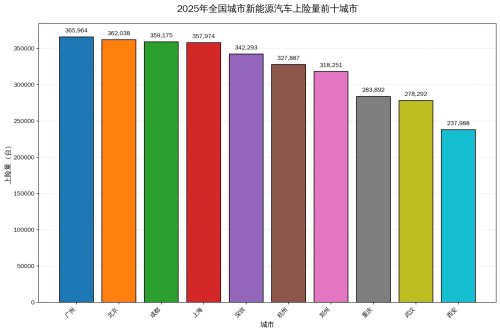

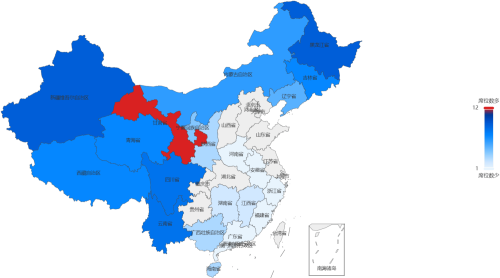

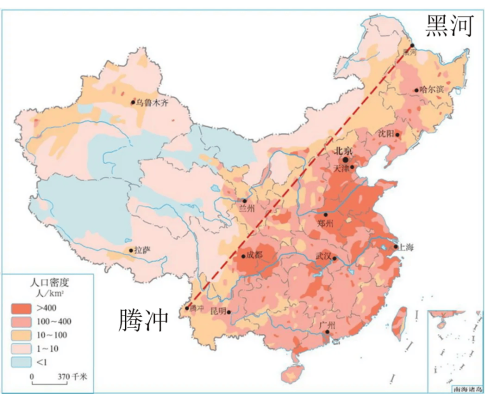

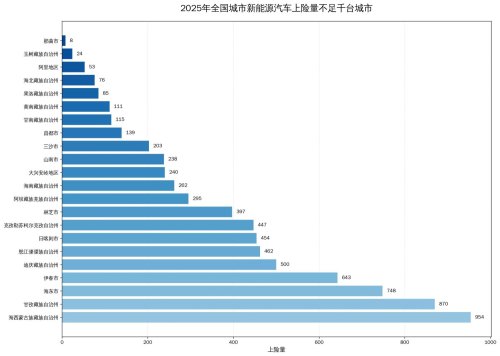

In 2025, China’s new energy vehicle penetration rate exceeded 54%, but regional distribution was highly uneven. High-altitude, frigid, and sparsely populated areas became market “dead zones”. Such gaps may persist long-term, marking the industry’s maturation. A city with a permanent population of 514,300 sold only 8 new energy vehicles (NEVs) throughout 2025. Known as the “Northern Gateway” of Tibet, Naqu City had the lowest NEV insurance registration volume in China in 2025. In the same year, Guangzhou, which ranked first in national NEV insurance registration volume, sold 365,964 units—45,745.5 times that of Naqu. The number “8” may not even be as many as the single-day orders of a popular NEV store in Guangzhou. Whether it is the statistics of the top 10 or 20 cities with the best sales of various brands/models released by third-party institutions, or the best-selling cities mentioned by car companies, people’s attention is always focused on cities/provinces such as Beijing, Shanghai, Guangdong, Zhejiang, and Jiangsu. Many other cities outside these regions have little chance of making the list. Naqu is undoubtedly an extreme case, but when the annual NEV penetration rate exceeded 54% in 2025, entering the mainstream public stage, it may be time for us to shift our attention to the “dead zones” of NEV sales and think about the possibility of further development of NEVs. Why are NEV sales in these cities insignificant? Can the “dead zones” of China’s new energy vehicle industry really be eliminated? At least for the second question, we can give an answer first: No, not in the short term. Where is Naqu? Open a map, look north of Tibet, and upstream of the Nu River, and you will find Naqu. In 2024, ChinaEVHome followed the smart team to conduct plateau tests on the smart #5. Like many tourists, we noticed a phenomenon that seemed novel to residents in eastern China: there were almost no trees in downtown Naqu. Roughly and conservatively speaking, this city located on the northern Tibetan Plateau has an average altitude of over 4,500 meters, making it the prefecture-level city with the highest altitude in China. A Tibetan proverb—”Far in Ali, bitter in Naqu”—directly points out its harsh natural conditions. It was not until the past two years, with the joint efforts of various investments and incentive measures, that Naqu’s history of having no trees was completely ended. Even so, the maintenance and planting of green belts in Naqu in winter remain a key part of the city’s public affairs. Even photos taken by Guangming Daily show that this work is promoted with signs at the end of the green belts. Extreme cold and thin air have created the harshest ecological landscape in Naqu. Naturally, they have also set a natural barrier for NEVs in this city, which has a permanent population of 514,300 and an area of 451,000 square kilometers, resulting in only 8 NEVs being registered for insurance in 2025. In stark contrast is Guangzhou, located in the warm and humid southeastern part of China, which topped the 2025 national NEV insurance registration list with 365,964 units sold. The two poles of this coordinate axis are clearly projected on China’s territory. Above these two coordinate points are completely different levels of popularity in the NEV market. Two Ends of the Rope In 2025, the national NEV insurance registration volume in China (excluding Hong Kong, Macao, and Taiwan) was 12.4456 million units, with an average of 36,400 units sold per prefecture-level and above administrative region. Frankly speaking, the reference significance of the average is very limited. The reason is that this figure is more like a ruler pulled high. Among the 341 cities we surveyed, only 80 were above this ruler, accounting for 23.5% of the total number of cities, but their NEV insurance registration volume reached 9.2658 million units, accounting for 74.5% of the total. More striking is that the top 10 cities—namely Guangzhou (365,964 units), Beijing (362,038 units), Chengdu (359,175 units), Shanghai (357,974 units), Shenzhen (342,293 units), Hangzhou (327,887 units), Zhengzhou (318,251 units), Chongqing (283,892 units), Wuhan (278,292 