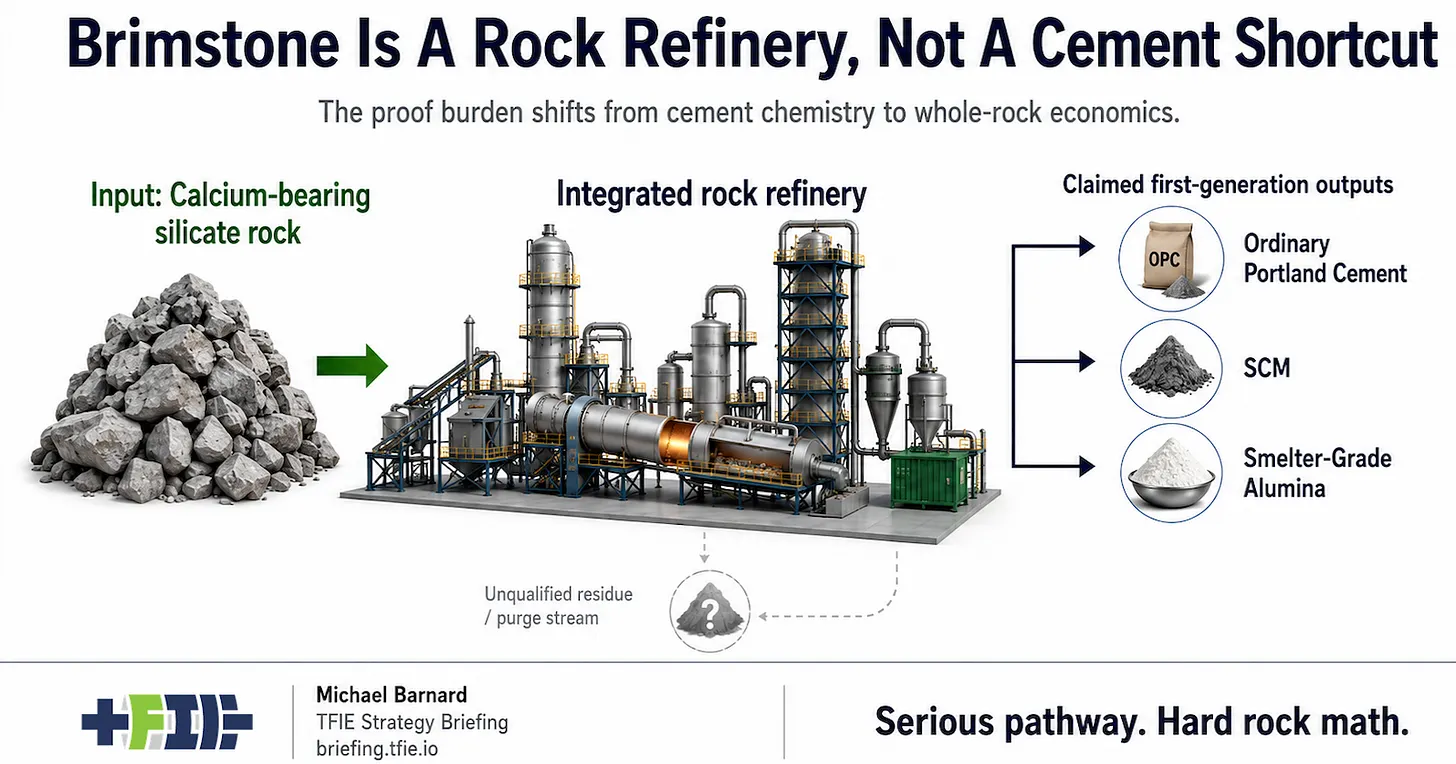

Brimstone’s cement story is interesting because it is not only a cement story. The company’s public positioning is now much bigger than ordinary Portland cement without limestone process CO₂. Brimstone is presenting itself as a Rock Refinery: a process that starts with calcium-bearing silicate rock and co-produces multiple industrial materials from the same feedstock. That is the right frame for diligence. A cement shortcut would be a simpler kiln, a better binder, or a clever retrofit into the existing cement plant model. Brimstone is closer to a minerals-refining business that happens to make cement as one of its first products. Its first plant is supposed to produce ordinary Portland cement, supplementary cementitious materials and smelter-grade alumina. The roadmap extends to aluminum, iron or steel, magnesium, titanium and other critical minerals. The conventional Portland cement problem is familiar. Cement plants use limestone, which is mostly calcium carbonate, as the calcium source. Kilns run hot, so there are fuel emissions. More importantly, calcination releases CO₂ from the limestone itself. Electrifying the kiln can help with heat emissions, but it does not remove the process CO₂ embedded in the carbonate chemistry. Brimstone’s strategic claim is that calcium does not have to come from limestone. Calcium-bearing silicate rocks contain calcium without carbonate CO₂. If that calcium can be separated, processed and recombined into ordinary Portland cement, the pathway attacks the limestone-process-emissions problem while preserving the material that builders, engineers, insurers and code officials already understand. That adoption point matters because cement is conservative for good reasons: it goes into structures expected to last for decades, under standards, specifications, warranties, procurement rules and liability systems that do not change quickly. But Brimstone is not only separating calcium. The company’s own refinery framing points to calcium, aluminum, iron, silicon and magnesium as material streams. In its minimum viable process, the relevant products are cement, SCM and alumina. That first product set matters because it is the early test of the business model. Cement alone is a low-margin, heavy, local commodity. Alumina and SCM change the value stack, but they also introduce more product-quality, market and offtake questions. The alumina claim is especially important. Smelter-grade alumina is not a casual byproduct. It is the intermediate material used to produce aluminum metal, and it has demanding quality expectations. If Brimstone can make saleable alumina from its rock-refinery process, that opens a much broader industrial story than cement decarbonization. It also exposes the process to aluminum-market dynamics, alumina quality requirements and competition from a mature global refining system. SCM is a different kind of product. Supplementary cementitious materials reduce the amount of clinker needed in concrete and cement blends. They are already central to many cement-decarbonization strategies, especially as traditional SCM supplies such as fly ash and blast-furnace slag become more constrained or geographically uneven. A process that produces both Portland cement and SCM could have a useful internal decarbonization logic, provided the SCM is reactive, consistent and accepted by concrete producers. The future-product roadmap makes the refinery framing unavoidable. Aluminum, iron or steel, magnesium and titanium are not cement-plant side notes. They belong to metallurgy, critical minerals, defense supply chains, aviation, automotive manufacturing, batteries and industrial policy. Brimstone is effectively saying that one abundant rock