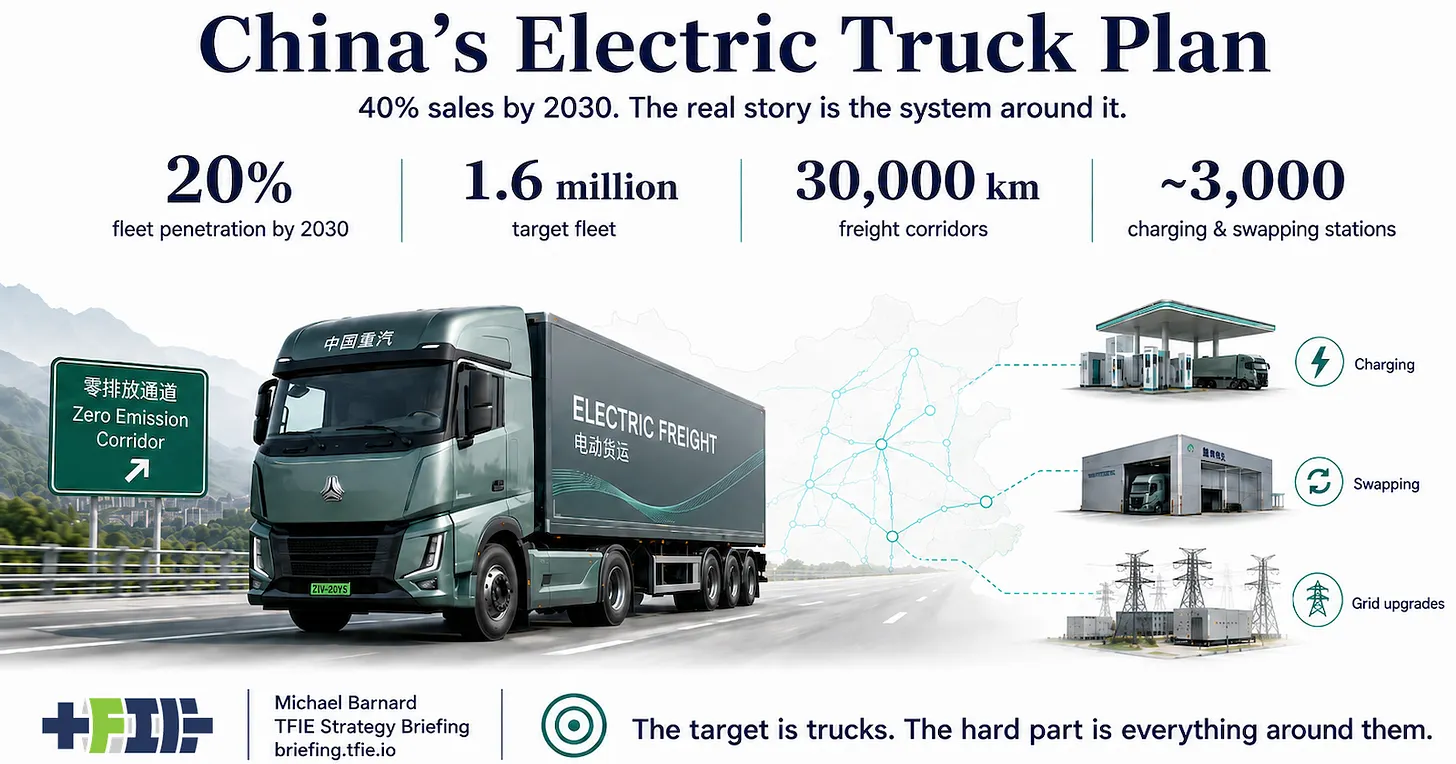

China’s new electric heavy-truck target is not interesting because another government wrote down a 2030 number. It is interesting because the target is tied to the system around the truck. The Ministry of Transport plan points to 40% of new heavy-truck sales being electric by 2030, 20% of the total heavy-truck fleet being electric, or about 1.6 million vehicles, and 3,000 charging and battery-swap stations as part of a zero-carbon highway push. On selected short-haul routes around Beijing, the target rises to 80%. Those are freight-system numbers, not just vehicle numbers. A battery-electric heavy truck only matters if the route, depot, charging point, grid connection, maintenance model, logistics contract and financing structure line up. A charger in the wrong place is a stranded asset. A truck without the right charging window is a procurement error. Heavy-freight electrification moves when the vehicle and the operating system around it are built together. China is already far enough along that the targets are not science fiction. Reuters reports that electric models made up nearly a third of China’s new heavy-truck sales in 2025, after growing quickly from a niche position over the previous two years. CATL has said that as many as half of China’s heavy-truck sales could be electric by 2028. That may prove optimistic, but it is the kind of optimism that comes from a fast-moving supply chain, not from a stranded pilot program asking for another grant. The practical examples are more useful than the rhetoric. Beiben Trucks showed a new electric dump truck with a 200 to 250 kilometer battery range and a claimed 22-minute charge, using a battery from EVE Energy. That is not a transcontinental sleeper-cab solution, and it does not have to be. Dump trucks, port trucks, mine trucks, construction-materials trucks, steel-mill trucks, cement logistics, drayage and return-to-base fleets are where heavy-truck electrification starts because the duty cycles are repetitive, routes are known and charging can be planned around work. That is the denominator many heavy-truck debates get wrong. They start with the hardest possible long-haul case and then imply that the entire sector must wait for that edge case to be solved. Freight does not work that way. It is a duty-cycle map. Some routes are long, irregular and payload sensitive. Many are not. The first large markets are the routes where batteries already fit or where depot power, corridor charging or swapping can make them fit. Battery swapping matters in that context. It is not the universal answer, but it is a useful operating tool where downtime, utilization, battery ownership and predictable corridors matter. Swapping can separate the battery asset from the truck asset, reduce waiting time and make high-utilization freight easier to electrify. Depot charging and high-power corridor charging will still carry a lot of the market, but China is not waiting for one perfect charging model to cover every route. It is adding tools where the freight problem needs them. The 3,000-station target should be read that way. It is not simply a count of places to plug in trucks. It is a decision to make freight corridors, depots and highway energy infrastructure part of the truck transition. The right station on a high-utilization corridor can change procurement behavior. The right depot upgrade can make a whole class of routes electric. The right swapping network can move heavier repetitive freight sooner than a pure charging-only model would allow. The contrast with hydrogen is not subtle once the system boundary is visible. Hydrogen trucking is usually sold on vehicle-level attributes: range, refueling time and the familiar rhythm of liquid-fuel logistics. But a fuel-cell truck is not just a truck. It is a truck plus a parallel fuel system: hydrogen production, purification, compression or liquefaction, distribution, station