units), and Xi’an (237,988 units)—had a total sales volume of 3.2338 million units, accounting for 26% of the national total. This means that the other three-quarters of the cities below the ruler only got less than a quarter of the market share. At the very end of the ruler are even quieter groups. In 2025, the total NEV insurance registration volume of the 100 cities ranked at the bottom was only 46,700 units. This figure is equivalent to only 12.8% of the NEV sales in Guangzhou (365,964 units), the top-selling city in 2025, and less than 1% of the total sales of the top 20 cities. Most of these 100 cities are scattered in the border areas of China’s territory. Gansu Province has 12 cities on the list, Heilongjiang Province and the Xinjiang Uygur Autonomous Region each have 9, Yunnan Province and Sichuan Province each have 8, Qinghai Province, the Tibet Autonomous Region, and Jilin Province each have 7, the Inner Mongolia Autonomous Region has 6, Liaoning Province has 5, the Ningxia Hui Autonomous Region has 4, Shaanxi Province, Hainan Province, and the Guangxi Zhuang Autonomous Region each have 3, Hunan Province and Jiangxi Province each have 2, and Fujian Province, Guangdong Province, Zhejiang Province, Anhui Province, and Henan Province each have 1. Northeast China, Northwest China, and Southwest China completely outline an arc-shaped zone of high cold and high altitude. This is almost an exact projection of the area west and north of the “Hu Huanyong Line”. In 1935, geographer Hu Huanyong drew a straight line between Heihe and Tengchong: 36% of China’s land area southeast of the line is home to 96% of the population; 64% of the land area northwest of the line has only 4% of the population. Ninety years later, the sales map of China’s NEVs has almost replicated this line—east of the line is the absolute main market of the 83 cities “above the average”; west and north of the line are densely packed with most of the cities in the bottom 100. Even more extreme figures come from the “silent places” for NEVs represented by Naqu. In 2025, there were 22 cities with NEV insurance registration volume less than 1,000 units. Among them, Qinghai (7 cities) and Tibet (6 cities) accounted for nearly 60%, and the rest were scattered in border or high-altitude areas of Sichuan, Yunnan, Heilongjiang, Gansu, and Xinjiang. Their distribution is by no means accidental, but highly overlapping with the geographical outlines of high cold, aridity, or extremely high altitude such as the Qinghai-Tibet Plateau in Southwest China, the desert in Northwest China, and the border areas in Northeast China. East and west, south and north, correspond to each other from afar. The early popularization map of NEVs is highly integrated with the area east of China’s population density dividing line, the “Hu Huanyong Line”. At the same time, due to their extreme fear of cold, the popularization of NEVs in cold Northeast China is not as good as that in cities south of it. This reveals the first and most basic logic of the NEV market: livability. The natural environment has placed a barrier that is difficult to cross with marketing rhetoric on the chemical properties of batteries and the economic feasibility of energy supplement infrastructure, cooling down the market enthusiasm. Absolute Dead Zones Cities with NEV insurance registration volume less than 1,000 units in 2025 are undoubtedly the “absolute dead zones” of China’s NEV market. The complex geographical environment of these cities weaves a tight network, restricting the entry of NEVs. High altitude is the most prominent feature of these 22 cities. Among them, 16 cities have an average altitude of over 2,000 meters. Among these 16 cities, 7 have an average altitude of over 3,000 meters. Naqu and Ngari Prefecture in Tibet, which stand on the “clouds”, both have an average altitude of over 4,500 meters, making them the two prefecture-level cities with the highest altitude in China. The other 6 cities with an average altitude below 2,000 meters are either special in political status like Sansha City, located in the core area of the Nu River Grand Canyon like Nujiang Lisu Autonomous Prefecture, or the “North Pole” of China like Daxing’anling Region. On the opposite side of this altitude map are the mild terrains of the NEV insurance registration highlands in