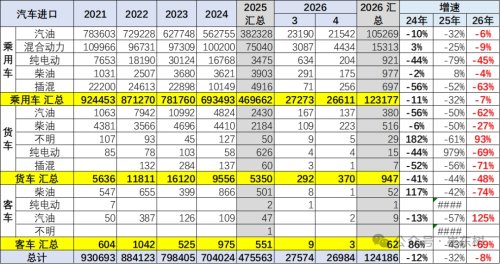

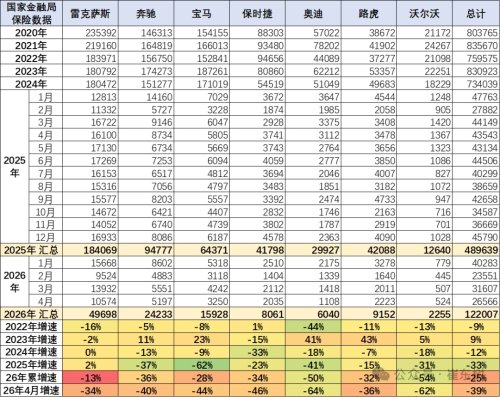

China imports totaled 27K units in April 2026, down 33% year-on-year. January–April imports reached 120K units, down 8%, supported by a low base last year. The market has been in long-term decline. Imports peaked at 1.43 million units in 2014. Volumes fell to 700K in 2024, down 12%; dropped further to 480K in 2025, down 32%. Trend of China’s vehicle imports and growth rates from 2007 to Apr 2026 Japan remains the largest source, shipping 13,607 units, accounting for over half of total imports. Germany ranked second with 6,658 units; the United States third with 2,518 units. The UK, Slovakia, Mexico, Austria, Thailand, China, South Korea followed. Stable supply and a broad model lineup support Japan’s lead. German and U.S. brands benefit from perceived engineering strength and brand trust. Passenger vehicles dominate imports. April passenger car imports reached about 26,730 units, over 99% share. Sedans accounted for 13,230 units, 49%; AWD SUVs 5,940 units, 22%. Auto import data across different types from 2021 to Apr 2026 NEV imports continue to shrink. January–April battery EV imports fell 45%; plug-in hybrids dropped 63%. NEVs account for only 2% of total imports, losing ground against strong domestic EV competition. At brand level, Lexus imported 10,574 units in April, down 13%, still leading the luxury import segment. Hybrid models retain steady demand. Import data of luxury auto brands from 2020 to Apr 2026 Ultra-luxury brands face sharper declines, down 52% in April. Bentley, Rolls-Royce remain weak with no clear recovery. Import data of ultra-luxury auto brands from 2023 to Apr 2026 Maserati pulls back after a high base in 2025, showing volatility. Ferrari holds relatively stable, one of the few resilient players in the segment.