system can feed several of the world’s largest materials markets. That is a much bigger claim than “green cement.” It is also a more fragile claim. Multi-product refineries work when the product slate, separations, purity requirements, market demand, logistics and capital allocation reinforce one another. Brimstone is invoking that reference class, but it still has to prove its own version. The refinery model creates both upside and dependency. If cement, SCM and alumina all sell at acceptable prices, the plant may share feedstock, energy, equipment and capex across multiple revenue streams. If one of the products struggles, however, the plant economics may weaken quickly. That is where the diligence questions become concrete. What is the range of acceptable feed rock? How much geological variability can the process tolerate? What beneficiation is needed before the rock enters the plant? How much energy is required per tonne of each product? What reagents are consumed and recycled? What separations are needed to produce cement, SCM and alumina at market specifications? What residues remain, and how much of the rock becomes saleable material under real operating conditions? Brimstone says its process seeks to use the full feed rock and reduce waste. That is the right aspiration for a refinery. The evidence investors and policy makers should want is plant data: mass balance, energy balance, product quality, downtime, reagent losses, residue chemistry, water demand, maintenance burden, capex per tonne of product and realized offtake prices. A multi-product refinery can look elegant in a diagram and still be difficult in a commissioning schedule. The cement-product claim also needs to be kept separate from the refinery claim. Producing ordinary Portland cement that performs like conventional cement would reduce adoption friction. It would not by itself prove that the alumina stream is profitable, that the SCM stream is accepted, that future magnesium or titanium recovery is economical, or that the plant can operate at commodity scale. The cement evidence and the refinery evidence overlap, but they are not the same evidence. This is why Brimstone is one of the more interesting industrial-decarbonization companies and still a first-of-a-kind risk. The company is attacking a real problem with a pathway that avoids a real adoption trap. It is not asking the cement sector to become a chemistry experiment. It is trying to make the familiar material from a different rock. That is worth attention. But the larger claim is mineral co-production. Cement, SCM and alumina from the first plant are the first test. Aluminum, steel or iron, magnesium, titanium and other critical minerals are the broader roadmap. If the refinery model works, Brimstone becomes more than a cement-decarbonization company. If it does not, the cement story has to stand on its own in a low-margin commodity market. The right question is not whether Brimstone has a good cement story. It does. The right question is whether the rock-refinery business case holds together after feedstock, separations, co-products, product quality, capex, uptime, residues, offtake and commodity-market exposure are counted. Co-products must be saleable products with real demand, not optimistic labels attached to what the plant has to move out the back gate. For the full TFIE Strategy Briefing diligence review, read Brimstone Is A Rock Refinery, Not A Cement Shortcut. The Briefing version tests Brimstone as a first-of-a-kind industrial refinery: cement adoption advantages, limestone process CO₂, SCM and alumina co-products, future minerals claims, commodity margins, plant complexity and the evidence needed before investors or policy makers treat the pathway as repeatable.