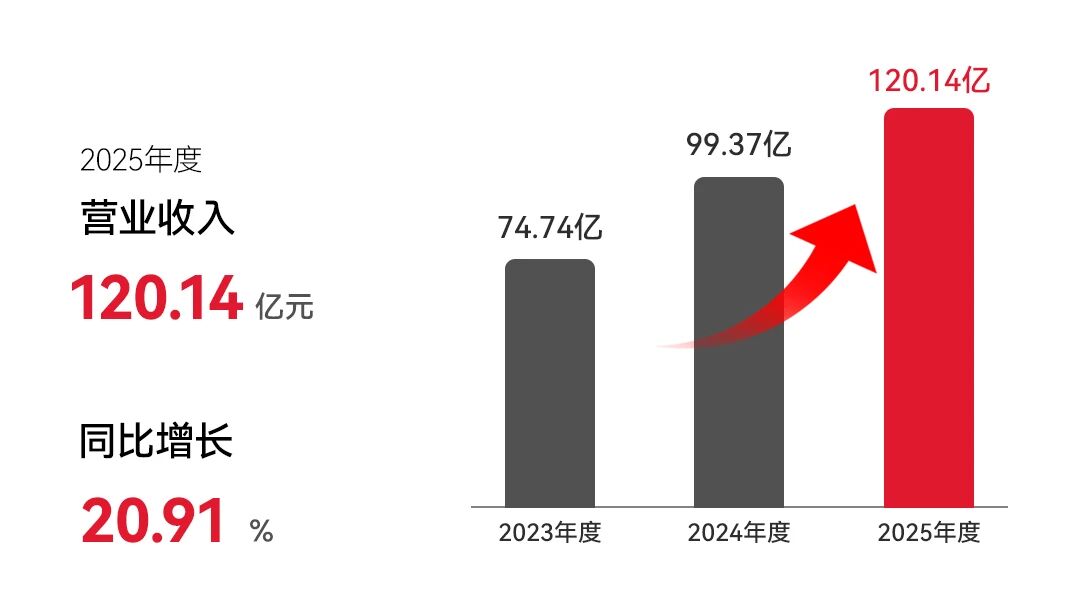

Gasgoo Munich- Bethel Automotive Safety Systems Co., Ltd. (WWBTL) recently released its 2025 annual report, posting full-year revenue of 12.014 billion yuan, a 20.91% jump that formally pushes the company into the 10-billion-yuan revenue bracket. Against a backdrop of slowing industry growth and intensifying competition, WBTL maintained steady expansion, driven by the continued ramp-up of its smart chassis business and supported by global client expansion and capacity planning.Image source: WBTL (same below)Still, there are caveats. While WBTL's revenue growth was robust in 2025, profit growth lagged behind revenue: full-year net profit attributable to shareholders came in at 1.309 billion yuan, up just 8.32%. Notably, fourth-quarter net profit slipped 2.99% year on year, signaling mounting pressure on profitability.Clear Revenue Structure, with Smart Electronic Control as the Core DriverWBTL surpassing the 10-billion-yuan mark in 2025 wasn't just about scaling up; it was the result of optimizing product, client, and capacity structures. The revenue surge was primarily driven by smart electronic control products, while traditional braking and steering operations provided a stable baseline, giving the overall growth strong structural support.Breaking it down by product, smart electronic control sales hit 7.0277 million units for the year, a 34.84% surge that made it the fastest-growing and most significant business segment. As automakers push for higher intelligence, penetration rates for brake-by-wire systems and chassis domain controllers continue to climb. WBTL has kept iterating on its WCBS brake-by-wire platform, with several new products entering testing and mass production, directly driving a synchronized rise in orders and sales.Disc brake sales reached 4.0626 million units, climbing 19.66%, slightly above the industry average, thanks to a recovery in the domestic passenger vehicle market and the securing of overseas client orders. Growth was relatively flatter for lightweight braking components and mechanical steering products, at 5.74% and 5.40% respectively, yet their massive shipment volumes still delivered a steady contribution to total revenue.Optimizing the client mix has further cemented the sustainability of this revenue growth. In 2025, WBTL added key clients including Renault of France, Ford Europe, FAW-Volkswagen, and SAIC-Volkswagen. It now cooperates with 8 of the world's top 10 automakers and 9 of China's top 10, steadily expanding its coverage. Volume procurement by these leading automakers hasn't just lifted overall volume; it has also diversified income streams, reducing reliance on any single customer.Meanwhile, the company secured 605 new awarded projects for the year, with an estimated total annual value of 9.508 billion yuan, up 45.4%. This substantial backlog of orders is set to convert into revenue over the coming years, underpinning continued growth. Building on this, WBTL is strengthening its steering business through capital integration. In February 2026, WBTL announced plans to acquire a 50.97% stake in Yubei Steering. If completed, the deal would significantly bolster its technology and market share in steering systems.Technology investment and capacity building have unlocked key bottlenecks for performance growth. Throughout 2025, WBTL advanced R&D in brake-by-wire technology, integrated motion control, and electronically controlled suspension. Progress on the fully localized WCBS solution, IMC integrated functions, and EDC electronically controlled dampers has further sharpened product competitiveness.On the overseas front, production at WBTL's Mexico base is steadily ramping up in Phase I, with Phase II construction underway, while planning has begun for a Morocco base. Backed by technical support from R&D centers in Germany and the US, overseas delivery capabilities have improved markedly. In 2025, WBTL successfully issued 2.8 billion yuan in convertible corporate bonds, providing solid funding for core capacity projects.Yet, global expansion has brought phased cost pressures. WBTL's gross margin fell 1.5 percentage points year on year to 19.65% in 2025. The squeeze