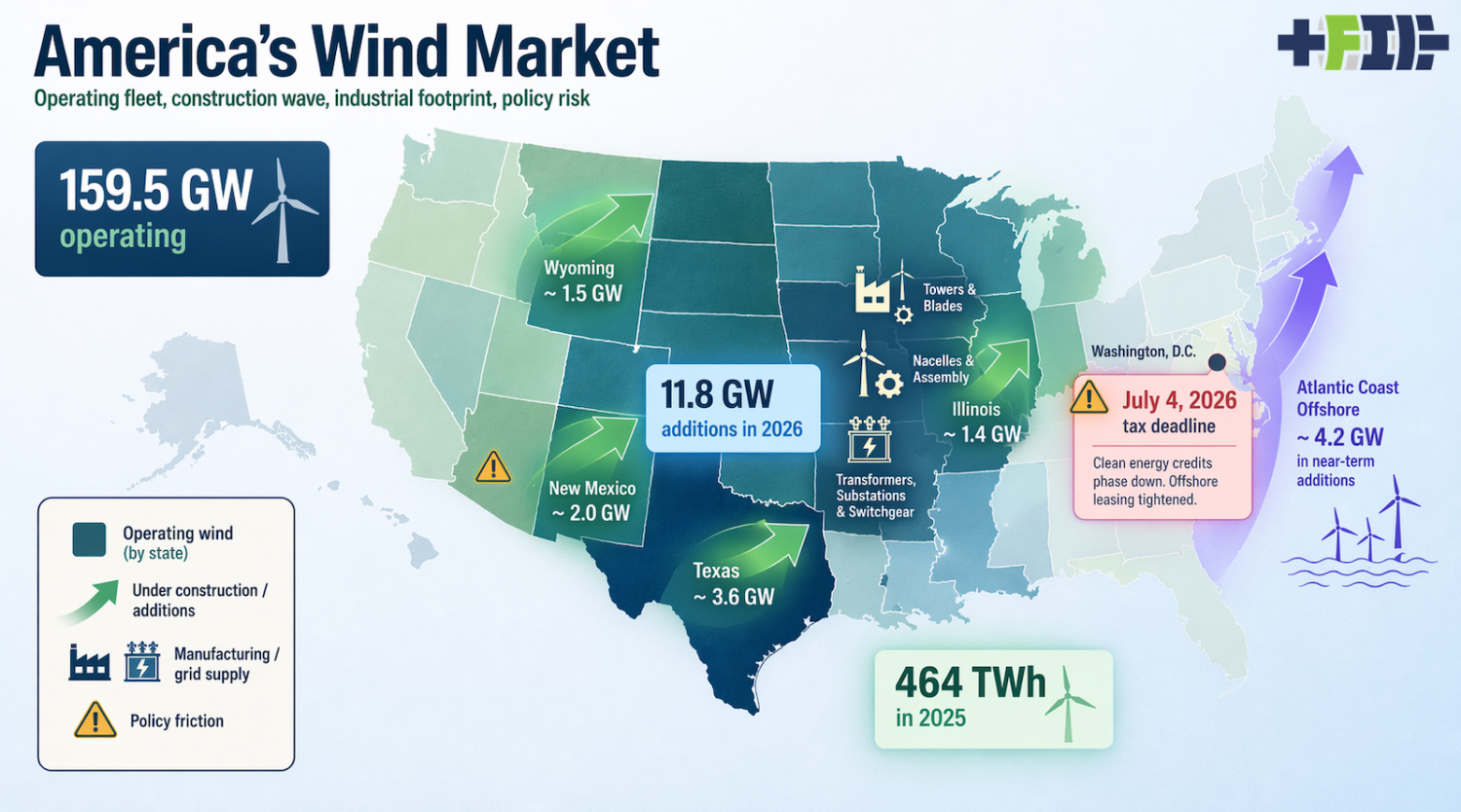

The useful way to understand U.S. wind energy in 2026 is to start with a contradiction. In physical terms, it remains one of the largest and most important wind markets in the world. In policy terms, it has become less stable and less predictable in a short period. The dichotomy is relevant as I prepare to provide context to a global audience through the bi-annual Global Wind Energy Association world wide update. The U.S. ended January 2026 with about 159.5 GW of utility-scale wind capacity in service, including about 159.3 GW onshore and 171 MW offshore. EIA’s February 2026 outlook also said developers planned to add 11.8 GW of wind in 2026, more than double the additions in 2025. That is not the profile of a collapsing industry. It is the profile of a large infrastructure sector still moving forward, but doing so in a harsher political environment. That installed base matters because it tells us where wind sits in the U.S. electricity system. This is no longer a technology living on tax credits and ambition alone. At roughly 159.5 GW, wind is one of the country’s largest generating fleets by capacity, behind natural gas and now alongside a rapidly growing solar fleet. The scale is continental. Texas remains the anchor state. The Great Plains and Midwest remain the long-established onshore heartland. The Mountain West has become a larger part of the next construction wave. The Atlantic seaboard is where offshore wind, despite its small current operating base, has moved from theory into contested physical buildout. The U.S. wind sector is no longer one market with one geography. It is several regional systems tied together by transmission, manufacturing, and federal tax treatment. The construction picture is where the current status becomes more interesting. EIA’s January 2026 inventory showed 14.0 GW of utility-scale wind in the next-12-month additions column, including about 4.2 GW offshore. Its February 2026 analysis simplified that into 11.8 GW of expected wind additions during calendar 2026, with New Mexico, Texas, Illinois, and Wyoming accounting for almost 60% of the total. That matters because the under-construction map is not just a rerun of the existing fleet map. Texas is still there, but the near-term build story now pulls hard toward the Mountain West and selected Midwestern states, while offshore construction remains concentrated on the East Coast. The U.S. is still adding turbines where the wind is strong and land is abundant, but it is also building where transmission pathways, load growth, and state policy still make large projects bankable. If capacity tells us how large the fleet is, generation tells us what it is actually doing. According to EIA, wind generated 464 TWh in 2025, up 3% from 2024. That is enough electricity to match the annual consumption of many medium-sized countries. EIA also reported that wind and solar together supplied a record 17% of U.S. electricity in 2025, with 760,000 GWh combined. Wind by itself was roughly 61% of that combined wind-and-solar output. If total U.S. generation was around 4,300 TWh, then wind’s contribution was a bit above 10%. That is the right scale to keep in mind. Wind is not an edge technology in the U.S. grid. It is a major electricity source that now shapes dispatch, prices, transmission needs, and planning assumptions in multiple regions. That physical strength sits beside a sharp federal policy reset. The cleanest single date in the new policy landscape is July 4, 2026. IRS Notice 2025-42 says the credit termination date applies to applicable wind and solar facilities whose construction begins after July 4, 2026, for the clean electricity production and investment credits under sections 45Y and 48E. In plain language, projects that fail to qualify in time move into a much less favorable tax position. In project finance terms, a hard deadline like that changes development behavior immediately. It pulls forward procurement, equipment orders, and construction starts where possible. It also raises the risk that marginal projects, especially ones facing interconnection or permitting delays, miss the window and become much harder to finance. The U.S. wind market in 2026 is therefore not just building. It is racing a clock imposed by tax policy. The offshore wind story makes the policy shift even clearer. The operating base remains tiny by national standards. EIA’s January 2026 data show only 171 MW of offshore