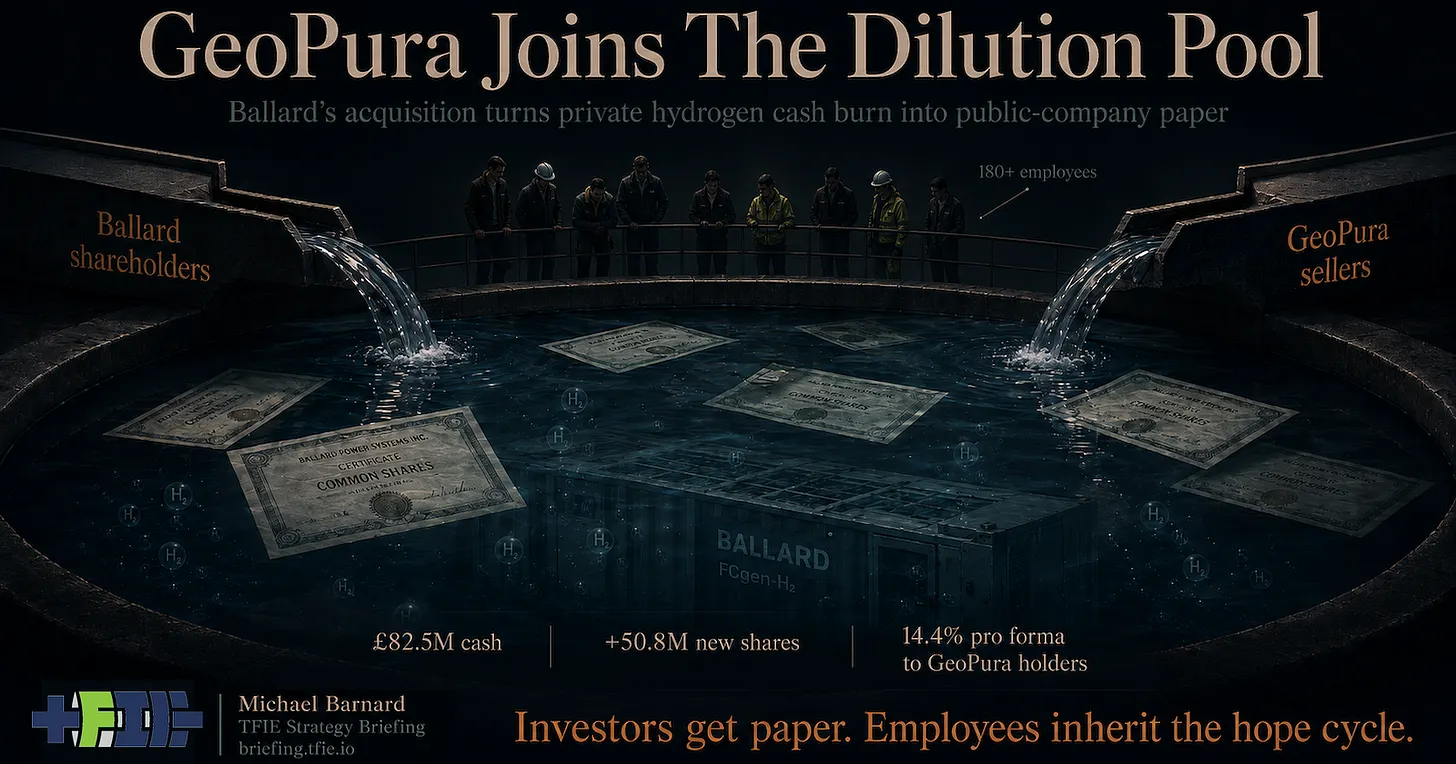

Perpetual loss-making hydrogen fuel cell firm Ballard Power is paying £275 million for GeoPura, but only £82.5 million is cash. Most of the price is 50.8 million newly issued and dilutive Ballard shares, leaving GeoPura’s investors with about 14.4% of the combined company and subjecting much of their consideration to post-closing lock-ups. That looks less like a strong strategic buyer acquiring a profitable growth platform than a capital-hungry private hydrogen company accepting the least-bad exit available. Ballard’s acquisition announcement presents the deal as a transformation into an integrated hydrogen ecosystem provider. The company will move beyond fuel-cell power modules into hydrogen production, storage, distribution, refuelling, logistics and deployed power services. That makes the investor presentation broader and more tangible, but it does not change the denominator: most of the purchase price is dilutive Ballard paper with its history of terrible stock performance. The share price is already down substantially from the announcement of the deal. Ballard full stock price history A clean strategic exit converts years of private-company risk into cash or highly credible acquisition currency. This transaction converts most of GeoPura’s risk into continued exposure to Ballard’s losses, financing requirements and future dilution. The deal terms suggest that GeoPura’s investors had limited attractive alternatives: another private raise, more asset-backed debt, a down round, slower expansion, a much narrower strategy or a buyer unwilling to pay primarily in cash. GeoPura has real equipment, customers, employees and operational experience. Its hydrogen power units have been deployed at construction sites, film productions, events, hospitals, military facilities, data centres and sites where grid capacity is constrained. Replacing diesel generators is one of the more defensible hydrogen-for-energy applications because diesel units are noisy, polluting and increasingly awkward for organizations with public climate commitments. The relevant comparator, however, is no longer just diesel. GeoPura competes directly with mobile and stationary battery systems that store electricity and return it through power electronics without first producing hydrogen, compressing or storing it, moving it by tube trailer and converting it back into electricity through a fuel cell. Hydrogen adds more equipment, more energy losses, more maintenance and an ongoing fuel-delivery obligation. Batteries do not cover every temporary-power requirement. Long-duration operation, charging access, weight, site constraints and some industry regulations can leave gaps where hydrogen or another fuel-based system may be useful. GeoPura found real customers in some of those gaps. But its addressable market is being squeezed as battery costs fall, mobile storage services expand and customers gain more ways to combine batteries, temporary grid connections and limited backup generation. GeoPura’s financing history shows that the operating niche was not supporting the growth story. The company raised £36 million, followed by £56 million and then £22 million of asset-backed debt, for approximately £114 million of financing over two years. At the same time, its chief financial officer discussed an ambition to reach 3,600 hydrogen power units, requiring more than £2.5 billion of capital over the following decade. Ballard’s transaction presentation describes a current operating base of more than 60 hydrogen power units, about 20 electrolyzers, 75 tube trailers, 150 manifolded cylinder packs, more than 180 employees and expected 2026 revenue of approximately £38 million. Those are meaningful assets and revenues, but they are small beside a 3,600-unit ambition and a £2.5 billion capital requirement. GeoPura was losing money and relying on external financing while competing against a technology whose system economics are improving more quickly. The numbers are also small against Ballard’s ongoing annual losses, which have added up to almost $2 billion of other people’s money since 2000. The best comparisons for the business Ballard is entering into are FuelCell Energy and Plug Power, vertically integrated hydrogen for energy services companies which have the distinction of having lost even more money than Ballard has while never turning a profit. The acquisition therefore