on profits stems specifically from losses during the Mexico plant's ramp-up period (the Mexico subsidiary posted a -7.8% net margin in 2025) and price pressure from intensifying industry competition.Positioning for Robotics: Leveraging Manufacturing Prowess to Build Second Growth CurveEven as its core automotive business grows steadily, WBTL is pushing beyond its traditional boundaries, repurposing precision manufacturing and motion control technologies for the robotics sector in a bid to forge a second growth curve. This move is a natural extension of its supply chain advantages and reflects a broader trend among top-tier parts suppliers hunting for new growth engines.Auto components and humanoid robots share significant technological commonalities; both rely on core capabilities like precision transmission, motor control, and chassis actuation. WBTL's years of experience in braking and steering systems, specifically in high-precision manufacturing, mass production, and supply chain management, can be directly transferred to robot core components. In 2025, WBTL swiftly established key positions in screw and motor technologies by setting up two joint ventures: Zhejiang Bojian Transmission Technology, focusing on precision transmission parts like ball screws, and Wuhu WBTL Drive Technology, focusing on motor tech. These components are critical for flexible movement and force control in robots, and market demand is expanding as the industry matures.(Image generated by AI)To speed up commercialization, WBTL is using both direct investment and funds to build an ecosystem. It invested 35 million yuan in Mojia Robotics, a subsidiary of Chery, and established a 200 million yuan robotics industry fund, having already deployed 100 million yuan, to gain access to application scenarios, technical synergy, and client resources through supply chain partnerships. This "in-house R&D + investment" model mitigates the risk of heavy upfront asset expenditure while allowing rapid integration into the industry ecosystem and shortening product validation cycles.Logically speaking, humanoid robots are still in the early stages of commercialization, where localization and cost reduction of core components are key to widespread adoption. WBTL's edge lies in its mass-production capabilities and mature quality control systems. By leveraging its experience in auto manufacturing, the company can potentially lower costs for robot components and improve product stability. Furthermore, as some automakers expand into robotics themselves, WBTL gains a natural channel for cooperation, facilitating the transition from automotive supply chain to robotics supply chain.That said, the robotics business remains in the early investment phase and is unlikely to contribute significantly to revenue in the short term. WBTL's current moves are largely forward-looking initiatives aimed at seizing long-term industrial opportunities. For now, the value of this second curve lies not in immediate performance, but in building long-term technical barriers and widening the growth horizon.Overall, behind WBTL's 10-billion-yuan revenue in 2025 lies the robust growth of its smart chassis business and the steady implementation of its global strategy. While cautiously entering the robotics race, the company is sticking to its core strengths, a balance that demonstrates both commitment to its current advantages and judgment on future trends. However, as scale expands, issues like slowing profit growth and overseas losses serve as a reminder to the market that improving quality of profit will be a critical task for the next stage. As automotive intelligence and robot industrialization proceed in parallel, whether WBTL can sustain growth and successfully unlock its second curve will serve as a key case study for the industry in observing the transformation of parts suppliers.

![Gasgoo, Xpeng, [Gasgoo News] XPENG GX officially announced; China's NEV insurance premiums up 34.8% YoY in 2025](https://cdn.topcarnews.net/media/id/aHR0cHM6Ly9pbWFnZWNuLmdhc2dvby5j-b20vbW9ibG9nby9OZXdzL1VFZGl0b3Iv-aW1hZ2UvMjAyNTA2MTAvNjM4ODUxNzAw-MTkzODM1OTU2NTQxNDEzNi5qcGc/c06991c2ffe2e05fe81c97062ebd8cf3.jpg?t=20260811&post_id=12479)