wind in service. But the same inventory shows 4.155 GW of offshore wind in the next-12-month additions column, which means the technology is no longer hypothetical in U.S. infrastructure planning. That is why federal hostility matters so much. On January 20, 2025, the White House issued a presidential memorandum temporarily withdrawing all Outer Continental Shelf areas from new or renewed offshore wind leasing. BOEM then rescinded all designated Wind Energy Areas on the U.S. Outer Continental Shelf in July 2025. On December 22, 2025, the Department of the Interior announced an immediate pause on leases for all large-scale offshore wind projects under construction. A market can absorb a tax-policy change. It has a much harder time absorbing a federal posture that turns leasing, permitting, and already-approved construction into moving targets. What the Trump administration tried to freeze through political interference, the courts largely refused to let die. Five of the country’s marquee offshore wind projects, Vineyard Wind 1, Revolution Wind, Sunrise Wind, Empire Wind 1, and Dominion Energy’s Coastal Virginia Offshore Wind project, all won preliminary court relief after the late 2025 federal suspension orders, and all remained in construction or forward motion by April 2026. Revolution Wind had already begun delivering power into New England, Vineyard Wind had entered initial operations, and Sunrise, Empire, and CVOW were all still advancing through construction, commissioning, and related offshore works. The point matters beyond the individual projects. Washington succeeded in injecting delay, cost, and uncertainty, but it did not erase the industrial reality that billions had already been committed, steel was already in the water, and state demand for large-scale offshore electricity had not disappeared because a hostile administration wished it so. That does not mean state policy has stopped mattering. In the U.S., wind remains partly a federal market and partly a patchwork of state-level choices. Some states continue to treat wind as core infrastructure. Virginia still has a 5.2 GW offshore wind target embedded in the Virginia Clean Economy Act. New York continues to describe offshore wind as critical to serving downstate load and future clean-energy demand. Other states send the opposite signal. In March 2026, the Arizona Corporation Commission voted to repeal the state’s Renewable Energy Standard and Tariff rules, even while noting that line-siting approvals were still expanding renewable generation. That kind of split matters. It means developers cannot read the U.S. as a single policy jurisdiction. They have to navigate a market where one state is still planning around large-scale wind and another is dismantling long-standing clean-energy requirements. Transmission and interconnection remain the quieter part of the story, but they are central to what happens next. The U.S. does not have a wind resource problem. It has a delivery problem. The Department of Energy’s National Transmission Needs Study says significant within-region transmission deployment is needed as soon as 2030 in the Plains, Midwest, and Texas. By 2040, the Mountain, Mid-Atlantic, and Southeast also need large deployments. DOE’s grid office says current momentum would expand long-distance transmission line capacity by 16% by 2030, including 7,500 miles of new transmission lines. That is progress, but it also suggests a system still playing catch-up. Cheap wind in the Plains is only as useful as the wires that move it to load centers. Offshore wind on the Atlantic coast is only as useful as the substations, export cables, and onshore grid reinforcements that let coastal cities absorb it. When transmission lags, good wind projects start to look expensive, not because turbines stopped making sense, but because the grid stopped being ready for them. The industrial picture is stronger than many casual observers assume, but weaker than the rhetoric of full domestic energy independence suggests. DOE says there are more than 500 U.S. manufacturing facilities specializing in wind components such as blades, towers, generators, and turbine assembly. That means the U.S. is not simply importing finished wind farms. There is real domestic manufacturing depth. But the industrial base is uneven, and it becomes more constrained as turbines grow and offshore projects scale. NREL’s regional offshore supply-chain work says domestic manufacturing for