eastern China. Except for Chengdu and Chongqing, most of the top 10 cities in insurance registration volume (Guangzhou, Beijing, Chengdu, Shanghai, Shenzhen, Hangzhou, Zhengzhou, Chongqing, Wuhan) have an average altitude of about 100 meters. In particular, the average altitude of land in Shanghai is only 2.19 meters, making it one of the prefecture-level cities with the lowest average altitude in China. Warm and relatively flat urban areas are the common geographical conditions of these fertile lands for the NEV market. In contrast, severe cold connects the high-altitude snowfields in western China with the forest sea in Northeast China. Whether it is the law learned in junior high school geography class that “the temperature drops by about 6℃ for every 1,000 meters increase in altitude”, or the weakening of solar radiation caused by latitude, these “absolute dead zones” all face long and harsh winters. Take Daxing’anling Region in Heilongjiang, where only 240 NEVs were registered for insurance in 2025, as an example. The annual average temperature in this region is -4℃ in Mohe City and the northern part of Huzhong District, and -2℃ in other areas, with cold winters and cool summers. Starting from October, the monthly average temperature in Daxing’anling Region is close to 0℃, and it does not return to above 0℃ until April of the next year. Moreover, from December to January every year, it is in a severe cold state of -20℃ to -29.9℃. Even though the extreme winter temperatures in high-altitude areas in western China are not as severe as those in Daxing’anling Region, there are still many days with temperatures below zero. More importantly, NEVs in high-altitude areas in western China, in addition to low winter temperatures, also face the shortcoming of climbing at high altitudes. The low temperature, low air pressure, and low air density brought by the high-altitude environment make it impossible for the battery to dissipate heat and cool down in time when the NEV is in continuous high-load output. It also makes it difficult for the battery to heat and keep warm, which consumes electric energy. In the end, the electronic control system usually chooses to limit the discharge power to prioritize protecting the battery. Severe cold will seal the battery of NEVs. Li Jingsheng, director of the National High-Cold Motor Vehicle Quality Inspection and Testing Center, stated at the end of 2024 that in an environment of -20℃, the range retention rate of current mainstream lithium batteries will drop sharply to about 40%. As for energy supplement, operation and maintenance reports of charging stations in northern cities such as Shandong and Hebei under the State Grid show that during the low-temperature period of -15℃ to -25℃ in winter, the average output power of charging piles drops by 55%-65% compared with normal temperature, and the queuing time increases by 2-3 times compared with summer. Even if the state invests in building charging and swapping stations, the huge cost and sparse population distribution are destined to make the user experience of NEVs in these areas worse than that in eastern China. Excluding Sansha City in Hainan with a special location (203 units), the population density of the other 21 cities is mostly below 30 people per square kilometer, and more than 80% of the cities have a population density below 10 people per square kilometer. For example, the population density of Ngari Prefecture in Tibet (53 units) is 0.37 people per square kilometer, and that of Yushu in Qinghai (24 units) is 1.63 people per square kilometer. Among the four first-tier cities of Beijing, Shanghai, Guangzhou, and Shenzhen, the lowest population density is Beijing’s 1,332 people per square kilometer, but the population density of its core urban area can reach 25,000 people per square kilometer, and the highest is Shenzhen’s 8,907 people per square kilometer. The tests of full-load climbing, winter travel, and long-distance travel make people’s anxiety about the range and energy supplement of NEVs an unavoidable reality in these areas, rather than a simple psychological feeling. Environment shapes demand. Therefore, we can see that in the “Guidelines on the Performance of New Energy Vehicles Equipped by Central Administrative Institutions” implemented at the end of 2025, it is specially