storage, dispensing, maintenance, safety systems, fuel quality and enough utilization to pay for all of it. The vehicle has to work, and the fuel system has to work. Battery-electric trucking has infrastructure burdens too, but they sit inside a power system that China is already expanding. Depots can be reinforced. Freight corridors can be prioritized. Batteries continue improving. Charging equipment can serve more than one vehicle class. The same grid that charges trucks also serves factories, ports, warehouses, rail yards, commercial buildings and other electrified loads. That does not make electrification easy, but it makes the infrastructure an extension of the central energy system rather than a second fuel system built beside it. China’s trade-in programs are part of the same architecture. The new plan prioritizes electric trucks in replacement incentives, which is how real fleet transitions happen. Trucking fleets turn over through operating cost, regulation, capital availability, residual value and procurement rules. If the incentive structure makes electric trucks the better replacement choice, manufacturers and logistics operators respond. China used similar trade-in and fuel-price dynamics to drive a wave of LNG truck adoption. The policy direction is now shifting toward electricity. The diesel implications are material. Heavy trucks are only one part of transport energy demand, but they are a visible piece of the remaining diesel system. Reuters has reported that China’s surge in electric heavy trucks is already forcing analysts to revisit diesel-demand forecasts. Rystad has estimated that the transport sector, which burns about two-thirds of China’s diesel, could use 40% less diesel by 2030. Electric heavy trucks are not doing all of that work, but they are no longer a footnote. The export signal is also worth watching. Beiben says about a fifth of its trucks are exported, with Southeast Asia looking promising, especially in mining applications. That is exactly the type of market where Chinese electric heavy trucks can travel well: mines, ports, industrial corridors, controlled routes and fleets where diesel logistics are expensive and charging can be planned. Europe and North America should not assume that China’s electric-truck capability will remain a domestic story. There are still hard limits. A 20% fleet target by 2030 means 80% of the fleet is not electric yet. A 200 to 250 kilometer dump truck is not a universal long-haul truck. A 22-minute charge is not the same as a solved grid-connection queue. Battery swapping needs standards, utilization and asset discipline. Megawatt charging will require real grid capacity. Freight markets are fragmented, and independent owner-operators do not have the same financing options as large logistics fleets. Those caveats define the build order. They do not rescue hydrogen trucking or justify waiting. Start with return-to-base fleets, industrial corridors, ports, mines, construction materials, urban freight, regional haul and predictable high-utilization routes. Build depot power and corridor energy infrastructure where trucks will actually use it. Track utilization. Standardize what needs to be standardized. Expand from the segments where the economics and operations work first. That is why China’s plan matters. It treats electric heavy trucks as part of a freight-and-power system. The target is connected to corridors, depots, charging, swapping, grids, incentives, manufacturers and use cases. Heavy-truck electrification becomes real when the system around the truck becomes real. For the full TFIE Strategy Briefing article, read China Just Made Electric Trucks A Freight System, Not A Vehicle Category. The Briefing version puts the 2030 target into the larger system frame: which freight segments electrify first, what infrastructure must be built around the truck, and why hydrogen trucking remains a higher-burden side bet.