I suspect they’ll both lose whatever money they have in the firm. Revterra is still small. Qnetic is at the pilot-money stage. Torus only looks large because it is not making a pure flywheel bet, but a battery-heavy bet with a side helping of flywheels. ZOOZ is public, but in a narrow power-boost and EV charging role that sits closer to power quality than to mainstream grid storage. This is not a field full of breakout contenders. It is a field of specialists, survivors, and hybrids trying to hold on to corners of the map that batteries, condensers, hydro, and power electronics have not already taken. The fairest conclusion is not that flywheels were foolish. They were not. The engineering proposition was always interesting, and in narrow use cases it still is. The lesson is harsher than that. A technology can be elegant, durable, and physically sound, receive federal support over decades, attract public and private capital, solve a real operational problem, and still fail to become important to the grid. Flywheels never lacked for physics. For a while they did not lack for funding either. What they lacked was a large, durable electricity market need that other technologies did not solve more cheaply, more simply, or at much greater scale. That is why they remain alive at the edges and absent from the center.