stipulated that when central units purchase official vehicles in plateau areas (with an average altitude higher than 2,000 meters): The range of pure electric vehicles should not be less than 600km, and the pure electric range of plug-in hybrid vehicles should not be less than 100km; the minimum ground clearance of sedans, SUVs, and off-road vehicles when fully loaded should not be less than 130/140/200mm, and the minimum turning diameter should not be higher than 12m. Tibet and Qinghai provinces, as well as parts of Sichuan, Yunnan, Gansu, Xinjiang and other provinces with an average altitude of over 2,000 meters, which are applicable to this regulation, are exactly the areas with poor insurance registration performance. SUVs and pickup trucks, especially gasoline-powered models, are particularly favored by consumers in these areas. The challenges of the natural environment are difficult to completely break through. In contrast, the “relative dead zones” brought about by economic and cultural factors are more likely to become new breakthrough points. Relative Dead Zones The second logic of the NEV market is the local economic and cultural characteristics. Take Wenzhou and Dalian, which became trillion-GDP cities in 2025, as examples. The GDP of Wenzhou and Dalian in 2025 is expected to rank 29th and 30th in the country. However, Wenzhou ranked 18th in national NEV insurance registration volume in 2025 (159,800 units), while Dalian ranked 59th (58,400 units), a huge gap. In addition to Wenzhou’s location in a warmer subtropical monsoon climate, the differences in economic structure between the two cities cannot be ignored. Since the “14th Five-Year Plan” period, Wenzhou has been cultivating a “5+5+N” modern industrial cluster. By the end of 2025, it has formed a 300-billion-level new energy industrial cluster. Among them, the electrical and auto parts industries have long been Wenzhou’s advantageous industries, and new energy has been included as one of the city’s five strategic emerging industries. The agglomeration of NEV parts enterprises has nurtured not only NEV-related industrial clusters but also a stronger atmosphere of discussion and higher trust in NEVs. A more classic and direct example is that in the era of fuel vehicles, Guangzhou, the base camp of Japanese cars, as well as Dongguan and Foshan, which undertook a large number of Japanese auto parts production needs, many consumers preferred Japanese cars. Compared with Wenzhou, Dalian’s core industries are still dominated by green petrochemicals with a scale of 400 billion yuan and shipbuilding and marine engineering with an output value of 80 billion yuan. Even the new-generation auto industry with an output value exceeding 100 billion yuan still focuses more on traditional fuel vehicle parts, with limited correlation with NEVs. If Dalian’s economy is highly dependent on petrochemicals and traditional industries, making it a typical northern resource-based city, then Suzhou is a representative city with a profound foundation in the traditional auto manufacturing industry. In 2022, the output value of Suzhou’s enterprises related to emerging fields such as NEV whole vehicles, parts, automotive electronics, intelligent connected vehicles, and fuel cell vehicles has exceeded 200 billion yuan, accounting for more than 40% of the total output value of the entire auto industry chain. Also in 2022, Suzhou set a goal that by 2025, the total output value of emerging fields such as NEV whole vehicles and parts, intelligent vehicle networking, and automotive electronics will account for about 50% of the total 600 billion yuan output value. But so far, as a major traditional auto manufacturing city, Suzhou has factories of joint-venture brands such as FAW Toyota and SAIC Volkswagen, whose influence is still difficult to ignore. Therefore, we can see that Suzhou, whose GDP grew by 5.4% to about 2.8 trillion yuan in 2025 and could rank 6th in the 2024 GDP ranking, ranked 14th in NEV insurance registration volume in 2025 with 198,000 units, lagging behind cities such as Ningbo, Tianjin, and Xi’an, whose GDP performance is not as good as its own. Cities similar to Dalian and Suzhou include Zibo, Xuzhou, etc. Their geographical and economic conditions are suitable for the promotion of NEVs, but due to the constraints of local economic