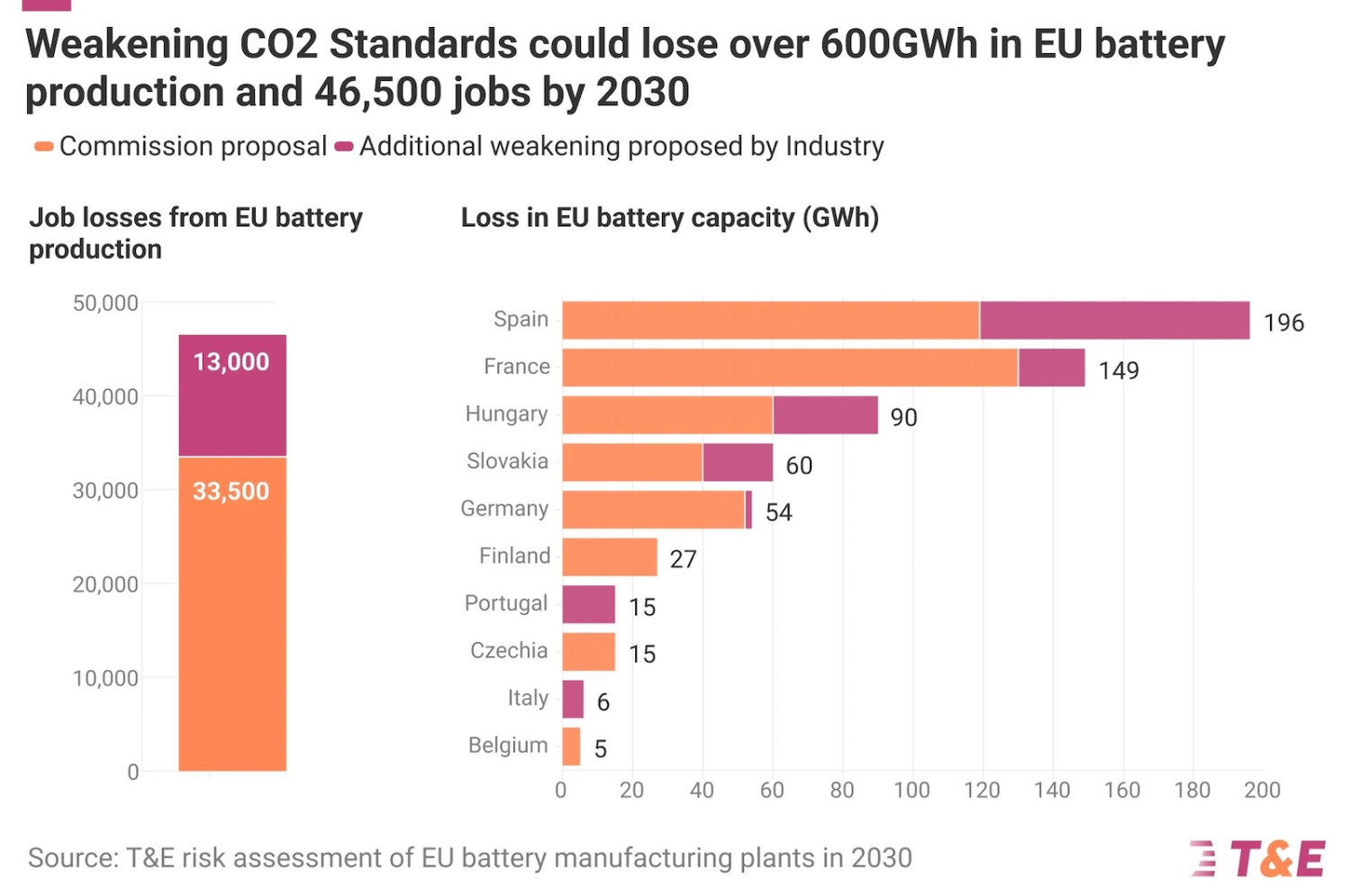

As the global auto industry rapidly shifts toward EVs, new analysis warns that Europe risks forfeiting a major industrial opportunity. Scaling back EU car climate rules would put a potential 34 Northvolt-sized battery factories at risk. That’s according to a new T&E report which models the ‘industrial opportunity cost’ of weakening EU car CO2 targets as carmakers demand. That scenario could see electric car (BEV) production halved in 2030 compared to today’s projections, while the bloc would spend an extra €50 billion on oil imports than under the current CO2 rules. BEVs are now the primary driver of global auto industry investment, and in the EU the CO2 targets determine the speed of the shift to electric. The report assessed three scenarios — the current EU regulation, the EU Commission proposal to weaken it, and the auto industry’s demands [1] — and found that scaling back targets would carry substantial industrial costs. Potential BEV production in the EU could halve to 3.7 million units in 2030, the report finds. That’s if the car industry’s demand to average the 2030 EU target over five years is met. Weakening the 2035 emissions target, as ACEA also calls for, would cut expected BEV production by 46% in that year. Just as the EU is proposing industrial policies to shore up its battery industry, its move to cut EV targets would see local battery offtake dwindle. Potential battery production capacity could shrink by more than two-thirds in 2030 — equivalent to losing 34 potential Northvolt-sized factories and up to 47,000 jobs, the report estimates. Julia Poliscanova, senior director for vehicles and emobility supply chains at T&E, said: “From China to Chile, EVs are now the growth engine of the global automotive industry. If Europe anchors EV manufacturing within its borders, it can be at the forefront of building a new cleantech industrial base. But if Europe weakens car climate targets, China will move even further ahead and the EU risks losing its nascent battery and EV industries through strategic hesitation.” Weak targets would undermine the entire battery value chain. The report finds that local manufacturing of cathodes, the most valuable component of a battery, could cover over two-thirds of Europe’s needs by 2030 — if strong car CO2 rules are in place. But if the auto industry’s amendments go ahead, only five cathode projects are likely to be realised, covering just over 10% of the projected 2030 demand. The reduced EV uptake as a result of weaker car CO2 targets could cost the EU €50 billion in additional oil import costs between 2026 and 2035. That is compared to a scenario where the current law is maintained and the bloc avoids more than 2 billion barrels of oil consumption by 2035. In contrast, if a strong local BEV market is in place, Europe’s dependency on battery imports could be as low as 7% due to increased domestic production and recycling. EU lawmakers are currently debating the Commission’s proposal to weaken car CO2 targets. T&E called on MEPs and governments to reject any weakening of the 2030 goal — including by ‘averaging’ it over multiple years. It said the 100% zero-emission cars target in 2035 and ambitious Made-in-EU requirements are needed to help build a European battery industry. Note to editors: [1] The industry scenario assumes an -80% CO2 reduction target in 2035 (instead of -100%), a five-year average period for the 2030 CO2 target, and a broadening of the scope of super-credits. See full report.