blades, towers, and monopiles is likely insufficient for planned projects in the 2020s and early 2030s unless more announced facilities come online. That is a useful way to understand the market. The U.S. has a meaningful manufacturing base in towers, blades, nacelle assembly, power electronics, transformers, substations, controls, and broader balance-of-plant systems. But it does not yet have unconstrained domestic capacity across the entire supply chain needed for a very fast buildout. That industrial point becomes more important when one looks beyond the turbine itself. A modern wind farm is not just blades, tower sections, and a nacelle. It is also foundations, roads, collector systems, step-up transformers, reactive power equipment, substations, export lines, protection and control systems, grid software, and long-term service operations. NREL’s materials work on U.S. wind technologies explicitly includes the nacelle and drivetrain, generator, tower, blades, hub, foundation or offshore substructure, cables, roads, and substations as part of the system. In cost and construction terms, that matters. The turbine package may still be the single biggest cost block, but the electrical and civil stack around it is large enough that domestic industrial participation does not disappear just because some high-value turbine components are globally sourced. One reason wind has a deeper U.S. economic footprint than critics claim is that so much of the ancillary power-management and grid-integration work happens locally or regionally, even when the OEM platform is global. Distributed wind is the smaller part of the national story, but it should not be ignored. The giant utility-scale fleet shapes most of the headlines, yet distributed and small-scale wind still matter for agricultural loads, remote industrial uses, resilience, and rural economic development. DOE’s Competitiveness Improvement Project for small and medium turbines continues to support domestic design, testing, and certification, while its land-based economic development guidance keeps pointing communities toward the local construction and operating value of wind projects. In a country as large as the U.S., not every wind story is about a 300 MW or 1,000 MW plant. Some are about whether a farm, cooperative, tribal community, or remote facility can lower costs and improve resilience with a smaller machine. It is not the dominant volume story, but it remains part of the sector’s industrial and political durability. Opposition and misinformation are real, but they are often overstated as explanations for national market outcomes. Community friction can raise costs and delay permits. Offshore wind in particular has been hit with repeated false claims, especially around marine impacts, while onshore projects continue to face local disputes over sightlines, sound, land use, and transmission routing. But those are not the main reason the market looks conflicted in 2026. Federal tax deadlines, interconnection delays, transmission shortages, and direct federal hostility to offshore leasing and project approvals matter more. A good way to test that is simple. If social opposition were the main barrier, there would not still be 11.8 GW of wind additions expected in 2026 and more than 4 GW of offshore capacity in the near-term additions column. The market is not failing for lack of demand or engineering capacity. It is being narrowed by policy and infrastructure bottlenecks. From the perspective of the global wind industry, the U.S. now looks like a market with extraordinary physical depth and compromised political coherence. It still has roughly 160 GW of installed wind. It still generated 464 TWh from wind in 2025. It still plans to add 11.8 GW in 2026. It still has a large manufacturing ecosystem and some of the best onshore wind resources in the world. But it also has a July 4, 2026 tax deadline hanging over new projects, a federal government that has withdrawn offshore areas from new leasing, rescinded Wind Energy Areas, and paused leases on projects already under construction, and a transmission system that DOE itself says needs significant expansion across the core wind regions. That combination is unusual. The physical market says one thing. The governing environment says another. In 2026, U.S. wind energy is still a major and growing infrastructure system. It is just no longer operating inside a policy framework that treats that growth as something to support and extend.