structure and culture, they show a mismatch between economic strength and NEV insurance registration volume, making them “relative dead zones” in the NEV market. However, compared with the “absolute dead zones” with numerous natural barriers, the situation of “relative dead zones” can be improved with government investment and industrial upgrading, making them loose “dead zones”. A Corner That Will Never Disappear In the past ten years, the state and society have made great efforts to promote NEVs. From 2009 to 2022, the central finance has invested more than 200 billion yuan in direct subsidies to enterprises for the promotion of NEVs and fuel cell demonstrations; consumer-side policies such as new energy vehicle purchase tax exemption and national subsidies are still stimulating the market. Among them, two actions are particularly critical: First, the NEV Going to the Countryside campaign, which was included in this year’s Central No. 1 Document. In the past six years, the number of participating models has increased from 60 in 2020 to 124 in 2025, and sales have jumped from 397,000 units in 2020 to 3.2087 million units in 2023, making NEVs more accessible to low-tier markets. Second, the “Hundred Counties, Thousand Stations, Ten Thousand Piles” energy supplement plan. Through financial support, the state has encouraged enterprises to participate in the construction of charging and swapping facilities in county areas, aiming to fill the gap in the county energy supplement network between 2024 and 2026. Enterprises are also actively sinking their markets. A typical representative is NIO, whose Power Swap Network covering all counties has been deployed in more than 1,000 districts and counties, making it one of the first car companies to build charging and swapping station routes in western China; BYD has extended its channels and services to more than 1,200 counties through the “county direct stores + township service points” network. Overall, China’s NEV “dead zones” are not monolithic, and their fate will undergo drastic differentiation with the passage of time and technological progress. Some “dead zones” will gradually be bridged, which is highly related to the substantial improvement of battery technology and the national energy supplement network. With the substantial improvement of battery technology in low-temperature performance and the more comprehensive and detailed coverage of the national energy supplement network, the consumption barriers caused by “severe cold” and “inconvenient long-distance energy supplement” will be greatly reduced. However, we must clearly realize that another type of “dead zone” may exist for a long time. This refers to areas locked by both extreme natural conditions and ultra-low population density. In wastelands and mountains with less than 1 person per square kilometer on average, even if the state invests in building and operating charging networks, it is difficult for car companies to balance the economic accounts of operating costs and income in these areas. The construction of infrastructure and technological progress take time, and the trust of local residents in NEVs also takes time. However, the returns from this part of the market are difficult to truly attract car companies to invest heavily. Therefore, the final picture we may see is that NEVs dominate the market with an extremely high market share of less than 100%, but there will always be room for fuel vehicles to survive on this land. The gap between the “8 units” in Naqu and the “360,000 units” in Guangzhou will narrow, but may never disappear. The ambitious market share target of new energy vehicles must also respect the constraints of natural conditions, economic conditions, and differences in cultural diversity, rather than trying to eliminate them forcibly. This may be the real sign of the maturity of China’s new energy vehicle industry—not only to actively embrace new things but also to have a rational sense of reservation. (End)

![Gasgoo, Xpeng, [Gasgoo News] XPENG GX officially announced; China's NEV insurance premiums up 34.8% YoY in 2025](https://cdn.topcarnews.net/media/id/aHR0cHM6Ly9pbWFnZWNuLmdhc2dvby5j-b20vbW9ibG9nby9OZXdzL1VFZGl0b3Iv-aW1hZ2UvMjAyNTA2MTAvNjM4ODUxNzAw-MTkzODM1OTU2NTQxNDEzNi5qcGc/c06991c2ffe2e05fe81c97062ebd8cf3.jpg?t=20260810&post_id=12479)