does not look like a profitable platform choosing the strongest strategic partner from a position of strength. It looks like a private hydrogen company whose next financing round had become the central problem, with Ballard offering an exit that included enough cash to be acceptable and enough shares to avoid placing the full burden on Ballard’s balance sheet immediately. Ballard is not an obviously strong buyer. Its recurring financial pattern has been to raise capital during hydrogen enthusiasm cycles, fund continuing operating losses and return to investors when another market narrative creates a new financing window. The applications have moved through cars, buses, trucks, trains, ships, stationary generation, resilience, data centres and energy-as-a-service. The markets change, but dilution of investor equity keeps happening as losses mount. The value to Ballard is investor-friendly marketing attached to a real but loss-making operating business. Ballard can point to hydrogen production, storage, tube trailers, deployed assets and customers while arguing that integration will improve control, capture more value and expand the addressable market. The industrial overlap also predates the transaction. Ballard already supplied fuel-cell power modules to GeoPura. Buying the company does not create that relationship; it internalizes it and moves much more of the system boundary onto Ballard’s balance sheet. Hydrogen production, compression, storage, transport, refuelling, utilization, uptime, maintenance, site logistics and customer operations now become more directly Ballard’s problems. That could make the combined offer more defensible if Ballard can improve utilization, lower delivered hydrogen costs and operate the system reliably. It also removes many of the excuses available to a component supplier. When a fuel-cell module fails to produce a profitable market, the supplier can point to fuel prices, infrastructure gaps, vehicle manufacturers, project developers or customers. An integrated company owns more of the commercial result. The broader system-boundary problem is examined in The Hydrogen Bit Isn’t The Product, which examines the implosion of hydrogen energy services firm CPH2 after its MW-scale, no membrane electrolyzer blew up. Selling the attractive component while leaving production, logistics, maintenance and customer operations to others can sustain an investment story for years. Taking those functions inside makes the company more substantial, but it also exposes the capital intensity and operating burden that the component story left outside. GeoPura founder Andrew Cunningham is expected to become Ballard’s president, reporting to chief executive Marty Neese. Ballard gains the executive associated with GeoPura’s operational credibility, while customers and employees retain some continuity. Cunningham also inherits responsibility for demonstrating that the acquired business can justify the shares issued to buy it. The greatest exposure sits below the executive level. GeoPura’s more than 180 employees include engineers, technicians, logistics staff, operators, apprentices and commercial personnel who have built equipment and delivered projects. When utilization disappoints, hydrogen costs remain high, battery competition intensifies and Ballard requires another financing round, the consequences will appear in cancelled expansion, reduced support functions and eventually headcount. This is what hydrogen dilution cycles obscure. The losses do not remain inside financial statements, and the risks do not end with shareholders. Companies recruit technically capable people into growth plans that depend on the next round of capital arriving before the previous round is consumed. When the economics fail to mature, real human beings lose their jobs. The GeoPura transaction compresses that financing cycle into one deal. Its investors receive £82.5 million in cash and mostly locked Ballard shares. Existing Ballard shareholders are diluted. Ballard receives a wider total addressable market and a more credible operating narrative. GeoPura’s employees inherit the task of making the combination work against expensive hydrogen, demanding utilization requirements and steadily improving battery competition. Read the full TFIE Strategy Briefing analysis for the seller-side diligence, battery competition, operating-system boundary and employees carrying the risk.