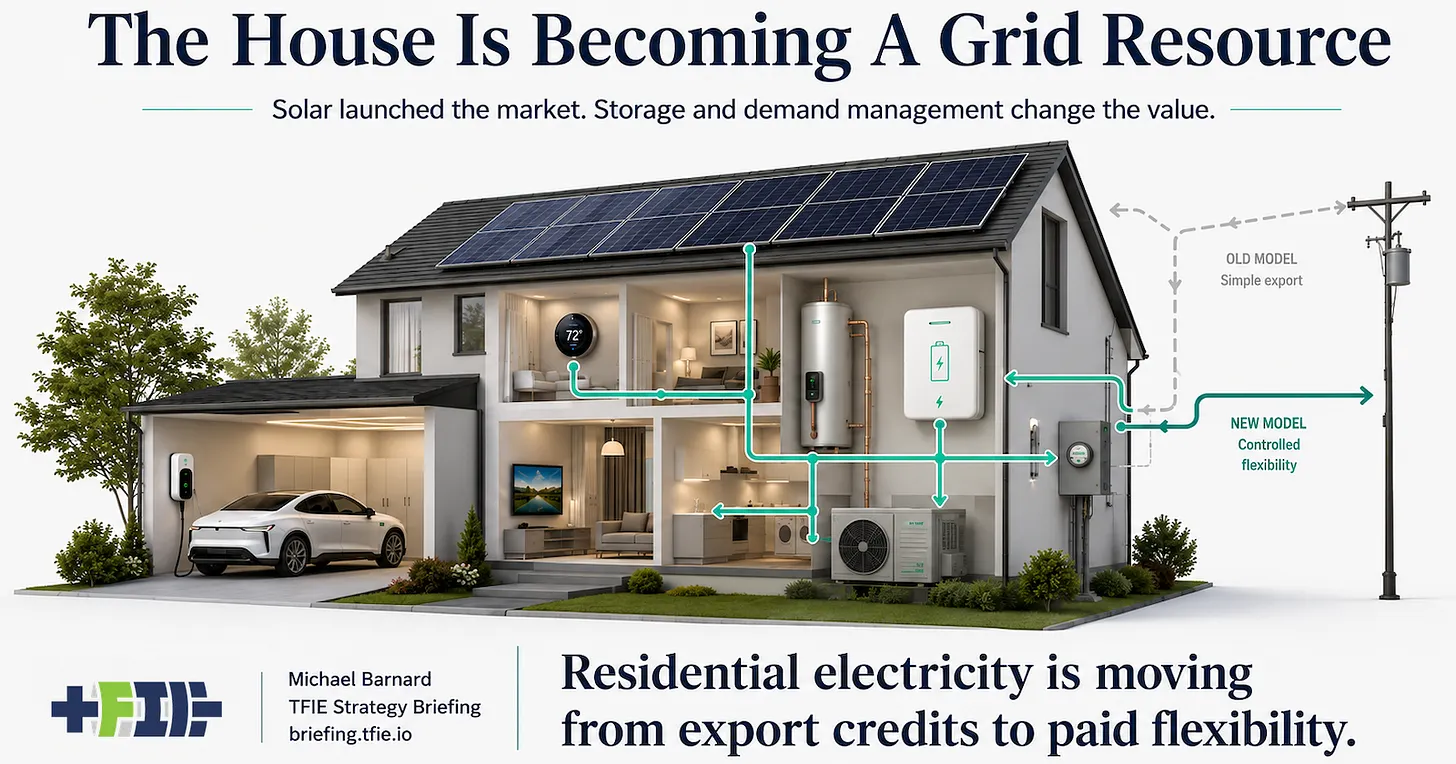

BC Hydro’s change to net metering looks, at first glance, like another rooftop solar fight. The old Rate Schedule 1289 is closing to new customers on July 1, 2026, and new self-generation customers will move to Rate Schedule 2289, where excess generation is paid at 10¢/kWh in the billing cycle instead of being banked as future kWh credits. Existing net-metering customers get a transition period, and BC Hydro has also created a community generation option. That is the local tariff story. The larger electricity-system story is that residential compensation is moving from passive export credits toward paid flexibility. Net metering was useful because it made rooftop solar simple enough to sell, finance, install and interconnect. A household could understand the proposition, an installer could build a business around it, lenders could underwrite it, and utilities could learn how to connect small systems without turning every rooftop into a bespoke regulatory exercise. At low penetration, retail net metering was a reasonable early-market bargain in developed countries. It helped launch markets that would otherwise have been slowed by transaction costs and uncertainty. The problem is treating that launch policy as the end-state. Annual kWh banking was tolerable when adoption was small and feeders were not under much stress. It becomes harder to defend once rooftop solar penetration rises, distribution constraints appear, batteries arrive, EVs become flexible loads, and utilities need customers to help with timing rather than merely settling up once a year. That does not mean every attack on net metering is justified. The cost-shift argument is real, but it is often overstated at low penetration. NREL’s 2025 review is useful because it keeps the issue in proportion: below 3% household PV deployment, net metering was unlikely to increase non-solar customer bills by more than $1 per month, and even between 3% and 7% deployment the estimated impact was still below $1 per month in two-thirds of states. California and Hawaii were the cautionary cases because high penetration and particular rate structures made the issue materially larger. Reforming too late creates entitlement politics, but reforming too early can turn a small accounting issue into a large solar-market fight. BC Hydro’s move should be read as part of a policy transition pathway, not as a simple rooftop-solar fairness dispute. The useful test is whether households and small customers are being paid for services they actually provide. Passive surplus electricity is one service. Self-consumption is another. Load shifting, battery discharge, EV charging control, water-heater flexibility, thermostat response and community generation are others. In California after the move from old net energy metering to the Net Billing Tariff, Lawrence Berkeley Lab found that storage attachment rates jumped from roughly 10% under the old regime to about 60% under the new one. That is the expected technical mechanism: lower export value pushes the market toward self-consumption and storage. But it also changes installer economics, financing assumptions and customer paybacks quickly. Net billing can point in the right direction and still arrive as a value cut rather than as a visibly better compensation offer. South Australia points more clearly toward the operational endpoint. SA Power Networks’ flexible export model lets compatible inverters export up to 10 kW per phase when the network can accept power, while dynamically turning exports down when there is too much energy on the grid. That treats export access as a network service with operating limits, not as a permanent right to send every surplus kWh into the system at a flat value. That is where demand response belongs in the story. The destination is paid useful electricity services. Households should be able to use their own solar, export when useful, shift EV charging away from peaks, let water heaters or thermostats respond within comfort limits, dispatch batteries when the grid actually needs them, and get paid for the service delivered. Customers should not have to become power traders. The offer should be simple, even if the market, utility and software systems behind it are complex. The international lesson is that the same distributed-energy technology creates different policy problems in different systems. Mature grids can let early generous rules become politically durable before the off-ramp is written. Fragile utilities can lose high-paying customers to self-generation while fixed network costs remain. Access-deficit systems may need reliable electricity for productive uses long before export-tariff design becomes the main issue. The same rooftop panel, battery or EV charger can solve different problems depending on the grid around it, so the compensation rule should follow the system problem. Pakistan is a useful reminder that distributed solar can move faster than official systems can measure. Customers did not wait for a finished distributed-energy regulatory architecture. Factories, commercial buildings and households installed solar because electricity was expensive and unreliable. Cheap Chinese hardware, weak service quality and immediate reliability needs created the market before institutions knew how to classify it. BC Hydro’s new rate is directionally consistent with the global move away from annual kWh banking, but it is only the first move. A flat 10¢/kWh export payment is a tariff correction, not a full residential flexibility strategy. The next question is whether BC Hydro, regulators and other utilities build the rest of the stack: seasonal and time-sensitive value, managed EV charging, water-heater control, battery dispatch, community generation, local flexibility and dynamic export access where feeders need it. Read the full TFIE Strategy Briefing analysis for the grid-type matrix, international comparators and policy triggers behind the shift from net metering to paid flexibility: Net Metering Is Not The End-State.